On September 26, HDFC Bank Limited declared that the Dubai Financial Services Authority (DFSA) had formally instructed its Dubai International Financial Centre (DIFC) office to restrict the onboarding of new customers.

The DIFC branch is prohibited from approaching or doing business with new clients who have not finished the onboarding procedure by that date, according to the Decision Notice of September 25, 2025. The limitations apply to a variety of financial services operations, such as custody-related services, investment transaction structuring, credit arrangement or advice, and financial product advice.

DIFC Prohibited From Engaging Financial Promotions

DIFC is not allowed to onboard new customers or run financial promotions. Clients who have previously received financial services but were not properly onboarded may still be served, and current clients may continue to receive services.

Until the DFSA publishes a written revision or repeal, the directive, which went into force on September 26, 2025, will stay in effect. Concerns about improperly onboarded financial services for clients and problems with the branch’s onboarding procedures were the core reasons behind the move, as mentioned by the DFSA.

Response from HDFC

No major financial repercussions are anticipated because HDFC Bank indicated that the DIFC Branch business is not relevant to its overall operations or financial situation. 1,489 customers, including joint holders, had been onboarded to the branch as of September 23, 2025.

The bank declared that it has already taken the required actions to adhere to the instructions and that it is dedicated to assisting the DFSA in its current investigation as well as to promptly resolving and addressing the regulator’s concerns.

What Forced DFSA to Take Stringent Action Against HDFC?

The two-year-old scandal over the purported mis-selling of high-risk Credit Suisse additional tier-1 (AT1) bonds serves as the context for the regulatory action. Through its UAE operations, which included account booking with its Bahrain branch, relationship management by employees at its Dubai representative office, and advising from DIFC authorities, the bank was accused by investors of marketing the products.

The effective onboarding of clients in the DIFC, a jurisdiction with distinct financial regulations and a more stringent environment for “professional clients”, was investigated.

When the AT1 bonds were written down in 2023 amid Credit Suisse’s collapse, a number of non-resident Indian investors suffered significant losses and were subject to margin calls on leveraged positions.

Quick

Shots

•The restriction took effect on September

26, 2025, as per a Decision Notice issued on September 25, 2025.

•DIFC branch cannot onboard new

customers, approach potential clients, or run financial promotions.

•Current customers will continue

receiving services; improperly onboarded clients can still be served.

•Regulatory action linked to concerns

over improper onboarding procedures and mis-selling of high-risk Credit

Suisse AT1 bonds.

The globe is slowly paving its way towards a cashless society. From invoices to cards and now to mobile wallets, this significant transformation has reduced the weight of bulky wallets. We can pay for any product, transfer money, make bill payments, and almost everything to do with money from the comfort of our home. Payment wallets in India have made online transactions of money easy and fast, with their one-tap feature and quick processing, all at one go.

A mobile wallet is a digital wallet that uses a bank account or credit/debit card to make payments seamlessly while securing the data of the user. They are designed to enable secured transactions with a hassle-free process, with reduced fraud. This method of online payment has proved to be more economical as compared to other physical wallets. These wallets are easily accessible as well from the play-store or app store.

India ranks 2nd highest in the Asia Pacific for digital payment adoption.

Digital payments in India are set to account for 71.7% of the total payments volume by 2025, leaving cash and cheque transactions at 28.3%, according to a report by a US-based payment systems company.

Since Demonetization hit the Indian Economy harshly, the Government promoted the use of these wallets and since then the user base of these e-wallets has been increasing significantly. Many digital wallets by the Indian Government has been given to citizens like UPI, BHIM, Aadhaar Pay and Payment Banks.

How Does A Mobile Wallet Work?

Start by downloading the mobile app of your choice onto your smartphone. Then, load the card information you want to store, from debit, and credit cards to loyalty cards and even coupons.

When you want to make a purchase with your mobile wallet, you can either:

Choose your app and select a card at the checkout screen when you’re shopping online with your smartphone.

Tap your phone to a digital payment-enabled terminal at participating merchants when checking out. Mobile wallets use what is called a Near-Field Communication (NFC) chip that lets you use contactless payment with a physical card.

Types Of Mobile Wallets In India

Closed PPI

Semi-Closed PPI

Open PPI

Definition

Issued by a company to buy goods and services only from that company; it does not permit cash withdrawals or redemptions.

Can be used to buy goods and services from merchants that have a contract with the Issuer to accept the payment instrument; it does not permit cash withdrawals or redemptions.

Allows a user to buy goods and services, withdraw cash at ATMs or banks, and transfer funds.

KYC Requirement

No KYC required

No As Such compulsion for KYC

KYC is Required

Examples

Makemytrip Wallet

Mobikwik

PayTM Payment bank

Are Mobile Wallets Secure?

One security concern when using a mobile wallet is losing your phone or having it stolen. That’s why it’s smart to use something like two-factor authentication, which could include setting up a personal identification number or a fingerprint requirement to unlock your phone.

You can also protect your data by installing apps that will help you locate your phone if you lose it or remotely wipe the data so a thief can’t reach the sensitive information in your phone. If you see any suspicious or unauthorized charges on your account(s), it’s a good idea to immediately change your password and call your bank to let them know.

Paytm is one of the largest online commerce platforms in India offering its customers a mobile wallet to store money and make quick transactions. It is considered by many the best mobile app in India. Paytm was launched in 2010 and basically works on a semi-closed model. Users can load money and make payments to merchants. E-Commerce is an added benefit of it, but despite that, you can make bill payments, transfer money, and avail yourself of services of entertainment, travel, and cashback. Payments through Paytm are accepted almost everywhere.

Google Pay

Mobile Wallet

Google Pay

Founded

2017 (India launch)

Total Downloads

1B+ (on Google Play Store)

Google Pay – Best Wallet Apps in India

It was formerly known as Tez andfor obvious reasons, it gained its user base really quick, in spite of being a late entrant in the mobile wallet industry. It is the best online payment app or best money transfer app with cashback. Google Pay works with your existing bank account, which already means that your money is safe with the bank and no issues with recharging your wallet every month. Send or receive money from your friend directly to your bank account. There is also no such issue regarding KYC making it all the more popular.

BHIM (Bharat Interface for Money) is another best mobile wallet in India. It is a mobile wallet app developed by the National Payments Corporation of India (NPCI), based on the Unified Payment Interface (UPI). Launched in December 2016, it is intended to facilitate e-payments directly through banks. Users register their bank account with BHIM and set a UPI PIN for the bank account. It can be used by both Axis Bank users as well as other bank users. The Mobile Number is then the permanent address and they can start transacting. User can pay their friends, family and merchants with the tap of a button.

PhonePe

Mobile Wallet

PhonePe

Founded

2015

Total Downloads

500M+ (on Google Play Store)

PhonePe – Best Payment Wallet in India

PhonePe was launched in 2015 and is now a part of Flipkart. From UPI Payments to mobile recharges, and money transfers to online bill payments, this can be done easily on PhonePe. With a good user interface, PhonePe has offered the safest and fastest online transaction experience in India.

Mobikwik

Mobile Wallet

Mobikwik

Founded

2009

Total Downloads

50M+ (on Google Play Store)

MobiKwik – Mobile Wallet in India

Mobikwik was launched in 2009 with its key proposition in Recharge and Bill payments. Mobikwik is one of the independent mobile payment networks that has a user base of 32 million. This e-wallet lets its users add money using debit cards, credit cards, net banking, and even doorstep cash services. One of the unique features Mobikwik has offered its users is ‘expense tracker’, basically which allows users to set a budget for expenses via SMS data to analyze and control the expenditure.

This application was launched by the State Bank of India to let users transfer money to other users, pay bills, recharge, book tickets, shop, and travel. This is one of the top mobile wallets in India and has offered its mobile wallet services in 13 languages the best part is, that it is also available to non-SBI customers. It taps into the special feature where-in it allows its users to set reminders for dues, and money transfers, and view mini-statement for the transactions done already.

Citi MasterPass was launched recently by Citi Bank India and MasterCard. This is one of India’s first global outreach in terms of digital wallets for faster and more secure shopping. Citi Bank debit and Master card customers become the first in this country to shop at more than 250,000 e-commerce merchants. It has ensured fast checkout with a single tap and stores all credit, debit, prepaid, and shipping details.

ICICI Pockets

Mobile Wallet

ICICI Pockets (ICICI Bank)

Founded

2016

Total Downloads

5 M+ (on Google Play Store)

ICICI Pockets – Mobile Wallet in India

It’s one of the best mobile wallets in India. It has provided the convenience of using any bank account in India to fund your mobile wallet and pay for transactions. It basically uses a virtual VISA card that enables its users to transact on any website or mobile application in India and provides exclusive deals or packages from associated brands.

HDFC PayZapp

Mobile Wallet

HDFC PayZapp

Founded

June 2015

Total Downloads

10M+ (on Google Play Store)

HDFC PayZapp – Best Wallet in India

PayZapp is a complete payment solution by HDFC Bank which has a one-tap feature for easy payment. Not only does it let you recharge your phone or send money but also your DTH and data cards, pay utility bills, and compare and book flight tickets, trains, hotels and shops.

Amazon Pay

Mobile Wallet

Amazon Pay

Founded

2007 (Global), 2011 (India)

Total Downloads

500M+ (on Google Play Store)

Amazon Pay – Mobile Wallet in India

Owned by Amazon, this online payment processing service was launched in 2017 in India (globally- 2007). Amazon Pay has focused its customers more on Amazon and so it gives its users the option to pay with their Amazon accounts on external merchant websites, including apps like BigBazaar etc. With Amazon Pay, you get to shop on Amazon with a number of cashback and discounts with fast shipping services. Recently, Amazon Pay got tied up with fintech companies, such as Zest Money to enable no-cost EMI payment options. The application has also made it easier for buyers to buy products on Amazon and pay later via affordable monthly instalments.

Samsung Pay

Mobile Wallet

Samsung Pay

Founded

August 20, 2015

Total Downloads

100M+ (on Google Play Store)

Samsung Pay – Mobile Wallet in India

Samsung Pay is a digital wallet service owned by Samsung, it was launched on the year 2015. It is considered one of the best payment processing services for contactless payments. Samsung is accepted in almost every store, wherever credit and debit cards can be used it also offers Cashback. With the help of Samsung pay, the transaction between merchants and payers are possible without the exchange of bank and card information. Samsung Pay accepts all kinds of card readers like magnetic stripes, EMV and others,

Apple Pay

Mobile Wallet

Apple Pay

Founded

October 20, 2014

Total Downloads

Not publicly disclosed

Apple Pay – Mobile Wallet in India

Owned by Apple Inc., Apple Pay is a digital wallet service, which was launched in the year 2014. Major credit and debit cards are supported in Apple Pay, it also provides extreme security through touch and face id. Anyone owning an apple device can use Apple Pay on them for making payments. The card information is kept confidential while making payments. Apple Pay currently is available in more than 60 countries.

WhatsApp Pay

Mobile Wallet

WhatsApp Pay

Founded

February 2018 (India pilot)

Total Downloads

Over 1 billion (WhatsApp Messenger)

WhatsApp Pay – Best Wallet App in India

Launched in the year 2018, WhatsApp launched the chat payment service to allow users to complete any kind of transaction through WhatsApp. The secure way of the transaction enables people to make payments easy just like sending a message on WhatsApp. WhatsApp Pay has also been providing some great features like Cashback to attract more customers. This UPI-based payment service provides the option of sending and receiving money.

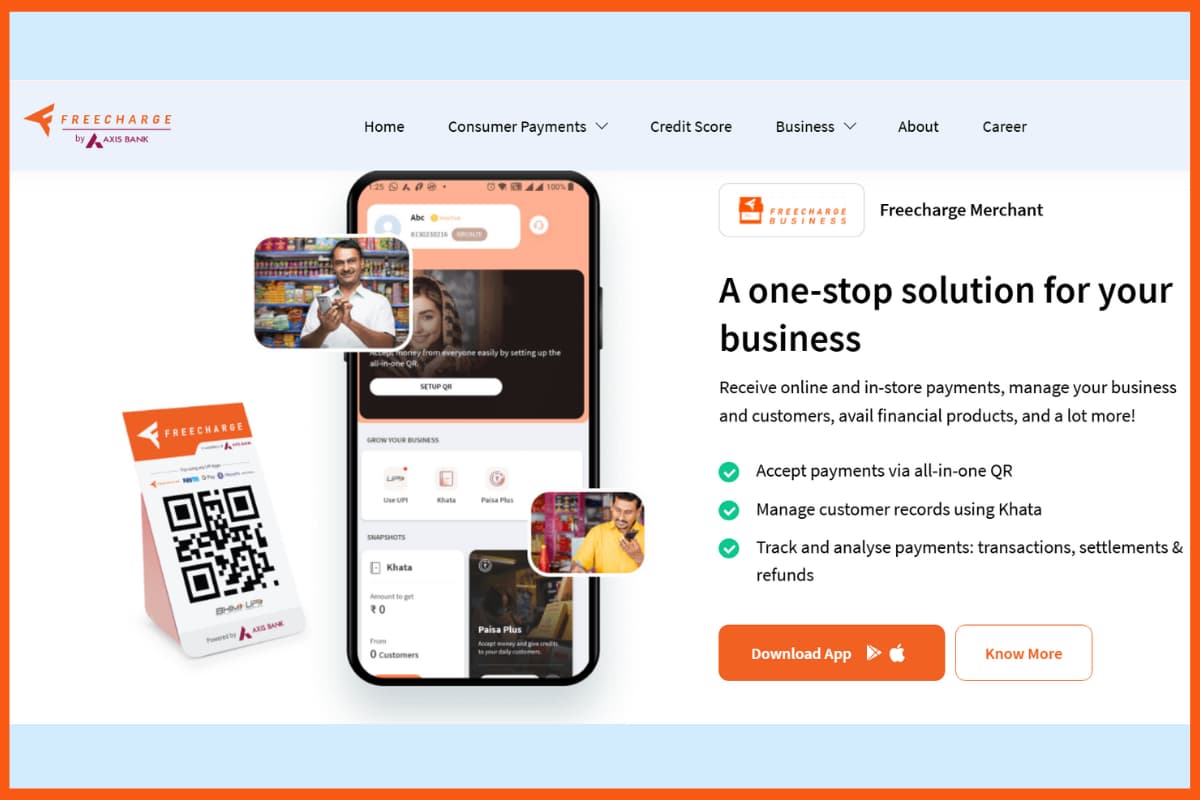

Freecharge

Mobile Wallet

Freecharge

Founded

August 2010

Total Downloads

50M+ (on Google Play Store)

Freecharge – Mobile Wallet App in India | Digital Wallets in India

Freecharge is a wallet app that is easy and fast to use for payments. You can recharge your phone, pay bills, and send money to friends. It also works with UPI payments and is popular for online shopping.

Freecharge gives good cashback offers and discounts, which users like. It lets you split bills, so sharing expenses with friends or family is simple. Many stores accept Freecharge for payments both online and in shops.

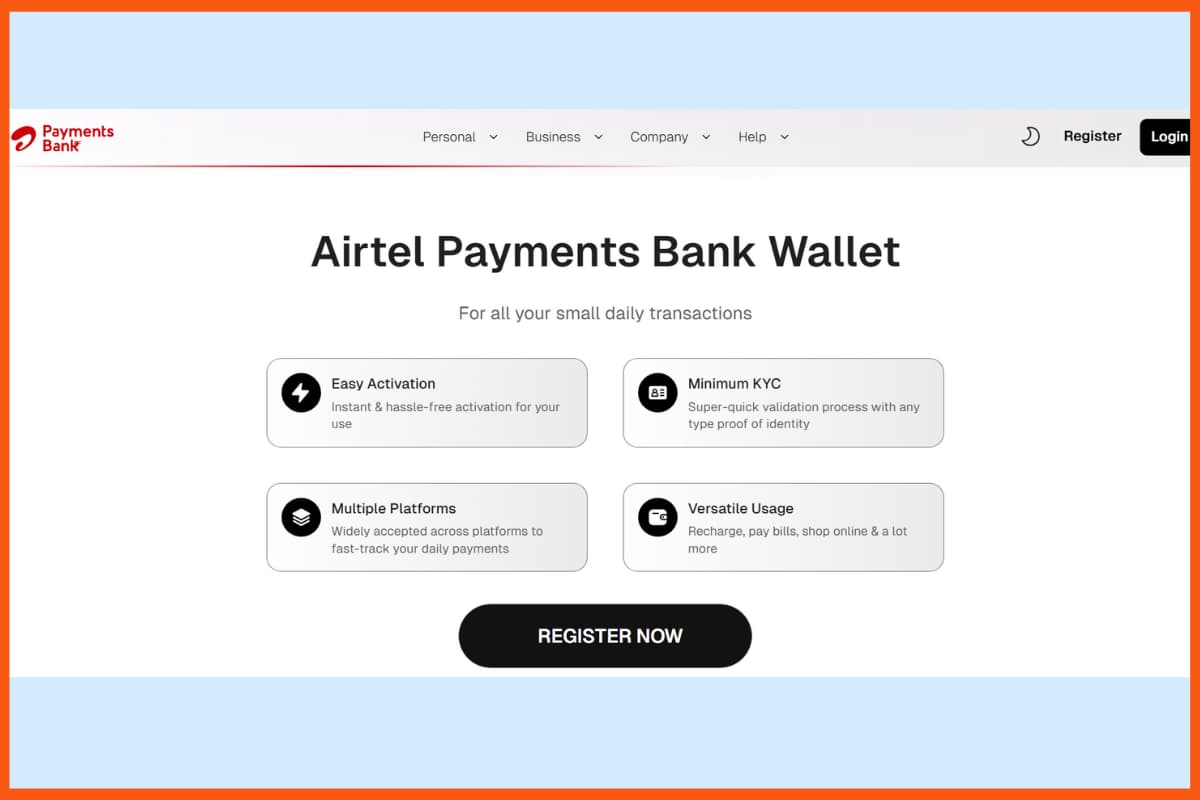

Airtel Money

Mobile Wallet

Airtel Money

Founded

2012 (initial launch)

Total Downloads

50M+ (on Google Play Store)

Airtel Money – Best Digital Wallets in India

Airtel Payments Bank Wallet is a special service that mixes a mobile wallet with digital banking. You can pay bills, recharge your phone, or send money using UPI. It gives you more interest on your balance than regular savings accounts.

The wallet works well with Airtel services and gives special discounts to Airtel users. You can also withdraw cash from ATMs without a card, using QR codes. It is safe and trusted for your digital banking needs.

Mobile Wallets’ Usage in India

Advantages Of Mobile Wallets

Mobile wallets got popular due to the advantages it offers. Here are listed some of the advantages of using mobile wallets in India

1. One-Click Pay

This is one of the most convenient ways to make payments since the user can pay via such wallets. The mobile wallet takes the information from your card (credit/debit) and makes payments directly or adds money to your wallet. This has offered easy accessibility to users.

2. Multiple Features and Uses

With easy accessibility, it can be used anytime, anywhere. These mobile wallets can be used in a jiffy, it’s just that you need a proper internet connection for your device. Also, your single mobile wallet account can be accessed on any of your devices like laptops, PC, or smartphones with authenticated verification.

3. Robust Security Features

Mobile wallets have tried hard to provide extensive safety and security. Almost more than half of the population has shifted from leather wallets to e-wallets for the protection of their money. Mobile wallets have also reduced the chance of daily theft or losing cash.

4. Several Benefits

They come up with several other benefits like loyalty programs, cashback, rewards, shopping benefits, and many more so that their customers stay happy. Simultaneously, users can also save money through heavy discounts and offers.

How funds in a Mobile Wallet are spent in India

Mobile Wallet vs Digital Wallet

Mobile Wallet

Digital Wallet

Definition

Mobile wallets are payment apps housed on mobile devices, like smartphones and wearables.

Consumers using digital wallets, may or may not interact with them on their smartphones.

Uses

Consumers mostly use a mobile wallet for in-person transactions.

Consumers mostly use a digital wallet for online shopping or purchases.

Examples

Some of the most popular mobile wallets are Apple pay, Samsung pay, etc.

Some of the most popular digital wallets are Paytm, Paypal, etc.

Limitations Of Mobile Wallets In India

Besides the advantages Mobile wallets in India offer in the payment service industry, it has some limitations which are listed below.

A limit is set on the amount that you can deposit in your mobile wallet. For instance, Paytm allows the amount of ₹20,000 in its wallet.

The number of merchants listed or having a tie-up with these wallets is limited. In that case, you would always need to carry some cash in urgency.

Sometimes, Infrastructure issues stand for a lot of lost transactions or common ‘server down’ problems.

Few times, some fraud calls can also cause a possibility of a mobile theft where your personal information is compromised.

One of the major concerns is that a person needs a smartphone to make online transactions possible and that too, with good internet connectivity. This alone has stood a major limit to many poor families, who still carry cash in their pockets.

More than 40% of respondents used a smartphone in India.

While these large numbers and large user bases indicate the growing need for secure, faster, and efficient transaction methods for the online marketplace. Regardless of what we’ve seen and read, top e-wallets in India have outweighed its concerns. The use of e-wallets has constantly increased due to obvious reasons and its surprising offers. Mobile wallets continue to gain prominence in smartphones and laptops across the globe and have dominated the discussions of new ways to pay.

A digital wallet sometimes called an e-wallet, is a service that allows you to pay for things, usually through a mobile phone app. It also stores a number of other items a traditional wallet would hold, such as a driver’s license, gift cards, tickets for entertainment events, and transportation passes.

What is a digital wallet used for?

A digital wallet (or e-wallet) is a software-based system that securely stores users’ payment information and passwords for numerous payment methods and websites. By using a digital wallet, users can complete purchases easily and quickly with near-field communications technology.

Which is better PhonePe or Google pay or Paytm?

Experts suggest that all three digital transaction apps, more or less, are equally secure. While Google’s brand image definitely does some good to Google Pay. Paytm, and PhonePe continue to be easy picks for others due to their many features.

How to get PhonePe cashback?

Steps to get PhonePe cashback:

Download PhonePe App.

Do the needful for PhonePe Login / Signup.

Set Your Virtual Payment Address (VPA)

Click On Bank Accounts From Menu &Link Your Bank Account.

Recharge Your Mobile.

Which Mobile wallet has highest market share in India?

Paytm has the largest market share in India followed by PhonePe and GooglePay.

What is the difference between Paytm vs PhonePe?

Paytm Allows transactions across multiple modes like wallets, UPI, and payment gateway. PhonePe has started its wallet service but it is widely used for its UPI-based transaction which doesn’t charge you for any transaction.

Which wallet app is best in India or write a few Mobile wallet examples?

Four significant public sector banks have changed their lending rates in response to the Reserve Bank of India’s (RBI) recent move to lower the repo rate by 50 basis points, which reflects the central bank’s monetary easing stance.

In the face of persistent difficulties, the action seeks to boost credit expansion and sustain economic activity. One of the first banks to lower its repo-linked lending rate (RLLR) by 50 basis points was Bank of Baroda, which did so on June 7, 2025, when it dropped to 8.15%.

Following suit, Punjab National Bank (PNB) maintained its Marginal Cost of Funds based Lending Rate (MCLR) at 8.35% but reduced their RLLR by 50 basis points to 8.35% as of June 9. Likewise, on June 6, Bank of India reduced its repo-based lending rate by 50 basis points to 8.35%.

UCO Bank reduced its MCLR by 10 basis points over a range of tenures, with the one-year MCLR now at 9%. It also reduced its RLLR by 50 basis points starting on June 9 and now stands at 8.30%.

Beginning on June 7, HDFC Bank, a prominent private sector lender, likewise lowered its MCLR by 10 basis points throughout all tenures. The overnight and one-month MCLR rates decreased to 8.9% as a result of this modification.

Bringing a Big Smile on the Face of Existing Borrowers

Floating-rate loans, which are required by RBI regulations to be adjusted in accordance with the benchmark repo rate, are immediately impacted by the RBI’s repo rate drop. Lower interest rates will therefore be an immediate benefit for current borrowers with floating-rate loans.

However, because banks are anticipated to adjust the spreads they charge over the repo rate in order to remain profitable, new borrowers might not fully benefit from the rate decrease. For instance, Bank of Baroda’s home loan rates for first-time borrowers now start at 8% following the change.

Due to this selective adjustment, current borrowers stand to benefit more than new ones, as many of them previously obtained loans at reasonable rates as a result of market competition. A number of public sector banks, including Union Bank of India, Bank of India, Bank of Maharashtra, and Central Bank of India, were providing home loans with interest rates as low as 7.85% for loans up to INR 30 lakh prior to the RBI rate drop.

Home loans were available at 7.90% from other lenders such as Canara Bank, Indian Bank, Indian Overseas Bank, and UCO Bank; Canara’s rate applied to loans above INR 75 lakh, while others applied to smaller credit amounts.

FDs will Fetch Lesser Returns Now

Lenders are also anticipated to lower returns on fixed deposits (FDs) in order to maintain profitability in the face of rate cuts and increasing liquidity in the banking system. In the short term, this change might make fixed deposits less alluring to savers.

While trying to promote economic growth through lower borrowing costs, the RBI’s drop of the repo rate and the banks’ subsequent adjustments show continuous efforts to balance credit availability, profitability, and competitive pressures in the Indian banking sector.

With the CEO of HDFC Bank now also named as an accused for allegedly targeting and harassing founder trustee Kishor Mehta, the ongoing conflict between the current trustees and former trustees of the Lilavati Kirtilal Mehta Medical Trust (LKMMT), which operates the renowned Lilavati Hospital in Bandra West, Mumbai, has intensified.

In connection with the INR 1,250 crore embezzlement scandal, Prashant Mehta, the current permanent trustee, has filed a formal complaint against the CEO of HDFC Bank and seven other former trustees, including Chetan Mehta and other members of the LKMMT, for criminal breach of trust and deceit.

Prashant Mehta, a permanent trustee of the LKMMT, filed the FIR in response to an order from a Bandra magistrate court against Sashidharan Jagdishan, the CEO of HDFC Bank, and seven other people, including previous trustee Chetan Mehta. Chetan Mehta and several previous trustees were charged by Prashant Mehta in March with embezzlement of trust funds, money laundering, and other financial violations.

After then, FIRs were filed, and an inquiry was requested from the Enforcement Directorate. Speaking at a press conference on June 7, Prashant Mehta charged that Sasidharan and prior trustees, notably Chetan Mehta, had harassed Kishor Mehta. The Bandra police filed a formal complaint against Sasidharan and the other suspects in accordance with the magistrate’s court order.

HDFC Calling it a Strategy to Thwart Recovery

HDFC Bank, a prominent private sector lender, has refuted allegations against its CEO, Sashidharan, asserting that the allegations were intended to impede the recovery process of loans borrowed from the bank by the trustees.

However, Prashant Mehta asserted that Kishor Mehta, who is 84 years old, was continuously harassed by more than 100 court summonses for reporting the operations of the trust. Kishor Mehta passed away in the midst of ongoing legal and medical issues, Prashant Mehta added.

INR 1.5 Crore Bribe-Falsely Presented as CSR Donation: Mehta

The permanent trustee also claimed that senior hospital doctors were bribed with INR 1.5 crore under false pretences of a CSR donation in order to try to hide or destroy important documents. This is neither a personal quarrel nor a business miscommunication, according to Prashant Mehta.

This is a pervasive criminal breach of the rule of law, charity law, fiduciary duties, and public funds. In addition to suppressing the truth, Mr. Sashidhar Jagdishan has obstructed justice by abusing his institutional position. In order to rebuild trust in India’s banking and judicial systems, the trust requests that he be removed immediately.

There is substantial documentary evidence to support the complaint against Mr. Jagdishan: A recovered cash diary shows that prior trustees paid Mr. Jagdishan INR 2.05 crore in unauthorised cash transfers.

INR 25 crore in trust funds were illegally deposited into HDFC Bank without any kind of resolution, authorisation, or supervision. Mehta claimed that Mr. Jagdishan and his family received preferential medical care and waivers at Lilavati Hospital in return for their quiet and complicity.

The Reserve Bank of India (RBI) fined HDFC Bank INR 75 lakh after discovering that the bank had not followed certain of the guidelines outlined in the RBI’s Know Your Customer (KYC) master guidance. Notably, the RBI is referring to a KYC master circular that was last modified on November 6, 2024, having been issued on February 25, 2016. In a March 26, 2025, press release, the RBI said that HDFC Bank Limited (the bank) had been fined INR 75.00 lakh (Rupees Seventy-Five Lakh only) by an order dated March 24, 2025, for failing to comply with specific guidelines the RBI had given regarding “Know Your Customer (KYC).” In accordance with Section 47A(1)(c) read with Section 46(4)(i) of the Banking Regulation Act, 1949, the RBI was granted the authority to impose this penalty.

How it all Begin?

The RBI went on to clarify in its statement that the bank’s financial status as of March 31, 2023, was the subject of a Statutory Inspection for Supervisory Evaluation (ISE 2023) of the bank. A notice was sent to the bank asking it to provide justification for why it should not be penalised for its failure to follow the RBI’s instructions, based on supervisory findings of non-compliance and related correspondence. The RBI made it clear that this financial penalty is specifically tied to regulatory compliance shortcomings and has nothing to do with the legitimacy of any transactions or agreements the bank has made with its clients. Furthermore, the penalty has no bearing on any further actions the RBI may take against HDFC Bank.

HDFC Fails to Provide Satisfactory Response

In its official statement, the RBI stated that, among other things, it determined that the following charges against the bank were upheld, justifying the imposition of a monetary penalty, after taking into account the bank’s response to the notice and other submissions made by the bank. Based on its evaluation and perception of risk, the bank did not assign some of its customers to the low, medium, or high risk categories. Rather than assigning a Unique Customer Identification Code (UCIC) to every customer, the bank assigned numerous UCICs to certain consumers.

Why Banks Need to Follow RBI’s KYC Guidelines?

Reiterating the January 2004 instructions, the “Know Your Customer” guidelines were released in February 2005 in response to the Financial Action Task Force’s (FATF) recommendations on combating the financing of terrorism (CFT) and anti-money laundering (AML) standards. These guidelines are now the global norm by which regulatory bodies formulate anti-money laundering and anti-terrorism funding strategies. International financial ties now require that the nation’s banks, financial institutions, and NBFCs adhere to these requirements. The Reserve Bank’s Department of Banking Operations and Development has provided banks with comprehensive guidelines based on the Financial Action Task Force’s recommendations and the Basel Committee on Banking Supervision’s paper on Customer Due Diligence (CDD) for banks, with indicative suggestions where deemed necessary. NBFCs are equally subject to these rules.

Therefore, it is recommended that all NBFCs adopt it with appropriate modifications based on their activities and make sure that, within three months of the date of this circular, a proper policy framework on “Know Your Customer” and anti-money laundering measures is developed and implemented with the Board’s approval. Before December 31, 2005, NBFCs were urged to make sure they were completely in compliance with the guidelines.

To support manufacturing startups, the Department for Promotion of Industry and Internal Trade (DPIIT) has partnered with SaaS giant Tally Solutions and HDFC Bank by signing a memorandum of understanding (MoU). Tally will provide training, case studies, and expert-led sessions to assist the chosen new-age tech companies in streamlining operations, implementing scalable business practices, and addressing startup challenges in areas like financial management, compliance, marketing, and digitisation, according to a statement from DPIIT.

Along with networking possibilities with colleagues and mentors in the sector, the SaaS platform will also provide users with free one-year rental licenses of Tally Prime software. Speaking about the collaboration, DPIIT joint secretary Sanjiv Singh stated that it will provide entrepreneurs with in-depth knowledge and useful resources to help them deal with the intricacies of markets. Tally is committed to providing business owners with the information, resources, and technology they need to expand their enterprises. Tally Solutions’ managing director, Tejas Goenka, remarked, “Tally is proud to partner with DPIIT to support entrepreneurs in their journey. Their efforts to support this ecosystem have been incredible.”

Joining Hands With HDFC

Additionally, DPIIT signed a Memorandum of Understanding with HDFC Bank, which would provide “customised” banking and financial products for domestic startups as part of the new partnership. To further improve the start-up scene in India, HDFC is happy to partner with DPIIT. According to Sunali Rohra, head of startups and gig banking at HDFC Bank, DPIIT-supported start-ups will easily access the bank’s tailored range of products designed to help speed their growth. The flurry of collaborations comes only a day after Kotak Mahindra Bank joined forces with incubators IIMA Ventures, NSRCEL, and T-Hub to launch the Kotak BizLabs accelerator program to support early-stage entrepreneurs.

The chosen entrepreneurs from industries like agritech, climate tech, fintech, edtech, healthcare, and sustainability will get mentorship, thematic workshops, and “guaranteed” seed investment from Kotak BizLabs as part of this initiative.

DPIIT’s Slew of Partnerships to Further Support Startup Ecosystem

However, in an effort to support the domestic startup scene, DPIIT has recently signed a number of collaborations. The department partnered with e-commerce giant Flipkart earlier this month to support and guide emerging businesses. Before that, DPIIT had collaborated with Moglix, a B2B e-commerce platform, to provide manufacturing firms with assistance. The government also partnered with HCLSoftware in October to advance its manufacturing incubation program.

HDFC Bank, India’s largest private sector lender by market capitalization, has cemented its position as a leader in the banking industry with its focus on retail and digital banking.

Beyond banking, HDFC Bank’s revenue model strikes an effective balance between interest-based earnings and diversified income streams, bolstered by treasury operations and non-interest revenue sources. Its robust financial metrics, including a strong CASA ratio and healthy capital adequacy, highlight its readiness for long-term sustainable growth.

From HDFC ERGO’s insurance solutions to HDFC Credila’s pioneering role in education financing and HDFC Property Fund’s real estate focus to the philanthropic efforts of the HT Parekh Foundation, the bank seamlessly integrates business growth with social impact.

In this Startup Talky, we will explore HDFC Bank’s journey, its revenue model, growth strategies, and the innovative ecosystem that sets it apart as a market leader.

HDFC Bank Limited, based in Mumbai, stands as India’s leading private sector bank by assets and ranks among the top ten banks worldwide by market capitalization as of May 2024. This financial powerhouse has carved out a significant presence, not just domestically but also on the global stage.

The Reserve Bank of India (RBI) has designated HDFC Bank, alongside the State Bank of India and ICICI Bank, as “Domestic Systemically Important Banks” (D-SIBs), signaling their crucial role in India’s financial ecosystem. These banks, often labeled as “too big to fail,” are integral to maintaining economic stability.

In terms of market value, HDFC Bank boasted a capitalization of $145 billion as of April 2024, making it the third most valuable company listed on Indian stock exchanges. Following its merger with the Housing Development Finance Corporation (HDFC), the bank expanded its workforce to over 173,000 employees, placing it among India’s largest employers.

HDFC Bank – Industry

As of July 2024, India’s mutual fund industry managed an impressive Assets Under Management (AUM) worth INR 64.97 lakh crore (US$ 780.70 billion). From April 2023 to March 2024, systematic investment plans (SIPs) contributed a robust INR 2 lakh crore (US$ 24.04 billion).

Equity mutual funds also witnessed significant traction. By December 2021, these funds saw a cumulative net inflow of INR 22.16 trillion (US$ 294.15 billion). In December 2022 alone, the net inflows hit INR 7,303.39 crore (US$ 888 million), recovering from a 21-month low of INR 2,258.35 crore (US$ 274.8 million) in November of that year.

Another pivotal sector is India’s rapidly growing insurance industry. In FY23, life insurance companies recorded first-year premiums totaling US$ 32.04 billion. Meanwhile, the non-life insurance sector garnered premiums of INR 1.87 lakh crore (US$ 22.5 billion) by December 2022.

Adding to India’s financial ecosystem, the Bombay Stock Exchange (BSE) announced a partnership with Ebix Inc to launch a dedicated insurance distribution platform. The market also saw vibrant activity in the IPO space, with US$ 7.17 billion raised across 40 IPOs in FY23. The number of companies listed on the BSE has grown exponentially, rising from 135 in 1995 to 5,415 by June 2024.

HDFC Bank – Founders and Team

Hasmukhbhai Thakordas Parekh

Hasmukhbhai Thakordas Parekh Founder of HDFC Bank

H. T. Parekh, the visionary founder of HDFC, transformed the dream of homeownership for India’s middle class into a reality. Born in Surat and raised in a humble Mumbai chawl, Parekh’s journey from modest beginnings to leading one of India’s most valuable financial institutions is truly inspirational. A graduate in economics from Mumbai and a BSc in Banking and Finance from the prestigious London School of Economics, Parekh’s career spanned roles as a lecturer, stockbroker, and later a key leader at ICICI, where he retired as Chairman and Managing Director. Not content with resting on his laurels, Parekh founded HDFC at the age of 66 in 1977, laying the groundwork for a financial powerhouse valued today at INR 4.14 lakh crore—outshining even icons like Dhirubhai Ambani. A recipient of the Padma Bhushan, Parekh’s life epitomizes resilience, vision and a lasting impact on India’s banking and housing sectors.

Sashidhar Jagdishan

Sashidhar JagdishanMD and CEO of HDFC Bank

Sashidhar Jagdishan, the MD and CEO of HDFC Bank, is a homegrown leader who has spent 24 years shaping the bank’s extraordinary journey. A proud “Mumbai boy,” Jagdishan grew up in the serene suburb of Matunga, attending Don Bosco High School before pursuing a bachelor’s degree in Physics from Mumbai University. With a Chartered Accountant qualification and a Master’s in the Economics of Money, Banking & Finance from the University of Sheffield, UK, his academic pedigree laid a solid foundation for his career. Starting at Deutsche Bank in financial control, Jagdishan joined HDFC Bank in 1996 as a manager and climbed the ranks to lead the institution after the legendary Aditya Puri. Today, as the torchbearer of India’s largest private sector bank, Jagdishan exemplifies dedication, expertise, and the ability to drive growth in a rapidly evolving financial landscape.

HDFC’s transformative journey began in 1978 when it issued its first loan, setting the stage for a groundbreaking venture in India’s housing finance sector. By 1984, under the visionary leadership of H. T. Parekh, the company was approving loans exceeding INR 100 crore annually. Parekh’s relentless dedication earned him the Padma Bhushan in 1992, solidifying his legacy as a pioneer in financial innovation.

The story took a monumental leap in 1994 when HDFC Ltd secured approval from the Reserve Bank of India (RBI) to establish a private sector bank. Incorporated in August 1994, HDFC Bank began operations as a Scheduled Commercial Bank in January 1995, with its first office at Ramon House, Churchgate, Mumbai. This move aligned with the RBI’s efforts to liberalize India’s banking sector, marking the birth of a financial institution destined for greatness.

HDFC Bank’s early years were defined by its unwavering commitment to trust, customer-centricity and operational excellence. Guided by these core values, the bank quickly built a reputation for reliability and innovation, capturing the trust of customers across the nation.

HDFC Bank’s journey to becoming a financial titan included key mergers and acquisitions. In 2000, it merged with Times Bank, marking India’s first voluntary bank merger. This was followed by the 2008 acquisition of Centurion Bank of Punjab (CBoP) in a share-swap deal, further solidifying its footprint in the Indian banking landscape.

Decades later, the historic merger of HDFC and HDFC Bank created a financial behemoth valued at INR 4.14 lakh crore. From a single loan to a banking empire, the HDFC journey stands as a shining example of resilience, vision, and determination—transforming lives and reshaping India’s financial ecosystem.

HDFC Bank envisions being recognized as a world-class Indian bank that embodies trust, transparency, and service excellence. It strives to lead the banking industry by setting benchmarks in innovation, customer satisfaction, and financial stability, creating value for all stakeholders while contributing to the nation’s economic progress.

Mission

HDFC Bank’s mission is built on a twofold objective. The first is to be the preferred banking partner for both retail and wholesale customer segments by offering tailored and superior financial solutions. The second is to drive healthy profitability growth while maintaining a balanced approach to risk management. The bank is committed to delivering on these goals through a foundation of trust, transparency, and an unwavering dedication to service excellence.

HDFC Bank – Name, Tagline and Logo

HDFC Logo

Tagline: “We understand your world”

HDFC Bank’s tagline reflects its deep commitment to understanding and addressing the unique needs of its customers, ensuring a personalized and seamless banking experience.

Logo: The bank’s innovative musical logo, MOGO, serves as a vibrant representation of its values, harmonizing tradition with modernity while creating a distinct identity that connects with customers on a sensory level.

Core Values: HDFC Bank’s identity is rooted in its steadfast core values:

Customer Focus: Placing customer satisfaction at the forefront of its operations, the bank offers tailored solutions to meet diverse financial needs.

Product Leadership: Continuously innovating and introducing market-leading financial products that redefine convenience and accessibility.

Sustainability: Upholding environmental and social responsibility by integrating sustainable practices into its operations.

People-Oriented Services: Fostering a culture of inclusivity, empathy and service excellence, ensuring meaningful engagement with customers and employees alike.

HDFC Group has built a dynamic and diversified business structure that caters to a wide spectrum of financial needs. Its various subsidiaries and initiatives contribute to its standing as a leader in the financial services sector.

Comprehensive Protection with HDFC ERGO

HDFC ERGO, the general insurance arm of the group, offers a diverse portfolio of insurance products, including health, motor, and other general insurance solutions. Known for its straightforward and efficient claims process, it ensures customer confidence with its commitment to reliability and transparency.

Empowering Customers Through HDFC Sales

Initially established to promoteHDFC’s home loans, HDFC Sales has expanded to become the one-stop distribution network for the entire group’s offerings. From mutual funds to insurance and wealth management products, it provides seamless access to financial solutions under one umbrella.

Shaping Futures with HDFC Credila

Launched in 2006, HDFC Credila stands as India’s first company exclusively dedicated to education loans. Partnering with colleges across the country, it specializes in tailored loan solutions, empowering students to pursue their academic goals with ease.

Driving Real Estate Investments via HDFC Property Fund

As one of the largest private equity entities focusing on Indian real estate, HDFC Property Fund manages assets worth ₹72 billion. It plays a pivotal role in shaping the real estate landscape through strategic investments and fostering growth in the sector.

Transforming Lives with HT Parekh Foundation

The HT Parekh Foundation, the group’s philanthropic initiative, works tirelessly to uplift underprivileged communities. By addressing critical challenges in areas like education, healthcare, and livelihood, the foundation embodies HDFC’s commitment to societal betterment.

HDFC Bank’s revenue model reflects a balance between core lending operations and diversified income streams. By blending interest-based earnings with dynamic treasury operations and non-interest income, the bank ensures long-term profitability while delivering value to its customers and stakeholders.

1. Interest Income: Core of Banking Operations

The primary source of revenue for HDFC Bank comes from the interest earned on loans, advances, and investments in government securities and other financial instruments. These loans cater to a wide range of segments, including retail, corporate, and priority sectors, forming the backbone of the bank’s financial operations.

2. Non-Interest Income: Diversified Earnings

HDFC Bank generates substantial revenue from non-interest sources, emphasizing service-based offerings:

Fees and Commissions: Derived from services like credit card transactions, remittances, and trade finance.

Cash Management Services: Efficient solutions for businesses, contributing to steady income streams.

Other Financial Services: Advisory and wealth management services also add to this segment.

The bank’s treasury department plays a crucial role in generating income through:

Trading Activities: Profits from trading in foreign exchange, government securities, and other market instruments.

Asset Management: Effective handling of cash and liquid assets to maintain optimal liquidity.

Risk Management: Mitigation of interest rate and liquidity risks to safeguard financial stability.

HDFC Bank – Challenges Faced

HDFC Bank is leveraging its operational strength and market leadership to address these challenges. By recalibrating its strategies and focusing on sustainable growth, the bank aims to enhance long-term value for its customers and shareholders.

1. Deposit Growth vs. Credit Growth

The pace of deposit growth has raised concerns as it has not kept up with the bank’s credit expansion, creating a credit-deposit gap. To address this, the bank plans to prioritize deposit growth over advances, aiming to bring down its credit-deposit (CD) ratio to more sustainable levels.

2. Rising Cost of Deposits

The cost of deposits has surged due to recent interest rate hikes and the Reserve Bank of India (RBI) draining surplus liquidity from the market. This has increased funding expenses, prompting the bank to adopt a cautious approach toward loan pricing and deposit mobilization.

3. Changing Consumer Preferences

A noticeable shift in consumer preferences toward mutual funds, equities and real estate has impacted deposit growth. The bank is working on tailored products and innovative strategies to attract deposits and retain customer loyalty.

4. Increased High-Cost Borrowing

Post-merger, the share of high-cost borrowing in the bank’s total liabilities has risen significantly, from 8% to 21%. This change has led to increased interest expenses, posing a challenge to profitability. The bank is focusing on optimizing its borrowing mix to mitigate this impact.

5. Balance Sheet Realignment

HDFC Bank is undergoing a strategic realignment to integrate operations post-merger and ensure regulatory compliance. While this may result in slower growth in the short term, the bank is focused on stabilizing key metrics like net interest margin (NIM), credit-deposit ratio, and liquidity coverage ratio (LCR).

6. Concerns Over Elevated Valuations

HDFC Bank’s elevated valuations, especially as one of the most heavily-owned stocks in the market, have drawn scrutiny. Investors and analysts are closely monitoring the bank’s ability to deliver consistent growth amid heightened expectations.

HDFC Bank – Funding and Investors

HDFC Bank has been strategically investing in branch expansion, technology upgrades, and customer-centric solutions, driving growth and strengthening its market leadership. Their total funding amount is currently at $2 Billion after 5 rounds of funding. They are as follows:

Date of funding

Funding Amount

Round Name

Investors

May 17, 2024

Post-IPO Debt

$500M

International Financial Corp.

Feb 7, 2024

Post-IPO Debt

$750M

–

April 12, 2023

Post-IPO Debt

$300M

The export-import Bank of Korea

Dec 23,2023

Post-IPO Debt

$400M

International Financial Corp.

Dec 5, 2022

Post-IPO Equity

$6.8M

Life Insurance Corp.

HDFC Bank – Mergers and Acquisitions

HDFC Bank has expanded through mergers like Times Bank and Centurion Bank of Punjab, creating a robust and diversified banking entity. And many more like:

Date

Organization Name

Funding Round

Money Raised

April 16, 2024

GPS Renewables

Debt Financing

INR 4.1Cr

March 20, 2024

Fam Infinity

Grant

INR 425 K

Feb 17, 2024

Fruitoholic

Debt Financing

–

Feb 7,2024

Cashinvoice

Series A

INR 282 Cr

Jan 30, 2024

Blackopal Group

Debt Financing

INR 250 Cr

Dec 11, 2023

Thirumals Paper Arizona Pvt Ltd.

Debt Financing

INR 50 Cr

Jun 28, 2023

Bonito

Debt Financing

INR 400 Cr

Jun 15, 2023

IdeaForge

Venture Round

INR 600 Cr

April 24, 2023

Goa Digit-Life Insurance

Debt Financing

INR 218.6 Cr

Feb 21, 2023

MintOak Innovations

Series A

INR 1.7 Cr

HDFC Bank – Growth

1. Advances Growth: HDFC Bank has demonstrated robust growth in its advances, with a significant year-on-year increase of 54.39%. This growth outpaces the bank’s 5-year compound annual growth rate (CAGR) of 19.71%, reflecting strong demand for credit and the bank’s ability to meet the evolving needs of its customers.

2. Revenue Growth: The bank’s revenue has surged by 99.35% year-on-year, significantly outperforming its 3-year CAGR of 37.37%.

3. Profit Growth: HDFC Bank has consistently delivered strong profitability, posting a 25.03% profit growth over the past 3 years.

4. Income Growth: The bank’s income has grown by 28.82% over the past 3 years

5. CASA Ratio: The bank’s Current Account and Savings Account (CASA) ratio stands at a healthy 38.19% of total deposits.

6. Capital Adequacy Ratio (CAR): HDFC Bank maintains a strong Capital Adequacy Ratio (CAR) of 18.80%, which is well above the regulatory requirement.

HDFC Bank – Advertisements and Social Media Campaigns

HDFC Parivartan National Ad Campaign

HDFC Bank’s Parivartan Launched a National Ad Campaign on ESG (June 6, 2022)

In celebration of World Environment Day, HDFC Bank launched a compelling national advertising campaign focused on Environmental, Social, and Governance (ESG) initiatives under its flagship program, Parivartan. The campaign was aimed at raising awareness about pressing environmental and social issues, urging the public to act today for a better tomorrow.

Powerful Message Through Film: The campaign consisted of four unique and thought-provoking films, conceptualized by Leo Burnett, which utilize dramatic visuals to underscore the urgency of the current environmental and social challenges. Each film highlights a different cause supported by HDFC Bank’s corporate social responsibility (CSR) efforts. The visuals depict a bleak future that will become inevitable unless action is taken now and demonstrate how restorative measures are already underway through HDFC Bank’s Parivartan initiatives.

Call to Action for Change: The films showcase real steps being taken by the bank to address critical social and environmental issues. Through these narratives, the bank invites viewers to join in making a positive change, reinforcing HDFC Bank’s role as a socially responsible corporate entity. The campaign aims to spark a movement toward collective action to build a sustainable future.

Nationwide Activation and Street Play: In addition to the film campaign, HDFC Bank has planned an impactful activation across more than 40 locations nationwide. The bank will host short street plays at over 125 busy traffic signals, encouraging commuters to turn off their engines while waiting at the signals. This initiative seeks to reduce air pollution and promote sustainable habits among the public.

Parivartan’s CSR Focus Areas: HDFC Bank is one of the largest corporate CSR spenders in India, with Parivartan focusing on key areas such as climate care, rural development, education, skill development, healthcare and hygiene, and financial literacy. Through its extensive CSR work, the bank continues to champion social and environmental causes, aiming to make a significant impact on society and the environment.

This campaign represents HDFC Bank’s ongoing commitment to integrating ESG principles into its core operations, encouraging others to join in the effort to create a better and more sustainable future for all.

HDFC Bank – Awards and Achievements

Conscious Corporate of the Year 2023 – Awarded by the Economic Times Awards.

India’s Best Bank – KPMG Study (2016)

Most Valued Brand in India – BrandZ Rankings

Best Managed Public Company – FinanceAsia (2015)

Best Bank in India at Euromoney Awards (2021)

HDFC Bank – Competitors

Despite fierce competition, HDFC Bank stands out as India’s largest bank by market capitalization and the fourth-largest in the world.

1. ICICI Bank

2. Kotak Mahindra Bank

3. Punjab National Bank (PNB)

4. Bank of Baroda (BoB)

HDFC Bank – Future Plans

1. Branch Expansion: HDFC Bank is set to significantly expand its physical footprint, with plans to open 1,000 branches in 2024. Over the next three to five years, the bank aims to reach a total branch count of 13,000–14,000, enhancing its network to attract granular deposits and strengthen its presence in underpenetrated markets.

2. Core Banking System Migration: On July 13, 2024, HDFC Bank will migrate its Core Banking System (CBS) to a modern platform, underscoring its commitment to enhancing operational efficiency, scalability, and customer experience.

3.Credit-Deposit Ratio Management: To maintain financial stability and optimize liquidity, the bank plans to grow advances at a slower pace than deposits. This strategy aims to lower the credit-deposit (CD) ratio to pre-merger levels, ensuring a balanced and sustainable growth trajectory.

4. Employee Retention Initiatives: HDFC Bank is addressing employee attrition and aims to bring it down to 15% through targeted retention programs, better work-life balance initiatives, and career growth opportunities.

5. Technology Infrastructure: The bank has made significant strides in technology modernization by upgrading its core banking system, launching new digital solutions, and relocating its primary data centers to advanced facilities in Mumbai and Bengaluru.

6. Focus on MSME Lending: With an aggressive branch expansion strategy and a strong focus on MSME lending, HDFC Bank aims to capture growth opportunities in this segment. Analysts from Motilal Oswal Securities project the merged entity to achieve a loan growth of 12% for FY24, with a recovery to a 17% CAGR in loan growth over FY24–26.

FAQ

How did HDFC Bank start?

HDFC Bank was founded in 1994, and promoted by the Housing Development Finance Corporation (HDFC), to provide banking and financial services after India’s banking sector liberalization.

Is HDFC the No. 1 bank in India?

Yes, HDFC Bank is India’s largest private bank by market capitalization and assets.

India’s economy and entrepreneurial spirit have flourished in recent years, leading to the emergence of the top 10 companies by market valuation as the leaders of the country’s dynamic corporate landscape in 2024.

These companies span various sectors and industries, showcasing their success and innovation and contributing to the country’s growth trajectory while influencing global markets.

In this article, we will take a closer look at the top 10 companies in India by market valuation, exploring their diverse sectors, innovative strategies, and the factors that have contributed to their success.

Reliance Industries – Top Indian Companies by Market Valuation

Reliance Industries Limited is recognized as India’s largest private-sector corporation that focuses on stakeholder-centric innovation and sustainable growth. Its motto is “Growth is Life.”

Over the years, Reliance has transformed from a textile and polyester company to an integrated player across various energy, materials, retail, entertainment, and digital services, contributing significantly to India’s economic landscape.

The company strongly believes in “What is Good for India is Good for Reliance”. It has positioned itself as a driving force behind India’s progress, especially in its commitment to self-reliance, sustainable growth, and embracing the new energy and digital-first future.

Reliance’s approach to value creation is characterized by its commitment to move “Forward with India” and “Forward with Everyone,” ensuring that the benefits extend beyond shareholders.

The company focuses on superior returns for investors, adherence to regulatory compliance, substantial contributions to the national exchequer, and extensive philanthropic initiatives through Reliance Foundation, thereby establishing itself as a responsible corporate citizen.

Reliance aims to provide superior experiences for its vast customer base across various business verticals, supported by solid partnerships with suppliers and vendors, including MSMEs and domestic manufacturers.

The company conducts its businesses ethically and respectfully, striving to uphold integrity and accountability in all endeavours. Reliance Industries Limited continues to shape India’s economic landscape while fostering a better future for all stakeholders through its relentless pursuit of excellence and commitment to societal well-being.

TATA Consultancy Services (TCS)

Founder

J.R.D. Tata

Founded

1968

Sector

Information Technology

Tata Consultancy Services (TCS) – Top Indian Companies by Market Valuation

Tata Consultancy Services (TCS) is a well-known provider of IT services, consulting, and business solutions with a history of over five decades. TCS firmly believes that innovation and collective knowledge can bring a brighter future.

It has been at the forefront of partnering with some of the world’s largest businesses and using technology to drive transformative change.

At its core, TCS is committed to fostering enduring relationships and delivering sustainable outcomes that reflect a long-term view prioritising mutual growth. This commitment also extends to its corporate social responsibility initiatives.

TCS endeavors to create more remarkable futures by connecting individuals to opportunities within the digital economy. TCS aims to contribute to a fairer and more equitable world for all, aligned with the values of its parent company, the Tata Group.

TCS empowers organisations to thrive in the digital age with its diverse services. It offers comprehensive solutions tailored to meet the evolving needs of its clients, from harnessing the power of artificial intelligence and cloud technologies to enhancing cybersecurity measures and leveraging data analytics for informed decision-making.

TCS’s expertise in consulting, cognitive business operations, IoT digital engineering, network solutions, sustainability services, and interactive experiences underscores its commitment to driving innovation and sustainability across various domains.

HDFC Bank – Top Indian Companies by Market Valuation

HDFC Bank Limited, known as HDFC, is one of the leading banks in India’s financial services sector, based in Mumbai. It was established in August 1994 and became the country’s largest private sector bank by assets, following the ‘in principle’ approval granted by the Reserve Bank of India (RBI) to its parent company, HDFC, as part of the liberalisation of the Indian banking industry.

HDFC has a strong legacy in the private banking sector and boasts an impressive distribution network with 8,192 branches and 20,760 ATMs/Cash Recycler Machines spread across 3,836 cities and towns as of February 2024.

The bank significantly emphasizes good corporate governance and has instituted a robust Corporate Governance Policy that serves as a guiding framework for managing and monitoring the bank in line with the principles of good corporate governance. HDFC Bank is committed to societal progress and champions empowerment through its social initiatives under the banner of ‘Parivartan.’

Through Parivartan, the Bank endeavours to catalyze positive transformation in the lives of millions of Indians, focusing on contributing to the economic and social development of the nation by empowering its communities sustainably.

These initiatives span a diverse spectrum, including rural development, education, skill development, livelihood enhancement, healthcare and hygiene, and financial literacy.

ICICI Bank

Founder

World Bank, the Indian government, and the Indian business executives

Founded

1994

Sector

Banking and Financial Services

ICICI Bank – Top Indian Companies by Market Valuation

ICICI Bank Limited is a renowned Indian multinational bank and financial services provider. It is headquartered in Mumbai and has a registered office in Vadodara. It offers extensive services to corporate and retail clients through various delivery channels and specialized subsidiaries.

These services include investment banking, life and non-life insurance, venture capital, and asset management. Over six decades, ICICI Group has played a vital role in fostering India’s economic growth and development, with a steadfast commitment to promoting inclusive growth.

For its exemplary commitment to corporate governance, ICICI Bank was awarded the ‘Best Governed Company Award’ by the Asian Centre for Corporate Governance & Sustainability in 2023. It also won the title of ‘Best Bank’ in the ‘Large Banks’ category at the esteemed 16th edition of the Mint BFSI Summit and Awards.

With these accolades and its continued commitment to excellence and societal impact, ICICI Bank reaffirms its position as a trailblazer in the banking and financial services industry. It is driving progress and prosperity for its stakeholders and the nation.

Bharti Airtel

Founder

Sunil Bharti Mittal

Founded

1995

Sector

Telecommunication

Bharti Airtel – Top Indian Companies by Market Valuation

Bharti Airtel is a renowned telecommunications company that provides trusted ICT services globally. Headquartered in New Delhi, India, Airtel has a vast global network spanning the USA, Europe, Africa, the Middle East, Asia-Pacific, India, and SAARC regions.

It is one of the top 3 mobile service providers globally in terms of subscribers. It operates in 18 countries across South Asia, Africa, and the Channel Islands. Airtel is known for delivering cutting-edge technology and offers 5G, 4G, and LTE Advanced services in India that cater to the evolving needs of consumers and businesses.

The company’s pioneering approach to strategic management, particularly its outsourcing model that encompasses all business operations except marketing, sales, and finance, has enabled Airtel to establish the ‘minutes factory’ model. This model is characterised by low costs and high volumes, enhancing operational efficiency and driving growth.

With its commitment to excellence and innovation, Bharti Airtel Limited continues to redefine the telecommunications landscape, providing seamless connectivity and advanced services to customers across the globe.

State Bank of India (SBI)

Founder

Government of India and Reserve Bank of India

Founded

1806

Sector

Banking and Financial Services

State Bank of India (SBI) – Top Indian Companies by Market Valuation

State Bank of India (SBI) is a Fortune 500 company headquartered in Mumbai that specializes in public-sector banking and financial services. With a legacy spanning over 200 years, SBI has gained the trust of generations of Indians.

The bank has diversified its businesses through subsidiaries such as SBI General Insurance, SBI Life Insurance, SBI Mutual Fund, and SBI Card, among others. State Bank of India (SBI) operates globally through 235 offices in 29 foreign countries, ensuring a global presence across different time zones.

SBI remains committed to evolving and continually redefining banking in India by providing responsible and sustainable solutions to its customers. The bank’s roots trace back to the early nineteenth century with the establishment of the Bank of Calcutta in 1806, later rebranded as the Bank of Bengal in 1809.

This marked the beginning of the first joint-stock bank of British India, sponsored by the Government of Bengal. Subsequently, the Bank of Bombay and the Bank of Madras were established, forming the State Bank of India.

In addition to its banking services, it operates the SBI Foundation, a philanthropic arm dedicated to supporting development initiatives in India. The foundation aligns with corporate social responsibility mandates the Ministry of Corporate Affairs set. It is pivotal in driving positive change and fostering sustainable development nationwide.

Life Insurance Corporation of India (LIC) – Top Indian Companies by Market Valuation

Life Insurance Corporation of India (LIC) is a trustworthy and reliable organization serving over 250 million lives as part of its extended family. LIC has been providing its services for over six decades and understands its profound responsibility.

It recognizes the immense value of each life it touches. While insurance is its core business, LIC views its role as fostering trust and security in the lives of millions.

LIC is headquartered in Mumbai and is the largest insurance company in India and the largest institutional investor. It manages assets worth ₹49.24 trillion (US$620 billion) as of March 2023.

LIC is a public sector enterprise owned by the government of India. The Ministry of Finance administers it. It is committed to upholding the highest standards of service and integrity.

Apart from its core operations, Life Insurance Corporation (LIC) is committed to social responsibility. It demonstrates this through initiatives like the LIC Golden Jubilee Foundation. This charitable organisation was established in 2006 and is dedicated to promoting education, alleviating poverty, and improving living conditions for the underprivileged.

One of its notable programs is the Golden Jubilee Scholarship Award, which supports meritorious students from economically disadvantaged backgrounds in pursuing higher education.

Infosys – Top Indian Companies by Market Valuation

Infosys, a global leader in next-generation digital services and consulting, is driven by a profound purpose: to amplify human potential and create the next opportunity for people, businesses, and communities.

With a presence spanning more than 56 countries, Infosys empowers clients to navigate their digital transformation journey effectively. Drawing on over four decades of experience in managing the systems and operations of global enterprises, Infosys adeptly guides clients through their digital evolution, leveraging the power of cloud computing and artificial intelligence (AI).

By infusing an AI-first approach into the core of operations, facilitating agile digital solutions at scale, and fostering a culture of continuous learning, Infosys enables clients to achieve sustained growth and innovation.

The company is deeply committed to upholding good governance and environmental sustainability principles, fostering an inclusive workplace where diverse talent thrives.

As an Innovation and Knowledge Hub, Infosys spearheads initiatives like the Infosys Knowledge Institute, offering thought leadership to steer enterprises through their digital transformation journey.

Additionally, Infosys invests in entrepreneurial ventures globally through its Innovation Fund, established in 2015, and collaborates with startups worldwide through the Infosys Innovation Network, facilitating partnerships for client implementation.

Through these initiatives, Infosys remains at the forefront of driving digital innovation, knowledge dissemination, and sustainable growth, shaping a future where businesses and communities thrive in the digital age.

ITC

Founder

William M. Jacks

Founded

1910

Sector

Conglomerate

ITC – Top Indian Companies by Market Valuation

ITC, a leading Indian conglomerate, operates across diverse sectors, including fast-moving consumer goods, hotels, paperboards and packaging, agribusiness, and information technology. Recognised as India’s most admired company in a survey conducted by Fortune India in collaboration with Hay Group, ITC’s success is driven by its multifaceted approach to business.

As a leader in FMCG marketing and the Indian Paperboard and Packaging industry, ITC has established itself as a pioneer in farmer empowerment and responsible luxury hospitality. The company’s subsidiary, ITC Infotech, offers specialized digital solutions globally.

Over the years, ITC has developed a robust portfolio of 25+ Indian brands, leveraging its institutional strengths in consumer insights, R&D, and brand-building.

Embracing the ethos of ‘Nation First: Sab Saath Badhein’, ITC prioritizes societal value alongside profitability, leading in sustainability efforts and solid waste management through initiatives like the Well-being Out of Waste program.

Collaborating with farmers and local communities, ITC implements climate-smart and sustainable agriculture initiatives, aligning with the vision of doubling farmer incomes. In line with the “Make in India” initiative, ITC also invests in world-class manufacturing facilities and hospitality assets, reaffirming its commitment to India’s future development and competitive capacity.

Hindustan Unilever (HUL)

Founder

Hindustan Vanaspati Manufacturing Co., Lever Brothers India Limited and United Traders Limited

Founded

1933

Sector

Consumer Goods

Hindustan Unilever Limited (HUL) – Top Indian Companies by Market Valuation

Hindustan Unilever Limited (HUL), a British-owned Indian final goods company headquartered in Mumbai, is a subsidiary of Unilever. Established in 1931 as Hindustan Vanaspati Manufacturing Co., it was renamed Hindustan Lever Limited in 1956 and later became Hindustan Unilever Limited in 2007.

With a 90-year heritage in India, HUL is the country’s largest Fast Moving Consumer Goods (FMCG) company, offering over 50 brands across 16 categories.

As part of Unilever, a global leader in FMCG products, HUL benefits from extensive resources and expertise. It operates in over 190 countries and is known for its commitment to environmental, social, and governance principles.

HUL’s reputation extends beyond its products; it is India’s top ESG-rated FMCG company and the preferred employer across sectors. In a rapidly evolving world emphasizing digitization and sustainability, HUL remains dedicated to its purpose-led journey, ensuring it continues to meet the needs of consumers while fostering a sustainable future.

India’s vibrant corporate landscape in 2024 reflects a remarkable fusion of innovation, sustainability, and societal impact across diverse sectors. The top 10 companies by market valuation include names like ITC, Reliance Industries, HUL, Infosys, TCS, HDFC Bank, ICICI Bank, Bharti Airtel, SBI, LIC India.

Collectively, these companies not only drive India’s economic growth but also shape its social fabric through impactful initiatives that empower communities and foster sustainable development.

As India continues on its trajectory of progress, these companies serve as beacons of excellence, driving innovation, and contributing to a brighter future for all stakeholders.

FAQs

Which is the largest private company in India?

Reliance Industries is considered the largest private company in India.

Is Tata bigger than Reliance?

If we talk in terms of market valuation and revenue, Reliance is considered to be bigger than Tata. However, both have a wide range of businesses and are in a headstrong competition.

What is the richest company in the world in 2024?

Microsoft is considered as the richest company in the world for the year 2024 based on its market cap of $2992 billion. It is closely followed by Apple and Nvidia corporation.

The startup culture has taken over the world. More and more people are showing interest to start their businesses. The recent growth that the startup world has experienced is immense and it is not going to stop anytime soon. However, beginning a startup means needing one of the most significant things and that is investment or funds. Without finance, a business cannot happen.

People who launched their businesses search for finance as they need funds to grow their companies. Businesses make money by borrowing cash. So, there are banks that willingly provide loans to small businesses. In this article, we will talk about some of the banks from which you can take loans and their eligibility criteria, and the documents that are needed. So let’s get started.

Is It an Ideal Idea to Get the Loan Offered by Bank?

Acquiring Loans from Banks for a startup with a futuristic approach is always a good idea. Loans are regarded as a better source of capital for a gainful business than share capital as you get to have better leverage. You can enjoy a surplus of the rate of return over the interest you pay for the borrowings. To begin with a startup, you need to be very well aware of how to keep your interest rate as low as possible with maximum benefits.

Loans enhance the scope of your business by aiding you in expansion as well. On the other hand, it also acts as a catalyst to motivate you for better productivity. You can avail these advantages of acquiring startup loans-

You can get a boost to develop an even stronger business plan.

You can effectively manage the flow of money.

Higher rate of return on capital.

List of Best Banks for Small Business Startup Loans

Many banks offer loans to small businesses so that entrepreneurs can fulfill their dreams of running a business. However, the most popular banks that offer loans and are favored the most are listed below, they are:

HDFC Bank Business Loans

HDFC Bank Business Loan

Startups can expand their operations by obtaining additional financial assistance through HDFC bank. Every entrepreneur wants to have the least amount of documents, flexible tenures as well as low-interest rates, which you can get from HDFC. The bank offers loans to fulfill related funding. any kinds of business requirements

Loan Amount and Tenure

The Business loan amount is up to INR 40 Lakhs and even INR 50 Lakhs in selected places.

Loan Tenure is 12 months to 48 months.

Eligibility

Entrepreneurs, Proprietors, Private Ltd. Co., and Partnership Firms involved in the business of Manufacturing, Trading, or Services.

The business has a minimum turnover of Rs. 40 lakhs.

Individuals who have been working for at least 3 years with a minimum of 5 years of working experience in the field.

Business involved in profit-making for the past 2 years.

A business must have a Minimal Annual Income (ITR) of at least Rs.1.5 lakhs per year.

The applicant must be at least 21 years when they apply for the loan, and not older than 65 when the loan’s maturity.

Documentation

If you are interested in a business growth loan, then you can apply for it using the following paperwork.

Mandatory Documents [Sole Prop. Declaration or Certified Copy of Partnership Deed, Certified true copy of Memorandum & Articles of Association (certified by Director) & Board resolution (Original)]

A copy of any of the following documents as identity proof:

Aadhaar Card

Passport

Voter’s ID Card

PAN Card

Driving License

3. A copy of any of the following documents as address proof:

Aadhaar Card

Passport

Voter’s ID Card

Driving License

4. Latest ITR along with computation of income, Balance Sheet, and Profit & Loss account for the previous 2 years, after being CA Certified/Audited.

5. Proof of continuation (ITR/Trade license/Establishment/Sales Tax Certificate).

6. Bank statement of the previous 6 months.

Interest Rate & Charges

The interest range for Rack is between 10% to 22.5%.

Loan Processing Charges – Up to 2% of the loan amount. NIL Processing Fees for loan facility up to ₹5 Lakhs availed by micro and small Enterprises subject to URC submission before disbursal

Benefits

You don’t have to submit any collateral or security for taking a loan from HDFC.

The process of applications is very simple.

Least amount of documentation.

Doorstep service is available in this bank.

An additional feature is access to the overdraft facility. You pay interest only on the utilized loan amount together with a credit protection plan.

You can have the credit protection plan at a nominal price.

Citi Bank Business Loans

Citi Bank Business Loan

Citi Bank offers loans referred to as CitiBusiness that offer business loans through which startups can manage working capital efficiently. A startup can also opt for diversified MSME loan products which include working capital loans, short-term loans, long-term loans, overdrafts as well as export-import finance options too.

Citi India has transferred the ownership of its consumer business to Axis Bank starting from March 1st, 2023.

ICICI Bank Business Loans

ICICI Bank Business Loan