How many times have you broken your pot to withdraw your savings from the piggy bank? If you’ve also done this, then you know the temptation to break the pot and take the money out. But this was a traditional method of saving. In this era, you can save whenever you spend. Want to know how? Then stay tuned with this article.

So many tactics we adopt in order to save our money for our future needs. Traditionally, we used to save our money in piggy banks. Whenever we have some extra pennies, we put that money in a piggy bank and wait until it is full. This way, we accumulate a handsome amount of money through small savings.

As mentioned, this is a traditional method, but today we have the privilege to use digital technology for saving as well. Now we can automate our savings without any extra hustle by leveraging the benefits of digital savings apps. These apps are designed to boost savings by contributing a small chunk of daily spending into gold or investing it into different portfolios, which, with large returns, yields a handsome profit.

What Are Digital Saving Apps?

Digital saving apps facilitate saving by leveraging AI and technology. These apps help you to save every single penny, and in addition to that, provide interest on it. You can create your goal for future spending and start saving for that goal now. Each day, when you see yourself going toward your goal will create a habit of saving in you and motivate you to continue further.

Top 12 Digital Saving Apps

There are many digital savings apps in the market, but the following are the best digital apps that you must try to make a profit.

Many of you are very much familiar with the word “Gullak”, as it is widely used by us for saving pennies and small amounts. Gullak is a goal-based saving app that helps to maintain consistency in saving and also to move towards your goal of saving. The amount we save in Gullak is invested in digital gold, which is 24k pure gold. This way, you can earn some interest on your savings through appreciation in the gold price.

Set your goal with as low as Rs 10 per day and automate the whole process of saving via the autopay facility. Currently, this app supports autopay from three UPI platforms like PhonePe, BHIM, and PayTM. You can adjust the contribution, pause, or revoke the autopay anytime.

The most influential feature of this app is saving on your spending. Whenever you spend your money digitally, it automatically rounds off the amount spent and invests in digital gold. For example, if you make a payment of Rs194, it rounds off the figure to the nearest 10 and invests the remaining amount of Rs6. This way, it accumulates a handsome amount of money by aggregating these small savings.

Features of Gullak

It invests in digital Gold provided by Augmont, where the buying and selling price is based on the wholesale market price.

Flexibility to change the duration of your goal, the amount of autopay, and the multiplier.

Automate your saving habit with Spenny, which is a spare change investment platform. The working of this app is similar to Gullak, but it has certain advantages. Whenever you spend money digitally, it accumulates your transaction data, and based on your transaction, it rounds up the figure to the nearest 10.

It holds all your rounded-up money in a cart and invests the whole amount into your desired investment option. There is a minimum threshold limit in the cart set by you, which means it invests your money when this threshold is met.

Let me clear one most common doubts, it doesn’t deduct the money to round up whenever you make any transaction. It accumulates the spare change in the cart and only deducts the money via autopay when it reaches the threshold limit decided by you.

Features of Spenny

There is no lock-in period, which means you can withdraw your money whenever you want.

It provides multiple investment options like Pennywise, mutual funds, and digital gold.

Fello

Rating

3.7/5

Best For

Gaming Enthusiast

Daily Savings App – Fello

Fello is a game-based digital saving app that enriches the saving experience with the fun and joy of built-in games. It offers two investment options to save money: fellow flo and digital gold. Users can opt for any of these two options to grow their savings and earn some interest. Digital gold of Fello is provided by Augmont, which is a government, BIS, and NABL-accredited Gold provider.

Apart from saving and investing in Gold and Fello Flo, Users can play exciting games and win rewards. This app provides a token for every single rupee you save, and you can use those tokens to play games. Also, every Rs500 of weekly savings makes you eligible to win a tombola ticket. A Tambola ticket is like a lucky draw coupon where you win a reward if your ticket number matches the leaderboard number. Every Friday at 6 PM, they announce the draw number.

Features of Fello

10% fixed return if you choose Fello Flo, which is a decent return compared to other fixed investment options available. This return may change anytime.

Along with the Fello Flo, the Digital Gold investment option is also available from a trusted provider, Augmont.

Win a Fello token every time you save some bucks, and use these tokens to play games.

Money Saving Apps

Wizely

Rating

4.2/5

Best For

Saving and future Plans

Digital Piggy Bank App – Wizely

Wizely is a savings app to improve your financial discipline and make sure you never run out of money at the end of the month. This app comes with many exciting features and gives a reward whenever you take one step forward toward your goal. There are some saving plans already created, like an emergency plan, safety plan, and growth plan, or you can create your custom plan and start saving.

The funds are automatically saved in the form of digital gold to earn some interest. Whenever you save some money and fulfil the challenges, it will provide you with a wellness score and a scratch card. The reward earned through scratch cards can easily be transferred directly to the bank account through UPI. Wizely Wednesday is another exciting reward contest to win rewards up to Rs 25 lakh. Your savings are in autopilot mode with Wizely, and it will also track your spending and all the transactions in one place.

Features of wisely

Budget creation and monitoring of the expenditure to build financial discipline.

Save more and take on challenges to win scratch cards and earn monetary rewards.

Expense categorization to prevent you from overspending.

Fi money

Rating

4.5/5

Best For

Working professionals

Best Money Saving Apps India – Fi Money

Fi Money is a one-stop solution for accounts, savings, investment, UPI, and lending. It is a neobank with a partnership with a federal bank that provides an enhanced banking experience to its customers. It is loaded with all the basic facilities of a traditional bank, with no minimum balance requirements and zero forex charges. RBI-approved Fi money insures your money up to Rs 5 lakh. Smart deposit is the piggy bank of this app to save money for your goals.

It allows you to save money for your vacations, a new house, a car, and many more. With the benefit of saving, it gives an interest of 5.45% on the amount you save. If you want to earn some extra interest of 5.95%, then you can simply switch to fixed deposits with the convenience of your smartphone. For better convenience and transparency, it connects all your bank accounts to its platform so that you can view all your transactions and bank balances in one place.

Features of Fi money

Multiple saving and investment options are available to choose from, based on your saving goal.

The Fi jump feature to earn a fixed interest of 9% every year and see your investment grow every day. Also, withdraw your investment anytime to your account.

Have a collection of direct and commission-free mutual funds to invest in.

Jar is a digital Gullak to save your hard-earned money into 24K digital gold. Just like you put pennies into your traditional Gullak, you can put spare change into a jar. This spare change is automatically debited from your account via UPI mandate. Jar is the best app for saving money in India digitally.

Whenever you make any digital transaction, Jar rounds up the value to the nearest 10 and invests the remaining spare change into your digital goal. SafeGold is the digital gold provider of Jar, which enables investing in digital gold to be feasible. One can easily withdraw the investment at any time with a single click. Jar also provides real-time updates on Gold prices through the chart. Also, there is a spin reward awarded to you whenever you save some money in it.

Features of Jar

You can choose to withdraw your savings either into a bank account or in the form of physical gold, which will be directly delivered to your home.

There is no lock-in period and minimum amount for withdrawal.

Seamlessly automate your savings via autopay and pause or revoke it anytime.

Jupiter

Rating

4.4/5

Best For

Expense tracking and management

Best Saving App in India – Jupiter

Jupiter is a federal bank-backed digital asset management platform that is loaded with banking facilities, investments, debit and credit card management, savings, and transaction tracking. Jupiter offers savings pots to save for future purchases. This pot lets you be aware of your savings for your goal and keeps you disciplined. Apart from saving, you can also make investments in direct mutual funds with no commission. These are no-penalty mutual funds, which means you don’t need to pay any penalty for SIP default.

A zero balance account with no forex charge is another notable feature of this app. Just like Fi money, you can configure your bank accounts and see all your transactions and bank balances at one single interface. It provides a Jupiter debit card with no annual maintenance charge. Earn a reward of 1% whenever you make a purchase using this card, also freeze and sleep the card with a single tap.

Features of Jupiter

Categorized insight into all the expenditures made through any of your bank accounts.

Intuitive interface to manage everything at a glance.

Get a 1% reward not only on debit card transactions but also on purchases through UPI.

Deciml is the next app on our list of digital portfolios. Like other saving apps we discussed so far, this also has the functionality to save your spare change and invest in a fixed return instrument. This supports all debit cards, credit cards, UPI, net banking, and ATM transactions to accumulate spare change.

While other apps invest your spare change in digital gold or mutual funds, this app invests your money into Lendbox. Lendbox is a P2P investment platform certified by the RBI. It invests your money into a diversified portfolio to earn interest on your savings. Deciml is currently working on implementing mutual funds and crypto in its investment portfolio. It’s a piggy bank app in India that supports all credit cards and helps you save money.

Features of Deciml

The main feature of Deciml, which differentiates it from Jar and Gulllak, is that it invests your spare change on a daily basis. It doesn’t wait to reach a certain amount to invest.

Offers return up to 10%, which is approximately 3X the savings account return, and 2.5X the FD return.

Cred

Rating

4.7/5

Best For

Credit card users

Best Money Saving Apps in India Digitally – Cred

Cred is a credit card management app that delivers amazing credit card-related services that eventually help you save a lot of money. The use of Credit cards is now very common among people, also most people tend to hold more than one credit card at a time. Credit cards come with a lot of benefits, only if you use them in a disciplined manner, and here Cred plays an exceptional role.

It helps in the timely payment of your credit card dues by reminding you of the due date. You can monitor all your credit cards in one place, their spending, EMIs, outstanding amount, and many more things. Apart from making you disciplined in credit card use, it also showcases the hidden charges associated with these cards.

It offers free credit scores to you from top credit rating agencies like Experian and CRIF. Cred allows you to become a member if you fulfil certain eligibility criteria. It checks your credit score when you apply for membership and approves you as a member if your credit score falls above the eligible score.

Features of Cred

Whenever you make a credit card bill payment through this app, it will reward you the Cred coins by which you can use to unlock exclusive rewards.

Since your Credit score depends on your credit behaviour, this app uses AI to provide you with the statistics of your spending patterns and usage.

Multiple credit card management facilities in one app, now there is no need to download separate apps for all your cards.

YNAB (You Need a Budget) is an app that acts as your personal finance manager that taking care of all your finances. It helps to manage all your finances in one place and also to make smart financial decisions. Integrate all your bank accounts in one place and see all your finances.

The goal-tracking feature will help you to track your progress at a glance. This app doesn’t allow you to save money on it, but it helps in different aspects of saving. Smart categorization of your expenses will help you monitor your expenses at the top.

Features of YNAB

Target setting for your goal to achieve it even faster.

Adjust your spending and move the money from one category to another seamlessly.

Easy monitoring of spending, goal progress, and budget.

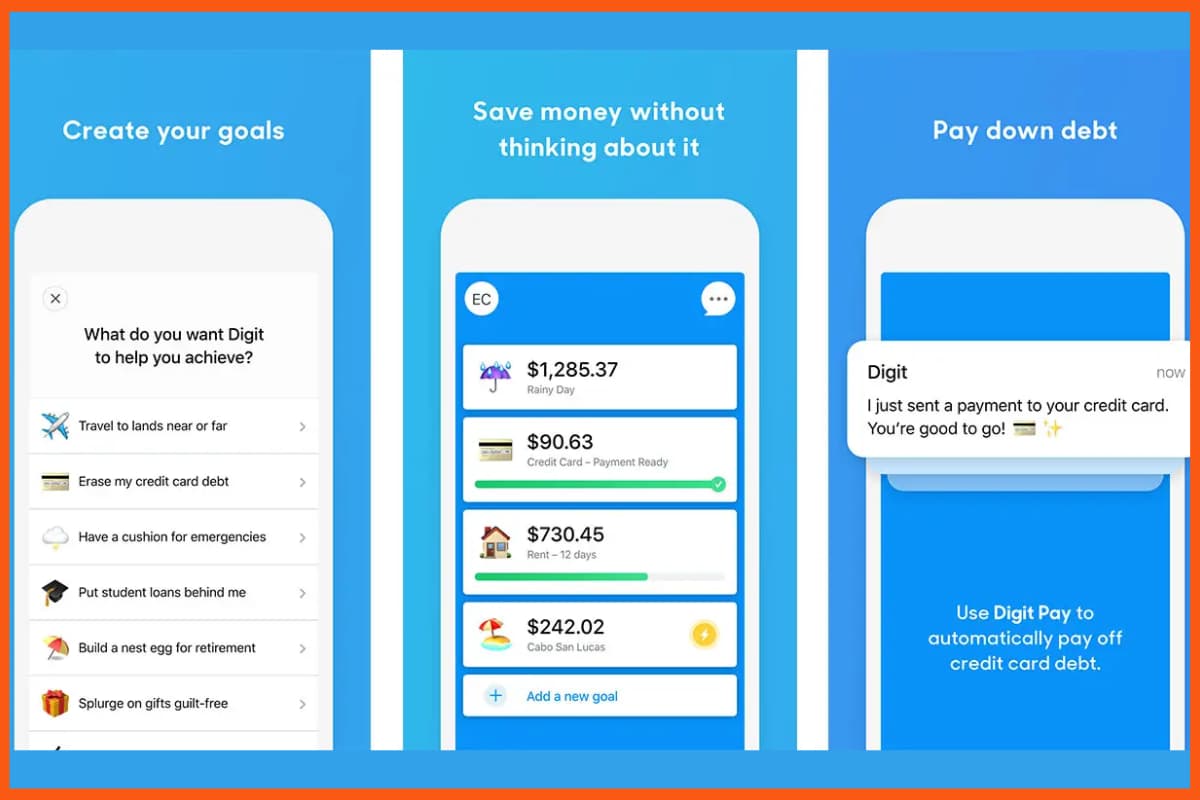

Digit is an AI-powered savings app that automatically analyzes your spending habits and moves small amounts of money into savings without you noticing. It helps you save for multiple goals like emergency funds, vacations, or debt repayment. The app removes the need for manual budgeting or transfers, making it ideal for people who want a hands-off approach to saving. Digit also offers features like overdraft prevention and investment options. It’s especially useful for users who struggle with consistent saving habits.

Features of Digit

Digit analyzes your income and spending habits to save small, safe amounts daily without manual input.

You can create multiple savings goals like travel, emergency funds, or debt repayment, and Digit allocates funds accordingly.

Digit monitors your bank balance and transfers money back if needed to help you avoid overdraft fees.

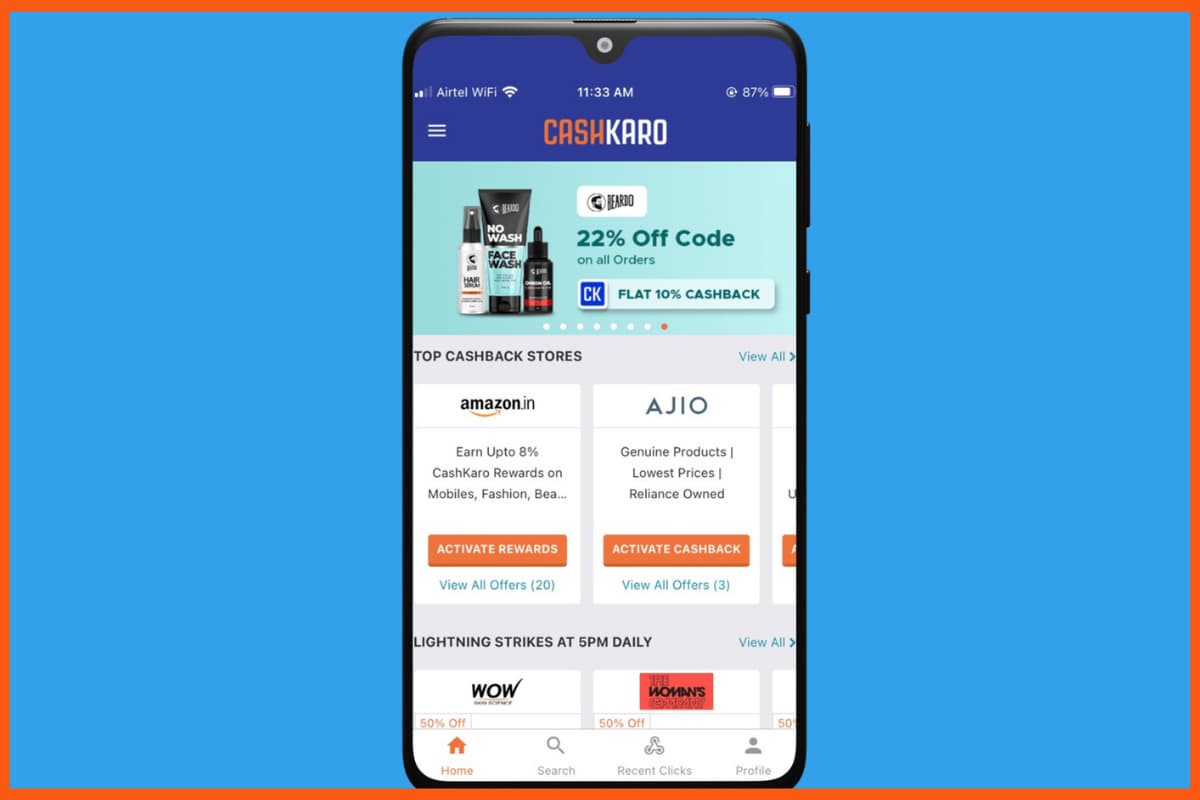

Cash Karo

Rating

4.2/5

Best For

Cashback and Coupons on Shopping

Best Digital Money Saving App – CashKaro

CashKaro is a cashback and coupons platform that helps users save money on online shopping. When you shop through CashKaro’s partner links, you earn real cashback on purchases from sites like Amazon, Flipkart, Myntra, and more. The cashback can be transferred to your bank account or redeemed as gift cards. It also offers exclusive deals and coupons to boost your savings. Ideal for regular online shoppers who want extra value on every purchase.

Features of CashKaro

You earn cashback when you shop on popular sites like Amazon and Flipkart through CashKaro.

It gives you exclusive coupon codes to save more money.

You can refer friends and earn extra cashback from their purchases.

Saving and investing for a future goal is the best thing you can start today, and these digital savings apps will help you in your journey. Today, we have a plethora of investment and saving options to choose from. You need to choose the right option that best suits your goals and requirements. Don’t think too much, just create your goal and start saving by choosing the best-saving App from the list we have provided.

FAQs

What are the benefits of Digital savings apps?

Digital savings apps can make the process of saving money easier over time. You can fill your piggy bank automatically so that savings goals can be met without stress, and it also helps you on tough days by automatically saving for you as you are spending. Some apps are programmed to make payments rounded off to the nearest whole number and save away the “change” you would receive if the transaction were done in cash.

Why is saving important?

Saving provides a financial “backstop” and provides financial security and freedom, and it also secures you in case any financial emergency arises. One can avoid debt, pay off loans, live their dream life, and avoid further debt if they have saved a sufficient amount.

Which are the apps like Jar?

Some of the apps like Jar

Gullak

Cred

Spenny

Fello

Wizely

Fi Money

Jupiter

YNAB

Deciml

Which is better in Gullak vs Jar?

Gullak and Jar are both digital savings apps that help you save money easily, but they work a bit differently. Gullak focuses on automating small savings by rounding off your daily expenses and putting the extra change aside, making saving effortless. Jar, on the other hand, also saves your spare change but invests it directly into digital gold, helping your savings grow with potential returns. So, if you want simple, automatic saving, Gullak is great. But if you want to invest your small savings in gold, Jar is a better choice.

Sameer Nigam is an Indian Entrepreneur who founded PhonePe, a UPI-based online payment system in 2015 and serves as its Chief Executive Officer (CEO). He also served as the Senior Vice President of engineering at Flipkart. In 2009, he launched his very first venture Mime360, which connects content owners to content publishers. He made a personal investment in an organization called Artifacia on 14 January 2016. He was listed in the top Indian business leaders 40 under 40 list by The Economic Times. He has a net worth of INR 17 crore.

Let’s go through the success story of Sameer Nigam along with getting a glance at Sameer Nigam’s Net worth, Education, personal life, how he founded PhonePe & more.

Sameer Nigam Biography

Name

Sameer Nigam

Born

1978

Age

47 (2025)

Nationality

Indian

Education

University of Mumbai, University of Arizona; The Wharton School

Sameer Nigam was born in Delhi and currently resides in Bangalore, Karnataka. His father worked in the Indian Navy and is an IIT graduate. Sameer Nigam’s mother is an entrepreneur and cleared her IAS on the first attempt at 40. Sameer’s wife is a consultant and together they have a son and a daughter.

Nigam made his way from Noida to Mumbai and finally to Bangalore where his company PhonePe is headquartered. His venture got a tremendous boost from the demonetization policy, which the Indian government announced in the same launching year of PhonePe.

Sameer Nigam – Education

Sameer completed his formal education at DPS Noida. He received his Computer Engineering degree from the University of Mumbai. He further went to the University of Arizona for a Master of Science in Computer Engineering (1991-2001). Later, he studied Master of Business Administration in Entrepreneurship at The Wharton School, University of Pennsylvania (2007-2009).

Sameer Nigam – Professional Life

Sameer Nigam, the Phonepe owner, served as the Director of Search Product Development at Shopzilla from May 2001 to June 2007. He then launched his venture, Mime360 in 2009 which is an online social media distribution channel. The company was later acquired by Flipkart.

He served at Flipkart from October 2011 to August 2015. While working for the eCommerce giant, he worked in several divisions including Marketing and Engineering as Vice President and Senior Vice President respectively. He further launched his digital wallet platformPhonePe in 2015, where he is positioned as the CEO.

He did exceptionally well in his corporate career with cordial entrepreneurial experiences to his credit. He displayed his skills in product marketing, eCommerce, strategic partnerships, online marketing, digital strategy, user experience, web applications, startups, mobile marketing, digital media, special needs, business development, web development, web analytics, and many more.

He is highly skilled in team management, digital marketing, non-medical homecare, lead generation, search engine optimization, strategy, mobile applications, mobile advertising, and online advertising.

Sameer Nigam – Founder of Mime360

In 2009, Sameer launched his first venture Mime360 (Mallers Incorporation), an online media distribution channel headquartered in Mumbai, India. The company offers an exchange platform connecting content owners with content publishers including Saregama, Indiatimes, and others.

Mime’s security is aided by API Feeds that help to prevent piracy and allow a large number of publishers to sell the licensed content globally. Most importantly, Mime eliminates various infrastructure costs for partners including content management, storage, and local data center bandwidth, and authorizes content owners to even set regional pricing.

Mime360 was acquired by Flipkart. The eCommerce giant has been looking to acquire small companies to grow the team. After the acquisition, some of Mime’s employees joined Flipkart to launch a digital music distribution service later. The strong entrepreneurial zeal, vision, and experience kept Sameer going and he soon launched another venture.

Sameer launched his Unified Payments Interface (UPI) based startup, PhonePe in December 2015. He is the Founder and CEO of Bangalore headquarteredPhonePe. He is a member of the Board of Directors at the company and advises on Marketing and several other strategies.

Sameer along with two of his friends, Rahul Chari and Burzin Engineer brought the idea of launching and designing an online payment app based on UPI. The PhonePe application went live in August 2016. It is available to users in over 11 Indian languages.

PhonePe was acquired by Flipkart in 2016. However, the e-commerce giant came into the ownership of US-based Walmart Incorporation in 2018 worth $16 billion. The acquisition of PhonePe was with the aim of expanding its online shopping footprint in India.

PhonePe’s first annual report shows a 73% revenue increase to INR 5,064 crore, with the company posting an adjusted profit of INR 197 crore after a INR 738 crore loss last year. Founders Rahul Chari and Sameer Nigam each earned INR 5 crore in FY24, with lower ESOP valuations compared to the previous year.

PhonePe IPO

PhonePe has officially become a public company, as confirmed by regulatory filings.

The change was approved at an extraordinary general meeting held on April 16, 2025, and the company’s name has been updated from PhonePe Private Limited to PhonePe Limited.

This move marks a significant step toward its much-anticipated IPO. PhonePe has been gearing up for a domestic listing, having recently shifted its headquarters from Singapore to India and appointed four investment banks to guide the IPO process. PhonePe is targeting a valuation of up to $15 billion as it prepares to strengthen its presence in India’s fast-growing fintech sector. Backed by Walmart, the company has brought on Kotak Mahindra Capital, JP Morgan, Citi, and Morgan Stanley to guide its IPO journey.

PhonePe founder and CEO Sameer Nigam issued an apology on Sunday for his comments about Karnataka’s draft job reservation Bill, clarifying that he never meant to offend the state or its people. His statement came in response to a ‘Boycott PhonePe‘ campaign initiated by Kannada groups, including the Karnataka Rakshana Vedike and other pro-Kannada organizations. The campaign started on social media after Nigam’s post on X, which commented on the Karnataka Cabinet’s approval of ‘The Karnataka State Employment of Local Candidates in the Industries, Factories and Other Establishments Bill, 2024’.

Here is the post that he made on X which caused backlash:

I am 46 years old. Never lived in a state for 15+ yrs

My father worked in the Indian Navy. Got posted all over the country. His kids don’t deserve jobs in Karnataka?

I build companies. Have created 25000+ jobs across India! My kids dont deserve jobs in their home city?

The Wharton Business School, University of Pennsylvania conferred him with the Wharton Venture Award in 2008. He has participated in two events. He attended the 16th NASSCOM Product Conclave 2019 on 5 November 2019, held in Bangalore, Karnataka, India, Asia. He attended Money 20/20 Asia 2019 as a Speaker on 19 March 2019 held at Central Region, Singapore, Asia.

His venture PhonePe was conferred with a list of awards, which are as follows:-

PhonePe was recognized by the National Payments Corporation of India (NPCI) for attracting the largest number of merchant transactions on the UPI network. (2018)

Received Best Mobile Payment Product or Service Category at the IAMAI India Digital Awards 2018

Won the UPI Digital Innovation Award from NPCI (2018)

Won the SuperStartUp Asia Award (2018)

Won the Telecom and Technology category award from India Advertising Awards (2018)

Won the Best Mobile Payment Product or Service at the 9th India Digital Awards 2019 conducted by IAMAI

Received the Best Digital Wallet initiative at the 8th annual Indian Retail & eRetail Awards 2019 conducted by Zee Business and The Economic Times.

Awarded Fintech Person of the Year – India at the Global Fintech Fest 2024.

FAQs

What Sameer Nigam net worth?

Sameer Nigam has a net worth of INR. 17.7 crore (as of 2017).

What is Sameer Nigam education?

Sameer Nigam has completed a Computer Engineering degree from the University of Mumbai, an MS from the University of Arizona, and an MBA in Entrepreneurship from The Wharton School, University of Pennsylvania.

The super.money app, which is a credit-first UPI (Unified Payments Interface) payments gateway app developed by India’s eCommerce giant Flipkart, intends to rapidly transition into a secured lending role in the next months.

According to a press release issued by the fintech, the app had about one million downloads during the test phase, which resulted in more than ten million transactions. National Payments Corporation of India reports that monthly credit transactions on UPI exceed INR 10,000 crore.

As a First Offering, Super.money Offers a Rupay Credit Card

The RuPay credit card, which functions similarly to an interest-bearing wallet on the UPI platform, is the initial offering from super.money. Already, Super.money has released an additional product—unsecured personal loans—in partnership with leading banks in India.

“The retail credit industry is booming and offers a lot of potential,” according to Prakash Sikaria, founder and CEO of Super.money, who spoke with a prominent media outlet. “Secured credit products have not been developed further and have not experienced the proper level of adoption,” he opined.

According to Sikaria, the Tier II and III markets in India are where the credit on UPI opportunity lies. From the standpoint of the user, it presents a three- to fourfold potential compared to conventional credit cards. Specifically, he emphasised how the beta phase shaped the super.money experience and how they innovated at the forefront of UPI credit in a press statement.

However, Super.money will have to distinguish itself through its products rather than relying just on UPI-backed transaction volumes if it wants to stand out in the still-growing but highly competitive lending industry, which is dominated by banks and NBFCs.

Secured Vs Unsecured Loans

The fast growth of unsecured loans in India’s retail loans segment over the past two years has been brought to the attention of the Reserve Bank of India in both informal meetings with banks and the formal publishing of the Financial Stability Report, which is done half yearly.

The risks associated with certain categories of unsecured loans were given a higher weightage by the regulatory body in November of 2023. The intended outcome has already been achieved. Following the RBI’s action, the growth rate of credit card portfolios dropped from 30% to 23%. In a same vein, bank lending to NBFCs fell to 18% from 29% previously.

Secured loans (vehicle, home, loan against property) are safer bets than unsecured loans (personal loans, credit card loans, and other types of consumer durables and student education loans), which do not require collateral. Lending system vulnerabilities increase when combined with a regime of still-high interest rates.

Many fintech companies in India compete for customers in the secured lending market by offering digital loans collateralised by precious metals and fixed deposits. Banking institutions and non-bank financial companies (NBFCs) have a greater branch network and street fleet, allowing them to dominate other products like home and vehicle loans.

Sikaria has faith in the possibilities of the cosmos he intends to serve. According to his polls, a mere fifteen to twenty percent of individuals who apply for a credit card actually receive one. Financial product cross-selling is super.money’s goal in the unsecured lending market.

The plan is to attract and keep users with greater average revenue per user (ARPU) by offering them greater incentives. The goal for Super.money, similar to other fintechs, is to increase the percentage of users who purchase additional financial products through cross-selling.

UPI or Unified Payments Interface is an instant real-time payment system created by the National Payments Corporation of India, which likewise implies that the Reserve Bank of India controls it. It helps to instantly transfer funds between two bank accounts with the help of a mobile app. The most common ones you might have come across in recent times are Paytm, PhonePe, MobiKwik, iMobile, BHIM app, among many others. Even the banks that boast of their own UPI app include Airtel Money, Axis Pay, Baroda MPay, Pockets-ICICI Bank, SBI Pay, Yes Pay, and so many others.

UPI reported 6.28 bn transactions in July 2022 that amounted to Rs 10.62 trillion, which is the highest-ever transaction volume since 2016!

In the words of Indian economist Raghuram Rajan, UPI means the

“WhatsApp moment for banking”

What is UPI? | Unified Payments Interface Explained

If you’re new to UPI or want to learn more about how it works, this blog is for you. In this post, we’ll cover everything you need to know about UPI, including its features, services, advantges and disadvantages, and how to use it. We’ll also discuss different types of UPI apps and how to use them. By the end of this blog, you’ll have a clear understanding of UPI and how it can benefit you in your daily life.

The UPI payments or Unified payments interface is a payment mechanism that allows instant money transfer without bank details. The UPI is developed by the NPCI and rather than a bank account number and IFSC code, the virtual payment address is utilized to pay through the UPI. UPI offers a wide range of services that make it a convenient and efficient payment system.

Here are some of the key services offered by UPI:

The most cost-effective way of money transfer

Fund transfer via NEFT entails a minimum charge of Rs 2.5 per transaction while the IMPS charges Rs 2.5 per transaction. On the other hand, UPI only charges 50 paise or less per transaction through the Unified payments interface. As such it has the potential to promote non-cash transactions of small amounts throughout India, which it is currently taking up seriously.

Cash-free functioning

UPI payments have made it a possibility for you to transfer a small amount to your vegetable vendor in a matter of seconds. Think Paytm or BHIM cards hanging on the local grocery store replacing the trouble you went through earlier to get a proper change. Think of the lesser time spent in the ATM lines. Going cash-free removes many hassles from your life and makes everything smoother in the age of digital India.

Security

People have stuck with their cash payments because primarily they couldn’t rely on online transactions and card payments as they ask for bank account details. However, the UPI method of payment cracks the deal here. The payment through the UPI does not require card details or the details of a bank account. You just need to enter your virtual payment address this way (think about the mobile number linked to your UPI app).

Real-Time Fund Transfer

Everything about the UPI app is an instant formula. Traditionally, adding new pay for the online fund transfer takes some time. This time varies from half an hour to 24 hours. In UPI, you can add a new payee instantly and transfer funds. Also, the process of fund transfer takes a few seconds with the help of a good data connection, which is very accessible for everyone now!

Cheaper alternative to POS machine

It is difficult to pay with the help of a banking card (debit or credit) everywhere you go. Most of the merchants don’t have a card swiping machine or sometimes the machines fail to catch signals. The machine in question is known as the POS terminal, which is a costly affair for the billing party involved. They have to pay the service charge for each transaction, which varies from 1.25% to 2.5% of the transaction value. This is why the UPI apps for merchants were introduced. You would have also faced the situation when the vendor asks for the service charge from you. It happens in a competitive market. Keeping the POS terminal is not very beneficial for small traders. However, UPI would help you do the same job without any cost incurred. As UPI operates through the smartphone, anyone can collect money without spending time and money on such machines. Also, the transaction cost is a mere 50 paisa, which is very low compared to the POS terminal.

One UPI app works for all the bank accounts

One might think that Axis Pay only supports Axis Bank accounts but the user gets to choose the UPI app they want to use and link all their Axis and Non-Axis bank accounts with them without any limitation. Be careful to choose the app that gives you maximum ease and options.

One-Stop Solution

The digital wallet has eased online payments. Opting for mobile recharges, buying rail tickets, shopping online and more have become very smooth because of the emergence of digital wallets. However, the number of such wallets is increasing by the day. Paytm, Freecharge, Flipkart, and IRCTC want you to keep the digital wallet. Naturally, it becomes a hassle to maintain more than one wallet. The UPI ends this problem as well. The payments through the UPI are as simple as payments through wallets, and only one app is enough to pay anywhere. Also, the UPI does not ask for money in advance. Rather, your money remains in the bank account and keeps earning interest. Digital wallets, on the other hand, don’t give us any interest as well.

Overall, UPI offers a range of services that make it a versatile and convenient payment system for users in India. Its user-friendly interface, quick transaction times, and advanced security features have made it a popular choice for digital payments.

Unified Payments Interface is developed by the National Payments Corporation of India

Currently, UPI is a free of charge payment platform. However, there has been no official statement from the authorities regarding a permanent waiver of transaction fees. The reason why UPI is free to use is its simple and cost-effective design. NPCI has been instrumental in democratizing mobile payments in India, making UPI a preferred mode of payment for even small transactions.

Despite the lack of transaction fees, NPCI has indicated that they would keep the cost of UPI very low. They have proposed a range of charges from 0 to 50 paisa per transaction. This range of charges is intended to keep UPI cost-effective and accessible for all users, including those who make small transactions frequently.

The UPI system is hailed as one of the most successful real-time payment (RTP) systems in the world since it has been adopted in India. This innovative payment interface offers simplicity, safety, and security to P2P as well as P2M (person to merchant) transactions in India. According to 2021 reports, the UPI system of payments reinforced by the UPI bank apps helped in successfully materializing over 39 Bn financial transactions, which amounts to a business of around $940 Bn, which is again equivalent to around 31% of India’s GDP. The ease of use of the UPI apps and the interoperability between them are some of the prominent reasons driving the growth of the UPI industry. The total number of transactions in a month crossed an all-time high of the $100 billion mark in October 2021.

As per a recent report, UPI continues to be the primary platform for digital payments in India, as the total number of transactions surged by 70% in 2022, reaching a staggering count of 74 billion.

The growth of UPI has transformed the digital payments landscape in India, and its impact is being felt across various industries. With its user-friendly features, low transaction costs, and growing acceptance among consumers and merchants, UPI is poised to become the de facto standard for digital payments in India in the years to come.

Unified Payments Interface (UPI) has been integrated with credit cards to provide users with a convenient and secure payment option. With this integration, users can link their credit card to their UPI ID and make payments using their credit card balance.

This integration has several benefits for users. Firstly, it eliminates the need to carry multiple payment instruments, as users can now use their credit card for UPI transactions. Secondly, it enables users to make digital payments even if they do not have sufficient funds in their bank account, as they can use their credit card balance for UPI transactions.

To link a credit card to UPI, users need to follow a few simple steps. They need to open their UPI-enabled mobile banking app, go to the add payment option, and select credit card as the payment instrument. They will then need to enter the details of their credit card, such as the card number, expiry date, and CVV. Once the details are verified, the credit card will be linked to the user’s UPI ID.

Once the credit card is linked, users can make payments using their credit card balance by selecting the credit card option on the payment screen. The payment will be processed through the credit card network, and the user’s credit card balance will be debited accordingly. Users can also view their credit card transactions and balance on the UPI app.

UPI to Reduce Declined Payment and Payment Timeouts

Users of UPI have frequently reported issues related to payment timeouts and declined payments, which poses a significant challenge for UPI transactions. To address these issues, the National Payments Corporation of India (NPCI) has set its sights on reducing declined or timed-out payments through a new feature.

The NPCI aims to minimize these issues in real-time by enabling banks to take action within 30 seconds to unblock funds that may have been caught due to failed UPI transactions. Currently, this process can take up to 24 hours, causing inconvenience and frustration for users.

This move by NPCI is expected to significantly improve the user experience of UPI transactions and further strengthen the position of UPI as the preferred digital payments platform in India. By reducing the number of declined or timed-out payments, UPI will become even more reliable and convenient for users, boosting its adoption across the country.

Growth of UPI outside of India

The UPI, which has been strictly an Indian concept, prevalent across the nation will now be also adopted by Nepal. This has made Nepal the first country to adopt the Indian UPI system, as of February 2022. The deployment of the UPI system in Nepal would be overseen by NPCI International Payments Ltd. (NIPL), the international arm of NPCI with a partnership with Gateway Payments Service (GPS) and Manam Infotech. Here GPS serves as the authorized payment system operator in Nepal whereas Manam Infotech will further aid in the deployment of the services in Nepal.

The UPI transactions have been accepted by many other countries too, after Nepal. These mobile-based fast, real-time payments, are now already happening in the UAE, Singapore, and Bhutan. France will be the latest addition to this list of countries. According to the National Payments Corporation of India (NPCI) announcement on June 17, 2022, the UPI and RuPay cards will be accepted in France soon. The NPCI’s international wing has already signed a memorandum of understanding (MoU) with the Lyra network of France for the acceptance of the UPI and RuPay across the country.

The Tata Group will soon be joining the league of the UPI apps, as per the news dated March 16, 2022. The multinational conglomerate is currently seeking clearance from the NPCI as per the reports. The Tata Group might also partner with ICICI Bank, as a private lender, via its digital commerce vertical Tata Digital, to power its UPI infrastructure. Tata Group has already applied to the NPCI to operate as TPAP (Third Party Application Providers) and is hoping it can go live soon.

According to the latest updates dated July 12, 2022, NPCI stated all of the UPI-based applications should first obtain the authorisation of the customers before they start recording their location and geographic coordinates. This system shall be followed without exception even for the customers who have already agreed to reveal their location originally while using the services, mentioned NPCI. In addition, the National Payments Corporation of India also mentioned that the UPI services of the apps shall continue even after the customers have revoked their consent for “sharing the location or geographical details for the app”.

Some major growth highlights of UPI are listed below:

The UPI transactions touched new heights when they crossed Rs 5 lakh crore mark in value in March 2021.

NPCI has mentioned that it will ban all gaming transactions via UPI on April 20, 2021.

Unified Payments Interface (UPI) crossed the 4 billion mark of transactions for the first time ever in October. These transactions concluded 2021 at a record high, where it recorded Rs 456 crore worth of transactions at Rs 8.26 lakh crore ($111.2 Bn).

The UPI payments recorded around 4.53 billion transactions, which is worth Rs 8.26 trillion in February 2022. It has almost doubled since the same time last year. Besides, the total value of UPI transactions was measured to be at Rs 41 trillion.

UPI recorded 6+ billion transactions in July 2022, which is the highest ever volume since it was founded in 2016. The 6.28 bn transactions that UPI platforms have seen amounted to Rs 10.62 trillion.

UPI boasts of a network of 330+ banks and an average ticket size of INR 1,730 per transaction. This makes UPI the most popular digital payment system in India.

The MoM Growth of UPI Transactions

The UPI transactions have been growing month on month. Though the UPI transactions declined slightly in June 2022, where there were Rs 586 crore transactions in contradiction with the Rs 595 crore transactions noticed in May 2022, the UPI payments have largely been quite unaffected by the RBI guidelines and the global economic scenario.

Among the duopoly that we always witness in the UPI ecosystem, of PhonePe and Google Pay, Whatsapp has risen to a record high in June 2022 with its UPI payment feature. Though WhatsApp Pay accounts for only 0.4% of the total UPI ecosystem of India, it has registered 2.3 crore transactions worth Rs 4,290.6 crore, thereby rising by 45% MoM in transaction volume and jumping 6.5X MoM in transaction count. The transaction count of Whatsapp Pay in May 2022, was only 34.8 lakhs, which were worth around Rs 294.98 crore.

Here is a table showing the MoM growth of UPI transactions in India:

Year

Total Number of Transactions

MoM Growth

2016

0.32 million

N/A

2017

915 million

2,746%

2018

17.9 billion

1,857%

2019

10.8 billion

-40.3%

2020

22.3 billion

106%

2021

43.5 billion

95.2%

2022

74 billion

70%

Crypto Payments Stopped through UPI

Some of the platforms including Mobikwik, the wallet firm of India, and the international crypto exchange, Coinbase, have been using the UPI platforms for cryptocurrency transactions. However, as per the NPCI statement, it wasn’t aware of any such happenings.

“We are not aware of any crypto exchange using UPI,” said NPCI

in a statement on April 7, 2022, which indirectly meant a warning to all the platforms doing so and an urge to stop them from doing so.

UPI – Milestones

UPI transactions concluded 2021 at a record high, where it recorded Rs 456 crore transactions at Rs 8.26 lakh crore ($111.2 Bn). The UPI transactions crossed the 6 bn mark in July 2022. PhonePe, GPay and Paytm are leading the UPI game in India with 96.47% of transactions being conducted via these UPI platforms.

PhonePe has been leading the UPI space since the beginning of the year. The Bengaluru-based digital payments app witnessed an 85.5% increase in its revenue from operations, which is recorded at Rs 690 crore in FY21 from Rs 372 crore in FY20. Google Payis the next in line among the other UPI apps, as per the reports dated 15th October 2021.

A month after the launch of UPI123Pay, the UPI transactions surged by over 19% (19.6%), thereby becoming 540 cr transactions, when compared with February 2022’s 452 cr transactions. Furthermore, the transaction value also witnessed a record rise of 16.17%, which was recorded at Rs 9.60 Tn in March from the previous month’s Rs 8.26 Tn.

The real-time payment system, which was commonly referred to as the UPI, recorded 558 cr transactions, worth Rs 9.8 lakh crore in April 2022. The total transactions seen in March 2022 were 540 crores and valued at Rs 9.60 lakh crore. With total transactions for the month worth Rs 4.86 lakh crore, PhonePe stood as the UPI leader, followed by GPay, which materialised Rs 3.39 lakh crore worth of transactions. Paytm, Amazon Pay, and Whatsapp Pay, with Rs 101.65K crore, Rs 6699 crore, and Rs 242 crore, made up the league of 5 of the largest UPI apps that recorded the highest individual transaction values also in April 2022, along with being the most popular UPI apps of the month.

Fast forward to August 8, 2022 reports, PhonePe, Google Pay and Paytm command a whoping 96.47% of the UPI transactions done in the month of July 2022. Here, PhonePe led the other UPI platforms with 47.67% of transactions, followed by Google Pay’s 33.9% and Paytm’s 14.87% shares of the UPI market in transaction count.

UPI Transaction Count in July 2022

Launch of UPI123Pay for the Feature Phone Users

As per the recent surveys, 74 crore mobile users have smartphones while the others out of 118 crore mobile users have feature phones, which are designed for voice calling and texting. This reveals that a significant portion of Indian mobile users uses feature phones. The UPI facility has certainly extended a whole new era of convenient bank account transactions merging multiple banks under one phone number so much so that the RBI thinks that the UPI should also be extended to feature phone users. This is the reason why the Reserve Bank of India governor Shaktikanta Das, has launched UPI for feature phone users, who can use the UPI facility without the need for the internet, which will help over 400 mn feature phone users use the homegrown payments network of India.

UPI, which was easily available to date for smartphone owners and the users of smartphones, was available only via the complicated method of USSD for the others will now be easily accessible with the launch of UPI123Pay on March 8, 2022.

While with the earlier Unstructured Supplementary Service Data (USSD) mode, the feature phone users had to dial *99#, which brought a set of menus before and initiated transactions, the new method will be easier and more cost-effective than the USSD method, which involved numerous chargeable messages.

There are 4 different technologies that will be used in this newly christened method of UPI123Pay. These are:

IVR – The Interactive Voice Response or IVR numbers stand at the core of this process where the users can dial a number and start a secured call from their feature phones. After registering themselves, they can then start their financial transactions without the internet.

Apps – The users can also use apps on their feature phones where they can avail of a wide range of UPI functions, which will help them proceed with the kind of UPI transactions they like, excluding the scan and pay transaction, the work for which is currently in progress.

Proximity Sound-based – Another method that the feature phone users can use involves proximity sound-based technology. This technology relies on sound waves to enable networking. This eventually helps them perform contactless offline and proximity data communication on any device.

Missed calls – The final method that the feature phone users can avail of is the Indian missed call approach. In this method, the users will receive a callback from a standard number, which will let them authenticate and make their transactions smoothly.

Since the launch of UPI123Pay on March 8, 2022, more than 37K users have joined the new initiative and 21,833 successful transactions have happened via the same, as per the written reply received from the Minister of State for Finance, Bhagwat K Karad.

Real-Time Payment Dispute Resolution System

NPCI is planning to launch a real-time payment dispute resolution system for the UPI ecosystem. While announcing the upcoming rollout of the feature, NPCI MD and CEO Dilip Asbe mentioned that the all-new dispute resolution system would remove 80-90% of payment failures in real-time. This feature is all set to be rolled out in September 2022.

DigiSaathi

NPCI or the National Payments Commission of India launched DigiSaathi in India along with UPI123Pay, which is the phone’s feature for real-time payments through UPI. DigiSaathi was brought in as a 24×7 helpline for the UPI123Pay, which will provide them with information on digital payments products and services. This DigiSaathi has been further made available by the NPCI for the users on Whatsapp. DigiSaathi, when it was launched in March 2021, was only available for the users via calling at 14431 and 1800-891-3333, but now they can simply text +91-892-891-3333 to access the same helpline.

The UPI apps are the apps that are designed to follow the UPI mode transactions and are primarily designed to focus on the same. There are several UPI apps that have gained popularity in India due to their ease of use, security, and convenience.

Here are some of the most prominent UPI apps:

PhonePe – This UPI app is owned by Flipkart and has gained popularity due to its ease of use and seamless transactions. It also offers cashback and discounts on various transactions.

Google Pay – This app was formerly known as Google Tez and is one of the most popular UPI apps in India. It allows users to transfer money directly from their bank accounts and has several features such as bill payments, mobile recharges, and more.

BharatPe – BharatPe was founded in 2018 in India. The company offers a range of digital payment solutions for small and medium-sized businesses (SMBs) to accept payments from customers using UPI, debit/credit cards, and more.

BHIM – BHIM is a UPI app developed by the National Payments Corporation of India (NPCI). It allows users to transfer money between bank accounts and has features such as bill payments, balance inquiry, and more.

Amazon Pay – Amazon Pay is a digital wallet service offered by Amazon that allows users to make UPI payments, recharge their mobile phones, pay bills, and more. It also offers cashback and discounts on various transactions.

Whatsapp Pay – WhatsApp Pay was launched in India in 2020. The service allows WhatsApp users in India to send and receive money from their contacts directly within the app.

If you haven’t already started using a UPI app or a Unified Payments Portal (UPI), then it is not something really difficult.

So, if you are wondering about “how to pay using UPI?” then you need not worry!

Here first, you will be needing to register yourself and create a unique UPI ID/VPA. You can register for UPI before using the payments system with the help of any UPI-enabled bank mobile application or third-party application. After the registration is done, you can then start using UPI to send and receive payments. Here are some easy steps to guide you with the process:

Step 1: You need to install either the UPI app or your banking UPI app from Google Play Store or Apple App Store.

Step 2: Then, you need to choose your preferred language, verify your mobile number and eventually select your bank account.

Step 3: Now, you need to create your profile by typing in the basic details like your name, virtual ID, password, and more. This virtual ID that you will create here will stand as your payment address.

Step 4: Next, you will need to go to the option that says Add/Link/Manage Bank Account on the app, and proceed with linking your bank and account number with the virtual ID that you have created in the previous step.

Step 5: After that, you need to create your MPIN (Mobile Personal Identification Number), which is a security code that will be asked every single time you want to continue with a UPI transaction.

Step 6: You would now be successfully registered.

UPI – UPI App Transaction Limit

The NPCI has maintained that while there is no daily limit on the number of transactions, the maximum amount of fund transfer that is possible per day is 1 lac Rupees only. This means that you can pay multiple times to different payees every day, which makes going cash-free a reality. However, when it comes to the BHIM app money transfer limit, then the app allows you to send/receive Rs 40,000 per transaction and Rs 40,000 per day.

Some UPI apps like SBI Pay and WhatsApp Money only allow 20 transactions per day which are also enough for regular use in the everyday life of the users.

UPI – Upcoming Features

UPI Features | Authorized Transactions | Authentication

In the digital world, everyday people are solving new problems through online methods. UPI has identified the opportunities to relieve the users even further and will most likely come up with these improvements in their newer versions.

Pre-Authorized Transactions

Forgetting to pay your bills can be penalized at times and cause you unnecessary trouble. In the UPI, one can pre-authorize the app to draw money for the selected items directly from the bank account before the due dates. This system would also work for EMIs and other bill payments. One would have the ease to customize as per the needs and also put a monthly cap on the automatic payments.

Biometric Authentication

Just like your smartphone unlocks itself through your fingerprint, the UPI app is set to be ‘smarter’. This technology would work on phones which can capture fingerprints or high-quality iris images. The biometric authentication would end the need for MPIN during UPI money transfers.

Error Resolve

As of now, the UPI gives an error if the same mobile number is linked to multiple people’s bank accounts. Commonly, the same mobile number is registered to the account of the husband and wife. The UPI would resolve this problem in the next version of UPI.

UPI – Advantages

UPI (Unified Payments Interface) has several advantages that make it a popular mode of digital payments in India. Here are some of the key advantages of using UPI:

One of the major advantages of UPI is that it is fast, hassle-free, and the cheapest way of money transfer.

UPI is also very fast and a safe medium, while you only need a UPI ID for carrying out a transaction.

It is easy to use as it only requires a single click authentication that involves only two factors.

The user can easily link all their accounts to one ID on the UPI app.

You also have an option of scanning with a QR code to make online and offline purchases.

If the user owns a business, he/she can get payments from clients through this app’s option of collecting payments.

While making payments on UPI, the user does not have to pay any charges as it is free by the Government.

You also get exciting cashback offers.

UPI – Disadvantages

While UPI has several advantages, there are also a few potential disadvantages of UPI system. Here are some of the key drawbacks of UPI:

Sometimes, there can be delays in payments, it takes up to 48 hours for the money to get back to your bank account.

The UPI money transfer limit is currently Rs 100,000, which you can send to anyone through the mobile app.

The UPI pin only consists of four to six digits, which should be elongated for more security.

Another major disadvantage of UPI is that it is very slow in making payments sometimes, but that can be avoided by using faster internet services.

While UPI is gaining popularity in India, it may not be accessible to everyone. Users need to have a bank account and a smartphone with a compatible UPI app to use the service.

Overall, while UPI has several advantages, it is important to be aware of these potential disadvantages of UPI before using the system. By understanding the limitations of UPI, users can make informed decisions about when and how to use this payment system.

UPI – Challenges

The UPI apps and the sector, as a whole, have faced many challenges already overcoming which it is treading on the path of glory. One of the major challenges of the UPI industry was when the world witnessed one of the most dreadful diseases of modern times in the form of the coronavirus pandemic.

Due to the lockdown imposed to contain the spread of COVID-19, UPI has recorded transactions of less than one billion for the month of April after 12 months of constant growth. This is the first time in the past seven months that UPI volume went below the one billion mark. According to the National Payments Corporation of India (NPCI), UPI has registered 0.99 billion transactions amounting to Rs 1,51,140 crore(Rs 1.51 trillion).

Unified Payments Interface (UPI) is an instant payment system developed by the National Payments Corporation of India (NPCI), an RBI-regulated entity. UPI can be used through various apps like Google Pay and PhonePe to make direct payments from one bank account to another.

The lockdown imposed by the government due to COVID-19 has caused everything to shut down or be just semi-operational. The coronavirus outbreak has devasted many sectors of human life, let it be the financial sector, industrial sector, etc. resulting in an economic crisis. Yet, India’s success with a unified payments interface (UPI) has continued to bring essential services to consumers amid the lockdown as well.

Though the government was able to transfer the relief money through UPI in the bank accounts of crores of Indians, UPI witnessed a 20.8% drop in volume and a 26.7% fall in value as compared to the month before. As corona effect, UPI had registered a little drop in payments volume in March resulting from 1.25 billion transactions worth Rs 2,06,462 crore or Rs 2.06 trillion.

Moreover, along with UPI, NPCI’s real-time payments service IMPS has also registered a sharp fall in volume as well as the value of transactions. In April, IMPS processed 122.47 million payments worth Rs 1,21,140.79 crore which is almost half of the previous month. In the previous month i.e. March, the figure was 216.82 million transactions worth Rs 2,01,961.70 crore.

The decline is shocking as in February 2020, the RBI governor, Shaktikanta Das, highlighted that digital payments accounted for almost 97% of the daily payment system transactions in terms of volume. He also mentioned that digital payments had accelerated by 50% in terms of volume in the last five years.

However, UPI body NPCI’s CEO Dilip Asbe said, “For the last five years, the number of transactions of UPI has been growing continuously month-on-month. But now there has been a slight drop in the volume due to the lockdown. The drop in volumes is due to near-zero restricted spends such as on e-commerce, travel, and similar online platforms. We expect volumes to pick up soon.”

Reasons behind the drop in transactions

It was anticipated that a nationwide lockdown to curb the spread of the Covid-19 pandemic would affect the digital payment volumes. However, financial experts were assured that digital payments will not get affected adversely but rather continue to grow as people would rely on digital transactions to avoid physical contact.

During the initial days of the lockdown, e-commerce, food tech, grocery as well as other online platforms were unable to operate. This led to a gradual fall in transactions but later the government allowed essential services to continue. Moreover, payments to PM-CARES via UPI have been the driving force behind UPI’s growth, which is still a 20.8% drop and these numbers are only in a few million.

Yet, transactions did not come back to normal as the government only allowed transactions on essentials. Hence, a majority of e-commerce services are still waiting for government orders. Soon, the government is likely to relax the norms for e-commerce platforms and allow them to deliver non-essential goods as well.

According to payment gateway Razorpay’s digital transaction report, for the month of April, the transactions in logistics have dropped by 96%, the travel sector has declined by 87%, food, and beverage by 68%, and groceries by 54%. In the last 30 days, transactions in cities like Ahmedabad, Mumbai, and Chennai took a hit of 43%, 32%, and 25% respectively. The report recorded transactions between when the lockdown was announced.

Razorpay’s report also stated that UPI emerged as the most popular digital payment method from March 24 to April 23, with 43% of the total transactions during the period. It was followed by card payments with 39% and net banking with 10%. However, compared to the previous month, transactions through UPI declined by 37%, cards by 30%, and net banking by 28%.

Steps taken to deal with the drop

Though the situation worsened throughout the lockdown, NPCI seemed prepared to handle the lockdown. CEO Dilip Asbe said that NPCI can have multiple sessions and had a spare capacity to handle the demand. In order to ensure that everything keeps running smoothly, around 5% of the NPCI’s workforce travelled to the office.

NPCI has already devised a plan for the situation with due consideration of all the factors. Asbe said that NPCI has received complaints from some businesses about delays in cheque clearing. He added that there could be issues on the last mile. “While we are in touch with banks, there might be some issues with uploading because of the lockdown. These issues might be hard to resolve now as most of the workforce isn’t available now,” said he. However, Asbe also mentioned that the main objective there was to keep employees safe. If they are safe, the operations can be managed. “There are things we cannot disclose, but there is enough backup in case something goes wrong,” he added,

The government also used the UPI technology for facilitating the transfer of money in the bank accounts of beneficiaries within a day under the Pradhan Mantri Garib Kalyan Yojana (PMGKY). He further noted that besides this transfer of relief funds, the government has been using UPI for transferring monetary perks in various schemes such as Ujwala and MNREGA.

After the success of the implementation of UPI in these schemes, many state governments then relied on UPI technology to transfer funds under various schemes. Madhya Pradesh government recently transferred some relief money to the accounts of lakhs of construction workers. PM Narendra Modi had also urged people to go for digital payment to ensure safety from the infection.

Major Challenge for the Stakeholders

India’s free payments system, UPI is not actually free for all. It is simply free for the users and merchants but the stakeholders have to pay a price for it. As per RBI, the costs incurred by the stakeholders in a peer-to-merchant (P2M) UPI transaction with an average order value of ₹800 is nearly ₹2 i.e, 0.25% of the transaction value. So, for example, if 16 lakh crore INR worth of transactions have occurred in the previous year on the UPI that means it costs roughly 4,000 crore INR ($500 million) to banks, NPCI, and the payment service provider.

UPI – Transaction Rules from January 2021

The Reserve Bank of India (RBI) has come up with the ”positive pay system” for cheque payments. This system is introduced in order to keep a check on banking fraud. According to the positive pay system, the user is required to re-confirm their key details for payments that go beyond 50,000. The user, however, has a choice to use this system.

UPI offers several benefits over other payment systems such as NEFT, RTGS, and IMPS. Here are some of the key advantages of UPI:

UPI vs NEFT

Both the platforms are known to have pros and cons. UPI facilitates instant transfer for free, whereas it can only transfer Rs 1 Lakh per day. NEFT on the other hand allows the user to transfer funds from any bank branch to any individual having an account with any other bank branch in India. A disadvantage of NEFT is that the cost is higher than UPI and it takes about 12 hours for one NEFT transfer.

UPI vs RTGS

UPI transactions are fast, simple to use, and free of charge, and are ideal for future payments, loan repayment, or credit card payments. Whereas the Real Time Gross Settlement (RTGS), is said to be of high value and needs to be processed in real-time, and is ideal for the transfer of Rs 2 lakhs and above.

UPI vs IMPS

The Immediate Payments Service (IMPS), is an instant interbank electronic fund transfer service that helps the user to access your bank account and transfer funds immediately and securely. However, with UPI the user can pay directly from a bank account to different merchants, both online and offline, without the hassle of typing your credit card details, IFSC code, or wallet passcodes.

Conclusion

UPI is a game-changing payment system that has made digital payments accessible and affordable for millions of people in India. Its ease of use, low cost, and instant transfer capabilities have made it the preferred payment option for individuals and businesses alike, and it is set to revolutionize the way people make payments in India for years to come.

With all the knowledge of UPIs, it is safe to say that people are encouraged to take a step toward going cash-free. Many other improvements are expected in the newer updates so it would not hurt to make the shift and keep up with the new digital times of managing funds.

FAQs

What is the use of UPI?

UPI or Unified Payments Interface is an instant real-time payment system created by National Payments Corporation India, which likewise implies that the Reserve Bank of India controls it.

What are the services of UPI?

The services of UPI are Cash-free functioning, Security, Real-Time Fund Transfer, a Cheaper Alternative to POS machines, and One UPI app that works for all bank accounts.

What is the Unified Payment Interface meaning?

Unified Payment Interface refers to a system that empowers the users with multiple bank accounts under a single mobile application for effective transactions. It is an all-in-one interface for payments, hence “unified”.

What are the charges for UPI?

UPI is free of charge at present. However, at the meeting of banks with NPCI on February 14, 2020, it has been decided that UPI transactions are free for up to 20 transactions per person.

What is the current UPI transfer limit?

Currently, the UPI transfer limit is set to Rs 1 lakh, as decided by the NPCI.

Can the UPI app for the current account be used?

The UPI app for current accounts can easily be used both by merchants and consumers and they work just as well as the UPI for savings accounts.

What are UPI transaction charges?

At present, the UPI transfer limit per UPI transaction is ₹1 Lakh.

Is UPI safe?

Yes, UPI is safe and secure as it has a number of measures that ensure its safety.

Is a debit card necessary for UPI?

Yes, the debit card is mandatory to set the UPI pin.

How to use UPI to transfer money?

UPI can easily be used to transfer money, in which a user needs to have his/her bank account connected along with a working UPI ID and a phone number that is linked with the bank account.

No, UPI is a domestic payment system and can only be used to transfer money within India.

Which banks support UPI?

Most major banks in India support UPI, including State Bank of India, HDFC Bank, ICICI Bank, Axis Bank, and others.

How does UPI work?

UPI allows users to link their bank accounts to a mobile app and make payments directly from their account. Users can transfer money to other bank accounts by using the recipient’s UPI ID or mobile number.

What should I do if my UPI transaction fails?

If your UPI transaction fails, you can try again after a few minutes. If the problem persists, you can contact your bank’s customer service for assistance.

Can I link multiple bank accounts to UPI?

Yes, you can link multiple bank accounts to UPI. You can switch between accounts while making payments or choose a default account for transactions.

Is there any disadvantages of UPI?

Yes, there are some disadvantages of UPI. It requires a stable internet connection and a smartphone to make transactions, and it may not be widely accepted in all merchants and stores.

The National Payments Corporation of India (NPCI) is an umbrella organization for operating retail payments and settlements systems in India. It is an initiative by the Reserve Bank of India (RBI) and the Indian Bank Association (IBA) under the provisions of the Payment and Settlement Act, 2007, for creating a robust infrastructure in India for any kind of retail payments and settlements. Created with an intention to provide a fair infrastructure to the entire Indian Banking system, it is Not-for-Profit in nature and has made it possible to create payments both physically as well as electronically.

National Payments Corporation of India

Management Team

Under the non-Executive Chairmanship of Mr. Biswamohan Mahapatra, a veteran who has served 33 years at RBI, the organization is owned by a consortium of major banks. The Board of Directors consists of nominees from the Reserve Bank of India and from nine core promoter banks.

There are nine main promoter banks in India which are:

The corporation portfolio currently includes various services such as:

Unified Payments Interface (UPI)

Unified Payments Interface

Unified Payments Interface (UPI) is a system that powers multiple bank accounts into a single mobile application (of any participating bank), merging several banking features, seamless fund routing, and merchant payments under a single hood. It also caters to the “Peer to Peer” collect request which can be scheduled and paid as per requirement and convenience.

With the above context in mind, NPCI conducted a pilot launch with 21 member banks on 11th April 2016 by Dr. Raghuram G Rajan (ex-Governor of RBI) at Mumbai. Banks have now uploaded their UPI enabled Apps on Google Play store.

The Participants of the service include the payer, payee, remitter bank, beneficiary bank, NPCI, bank account holders, and merchants. Some examples of UPI apps that you may already be using are PayTm, BHIM, PhonePe, Axis Pay, and many more.

RuPay

RuPay

RuPay, which literally translates to Rupee and Payment merged together, is a domestic card scheme launched by NPCI in 2012 to fulfill the Reserve Bank Of India’s desire to have a domestic, open loop, and multilateral system of payments in India . In India, 90% of credit card transactions and almost all debit card transactions are domestic; however, the cost of transactions remained high due to the monopoly of foreign gateways like Visa and Mastercard.

RuPay facilitates electronic payment at all Indian banks and financial institutions. NPCI maintains ties with Discover Financial to enable the card scheme to gain international acceptance.

Lower costs and affordability, customized product offering for Indian customers, interoperability between payment channels and products, and protection of information related to Indian consumers are just some of the advantages of RuPay as claimed by NPCI.

RuPay Contactless

It is a contact-less technology feature that allows cardholders to wave their card in front of contact-less payment terminals without the need to physically swipe or insert the card into a point-of-sale device. This is an EMV-compatible, “contactless” payment feature similar to Mastercard Contactless, Visa Contactless and the ExpressPay, using RFID technology. All three use the same symbol. Contactless can currently be used on transactions up to ₹2000.

RuPay Contactless

NPCI developed RuPay Contactless’s specifications are open standards, interoperable, scalable, and can be adopted by all card schemes. RuPay Contactless (Transit as well as Retail) offers the unique proposition of one card for all payments. This card can be used for transit payments (bus, metro,cab etc.), toll, parking, small value offline retail payments, as well as normal day to day retail payments.

One Card Many Benefits

Bharat Interface for Money (BHIM)

Bharat Interface for Money

Bharat Interface for Money (BHIM) is a mobile application that lets you make quick payment transactions using Unified Payment Interface (UPI). You can make instant bank-to-bank payments and Pay and collect money using your mobile number or Virtual Payment Address (UPI ID). More than 125 lakhs citizens have been using the BHIM app since 2017.

Unlike mobile wallets (PayTM, MobiKwik, mPesa, Airtel Money, etc) which hold money, the BHIM app is only a mechanism which transfers money between different bank accounts. Transactions on BHIM are instantaneous and can be done 24/7 including weekends and bank holidays.

Users can create their own QR code for a fixed amount of money, which is helpful in merchant-seller-buyer transactions. Users can also have more than one payment address. If the 12-digit Aadhaar number is listed as a payment ID, the BHIM app will not require any biometric authentication or prior registration with the bank or Unified Payment Interface (UPI).

At present, there is no charge for transactions from ₹1 to ₹1 lakh. The minimum transaction amount should not be less than ₹1. A maximum of 20 transactions are allowed in a day. Some bank might however levy a nominal charge as UPI or IMPS transfer fee. Currently the fund transfer limit has been set to a maximum of ₹20,000 per transaction, and a maximum of ₹40,000 per day.

The BHIM app currently supports 13 languages (including English), though there are 22 official languages of India (excluding English) under 8th Schedule of Constitution of India. In near future, BHIM App is expected to support all 22 official languages of India along with other regional languages which are spoken widely next to the scheduled languages.

Immediate Payment Service (IMPS) is an instant payment inter-bank electronic funds transfer system in India. IMPS offers an inter-bank electronic fund transfer service through mobile phones. Unlike NEFT and RTGS, the service is available 24/7 throughout the year including bank holidays.

In 2010, the NPCI initially carried out a pilot for the mobile payment system with 4 member banks (State Bank of India, Bank of India, Union Bank of India and ICICI Bank), and expanded it to include Yes Bank, Axis Bank, and HDFC Bank later that year. IMPS was publicly launched on November 22, 2010. Currently, 53 commercial banks, 101 Rural/District/Urban and cooperative banks, and 24 PPIi have signed up for the IMPS service.

The participants of IMPS include the remitter (sender), beneficiary (receiver), banks, and National Financial Switch – NPCI.

You can avail the fund transfer service:

Using Mobile number & MMID (P2P).

Using Account number & IFS Code (P2A).

Using Aadhaar number (IMPS).

National Electronic Toll Collection (NETC)

National Electronic Toll Collection

The National Payments Corporation of India (NPCI) has developed the National Electronic Toll Collection (NETC) program to meet the electronic tolling requirements of the Indian market. It offers an interoperable nationwide toll payment solution including clearing house services for settlement and dispute management.

Interoperability, as it applies to National Electronic Toll Collection (NETC) system, encompasses a common set of processes, business rules, and technical specifications which enable a customer to use FASTag as a payment mode on any of the toll plazas irrespective of who has acquired the toll plaza.

FASTag is a device that employs Radio Frequency Identification (RFID) technology for making toll payments directly while the vehicle is in motion. FASTag (RFID Tag) is affixed on the windscreen of the vehicle and enables a customer to make toll payments directly from the account which is linked to FASTag.

FASTag offers the convenience of cashless payment along with benefits like savings on fuel and time as the customer does not have to stop at the toll plaza. The program is currently live on 415+ toll plazas across the country. As per NHAI, FASTag has unlimited validity. 7.5% cashback offers were also provided to promote the use of FASTag. Dedicated Lanes at some toll plazas have been built for FASTag.

*99#

*99#