When it comes to managing expenses and bills, especially when one has low funds. This becomes really pressurizing and people start looking for sources to lend money from. In such situations, borrowing from friends and family could be embarrassing and hectic. And depending upon banks could cost major interests. So where should we look?

Well by acknowledging these situations and deals, online money lending apps are developed. These provide the facility to lend money through digital platforms without any further issues.

Multiple companies are providing the facility of offering loads immediately with minimal competitive interest rates and required tenure durations. These companies facilitate the loan very easily and quickly as compared to usual bank loans.

With keeping such progress in mind, India has developed numerous digital lending companies whose finances can manage smoothly. India is evolving to a great extent in the digital sector and financial inclusion. The country has cash for transactions. But with the evolving method of development and modernization, India is shifting toward a cashless economy. To understand its development more prominently, let’s look at the top 10 digital lending platforms in India.

Best Digital Lending Platforms in India – Lendingkart Website

The prominent digital lending platform, Lendingkart was founded in 2014. It works by offering different capital loans and company loans vary from small to medium-sized businesses across India. They are widely famous for providing capital completely through an online platform and require minimum documentation for the procedure to begin.

For young entrepreneurs, managing their finances becomes quite hectic and it deviates them from focusing on their business growth. That’s why Lendingkart has taken the initiative to make capital funding easily available for entrepreneurs so they don’t have to worry about the cash-flow gaps. Lendingkart is a company established in Ahmedabad, Mumbai and Bangalore. But, its services are accessible throughout the whole of India.

2. Pine Labs

Lending Platform

Pine Labs

Loan Amount

From ₹25,000 to ₹5 Lakhs

Loan Tenure

90 Days

Best Digital Lending Platforms in India – Pine Labs Website

Pine Labs is one of the leading fintech companies in India established in 1998 that provides digital lending services. The company is quite famous for its incredible facility of transforming the mobile NFC into a card machine and activating the service of accepting all types of payment digitally which also includes the ‘Tap n Pay’ card as well.

Pine Labs have brought tons of services for the retailers including multi-channel, different payment options, brand offerings, risk assessments, analytics, and many more.

It provides working capital loans for small to medium businesses. Their loan application process is quite simple and you can apply for a business loan through their website or their app myPlutus.

Pine Labs’ services and technologies are widely preferred and used by more than 100,00 merchants all across India and also, many Asian companies. According to the estimations, PineLabs’ cloud-based technology has the power of over 350,000 PoS terminals; that too in more than 3,700 cities.

3. MobiKwik

Lending Platform

Mobikwik

Loan Amount

Upto ₹5,00,000

Loan Tenure

6 to 36 Months

Top Loan Aggregators in India – MobiKwik Website

MobiKwik is a very prominent mobile payment company that works by connecting the consumers together with the merchants and many online sellers. The company is established in Gurgaon, Haryana, India.

Mobikwik is a private company that has more than 550 employees. Since the establishment of this company, the company has raised a total of 118 million USD from over 8 funding rounds.

Mobiwik provides instant personal loans. You can download its app and once the loan is approved it will be credited to your wallet.

₹1 Lakh to ₹15 Lakhs (unsecured) or up to ₹2.5 Crores (secured)

Loan Tenure

6 to 48 Months (unsecured), Up to 84 Months (secured)

One of the biggest lending companies, Shiksha Finance, is an education-based finance firm. Shiksha Finance provides the services of funding parents for school fees by reducing the school drop-out rates. It also offers capital to educational institutions for the development of buildings, properties and working capital.

Shiksha Finance has loans that range from INR 10,000 to INR 50,000 with a return duration of 6 to 10 months. The loans which Shiksha Finance provides can be utilized for educational based purposes such as school fees, tuition, luggage and stationary.

5. MoneyTap

Lending Platform

MoneyTap

Loan Amount

Upto ₹5,00,000

Loan Tenure

36 Months

Best Digital Lending Platforms in India – MoneyTap Website

The Bengaluru based lending company, MoneyTap is known for its huge service of offering credit lines for the consumers as their loans, with the partnership with RBL Bank. MoneyTap is now counted among the leading lending businesses. Recently, the company received the license of NBFC for co-lending space together with their lending partners.

MoneyTap has offered many great features among which, the minimal documentation procedure for a personal loan is the most special one. Moreover, its app version also provides the facilities for tracking down your borrowing records.

6. Paytm

Lending Platform

Paytm

Loan Amount

Upto ₹2,00,000

Loan Tenure

6 to 36 Months

Fintech Lending Companies in India – Paytm Website

The biggest digital lending wallet company Paytm is wildly famous in the minds of Indians. The company is established in Noida, Uttar Pradesh. Paytm has grown to a great extent and now, millions of downloads have been made.

The development the company has received is breathtaking. It employs more than 9000 people and has a revenue of a total of $118 million. Paytm is highly specialised in online shopping as well.

Best Digital Lending Platforms in India – PolicyBazaar

The company is counted among the top leading online insurance companies, PolicyBazaar was established in the year 2008 and headquartered in Gurgaon, Haryana, India.

It is online life insurance as well as a general insurance aggregator company. PolicyBazaar is very popular among Indians for its incredible services and holdings. It employs over 2500 people and has an annual revenue of $21 million (as estimated in 2017-18).

The current CEO of PolicyBazaar is Yashish Dahiya who is also one of the founders of this company. It has raised around US$ 346 million through 7 funding rounds.

8. Capital Float

Lending Platform

Capital Float

Loan Amount

₹50,00,000

Loan Tenure

Upto 36 Months

Best Digital Lending Platforms in India – Capital Float Website

Capital Float is one of the leading lending companies in India. It is acquired by CapFloat Financial Services. Capital Float is popular for its amazing service of specialised financial loans and business credits.

Capital Float has a partnership with some prominent companies such as Shopclues, Paytm and Uber. The company lends the potential borrower through its system of proprietary loans. Capital Float is now targeting established store owners and small merchants.

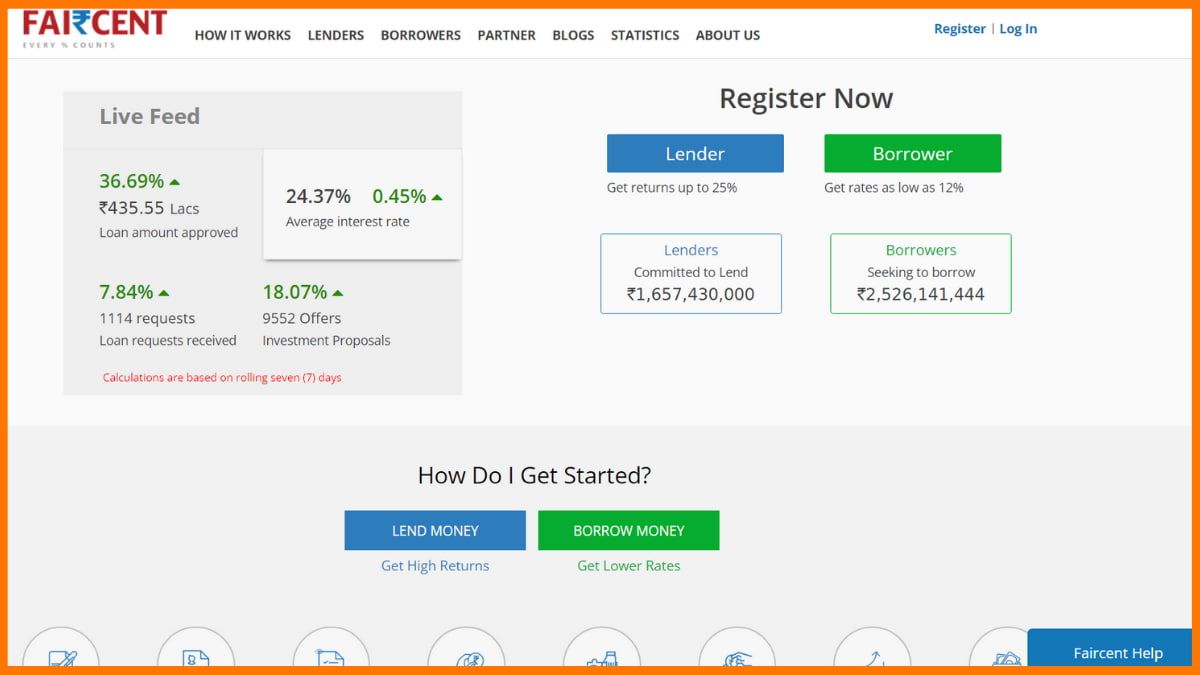

9. Faircent

Details

Information

Loan Amount

₹5,00,000

Loan Tenure

6 to 36 Months

Best Digital Lending Platforms in India – Faircent Website

The largest and first Indian peer-to-peer digital lending platform, Faircent is known to be absolutely amazing. It is officially registered by the RBI. It provides a safe marketplace for people to loan money to a borrower. Faircent facilitates the credit to organizations and individuals who are interested in lending money.

Faircent provides the absolutely convenient procedure of lending the required money to those who need it, at reasonable interest rates.

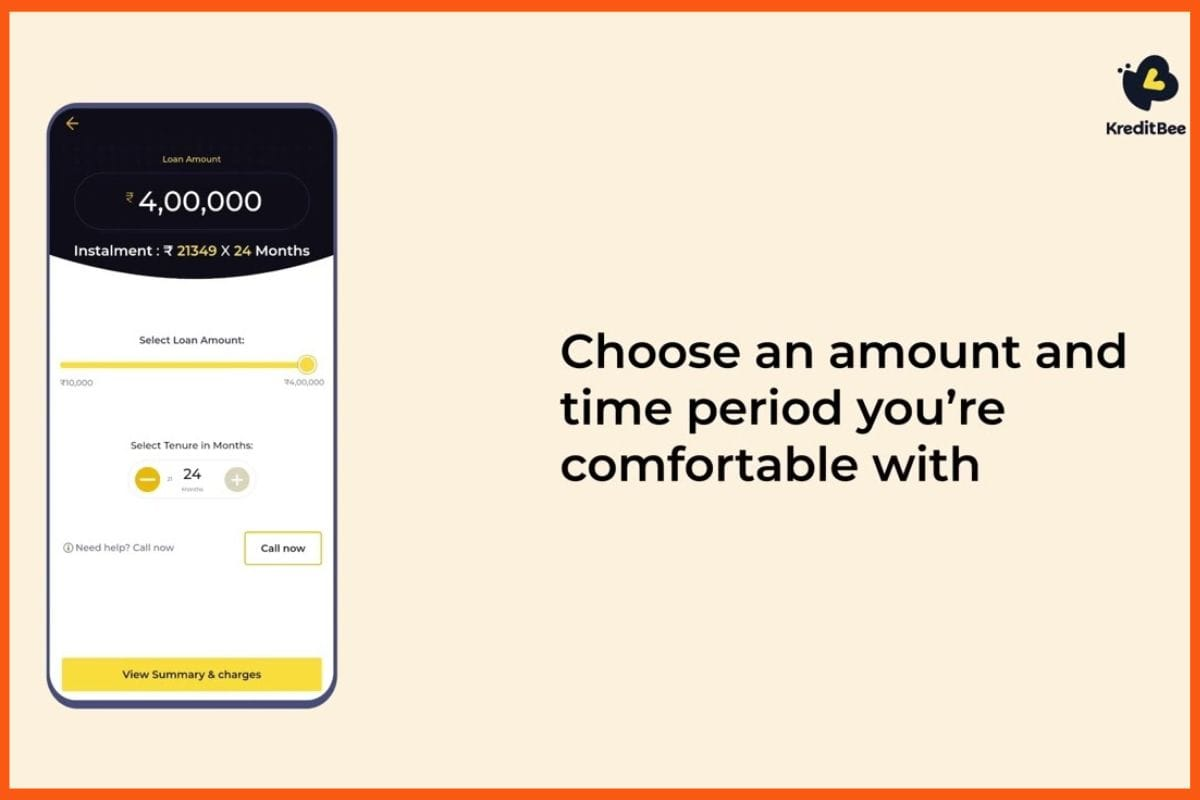

10. KreditBee

Lending Platform

KreditBee

Loan Amount

₹5,00,000

Loan Tenure

6 to 36 Months

Lending Service Providers in India – KreditBee

KreditBee is a Bangalore-based fintech that offers quick personal loans up to INR 2,00,000 for working professionals. Using easy online KYC, the loan process is fast and simple. KreditBee is one of the top lending companies in India.

Backed by trusted investors like ICICI Bank and supported by banks like AU Small Finance, KreditBee serves over 5 million customers.

The process is mostly paperless, sign up on the app, and within 15 minutes, approved loans are transferred instantly to your bank account.

In India, there are many fintech companies that are providing the service of digitally lending money very easily with the minimal documentation procedure. Today, many apps have been developed by these companies to make the transaction of money absolutely susceptible. And for those who require a personal loan or business loan, can easily get one. That’s why we listed these top digital lending companies in India.

FAQs

What are some of the top digital lending companies in India?

Lendingkart, Pinelabs, Mobiwik, Policybazaar, and Paytm are some of the top digital lending companies in India.

How does a lending company work?

Lending companies provide loans to an entity, which is then expected to repay its debt.

How many fintech companies are there in India?

There are around 2,000 fintech companies in India.

Company Profile is an initiative by StartupTalky to publish verified information on different startups and organizations.

The concept of credit is not new. People have been opting for credit since time immemorial. Credit is crucial when our capital cannot support certain investments, and credit cards have certainly made them easy to avail. However, paying the credit card bills is a priority and equally difficult to manage. This is why CRED decided to come forth with the unique idea of a platform that will help Indians pay their credit card bills on time and also offer them instant offers and rewards for the same.

CRED is a fintech company headquartered in Bengaluru, which allows its users to make credit card payments through its app and get exclusive offers and other benefits online. Furthermore, CRED has also introduced house rent payment options, Rent Pay; flexible credit lines, CRED Cash; and CRED Mint, with which the lenders can lend their idle money to borrowers who exhibit decent credit scores at interests of around 9% per annum.

Learn more about the CRED startup story, its founder, history, tagline, logo, business model, revenue model, funding, competitors, and more.

CRED allows credit card users to pay their credit card bills through its platform and extends rewards for each transaction. The fintech platform also lets users make their house rent payments and avail all the benefits of the short-term credit lines that the app now offers. The CRED headquarters is in Bangalore.

The company takes the utmost care in protecting the data and user information. Hence, the app is completely safe and secure. Kunal Shah is the founder of CRED. He founded the company in 2018 and often describes CRED as a TrustTech company, not a Fintech. This is because his initial motivation to start CRED came from solving trust issues in Indian society, which, according to him, is the key to economic prosperity. The CRED founder, Kunal Shah, is a well-known face in the startup ecosystem who has already funded numerous startups.

CRED – Startup Story

The Cred story was very simple. The goal was to create a platform where life could be made better and systematic. Kunal Shah wanted to offer more privileges and benefits to people with good credit scores. Therefore, creating a flywheel effect for more people was important to improve the scores.

Everybody, from the startups to the government, has focused on the masses. The founder of the company wanted to focus specifically on the people, the responsible citizens who pay taxes on time. He felt that nobody had solved their problems earlier.

‘If you look at history, nobody has been rewarded for paying back on time. We want to fix that.’

Therefore, CRED was founded primarily to solve the problems of the taxpayers and reward them with attractive rewards in return.

CRED – Founder and Team

Kunal Shah

Kunal Shah, Founder and CEO of CRED

Kunal Shah is the founder and CEO of CRED. He is an Indian entrepreneur who is credited for launching new ventures for a second time. Kunal was a Philosophy graduate from Wilson College and later went on to pursue an MBA from the Narsee Monjee Institute of Management Studies, but he dropped the course midway to chase his dreams as an entrepreneur.

Kunal started his entrepreneurial journey with PaisaBack, a website for cashback, coupons, and other offers for users, along with Sandeep Tandon. However, he eventually shut down its operations in order to found FreeCharge, which the duo founded in 2010.

FreeCharge was acquired by Snapdeal in April 2015, but the company still continued as an independent entity led by Shah. CRED was founded in 2018 and successfully turned unicorn on April 6, 2021. FreeCharge, on the other hand, was acquired by Axis Bank in July 2017. Here’s looking at the FreeCharge business model and how it makes money through it.

Kunal Shah was born in Mumbai in 1983. His hobbies include playing chess and poker. He loves munching on chips and guacamole. He loves the ideology of Socrates and the plays of G.B. Shaw.

CRED app – The CRED app is a neat-looking, beautifully designed app that users can visit if they want to go through the offers that are available after they pay their credit card bills. They can easily sign up on the app and view all the offers that they can avail of.

Businesses that provide offers on the app – The users of CRED can also find a wide range of offers from numerous businesses. For this, CRED brings businesses on board and collaborates with them. Along with benefitting CRED and its customers, who can avail of the exclusive offers provided by the businesses, it is also a win-win situation for the companies. This is because they also hugely benefit from the visibility they get.

Users who pay their credit card bills – CRED also serves as a smooth and rewarding platform for the users who use it to pay their credit card bills. In comparison to banking or other apps, end-users can choose CRED as an app to pay their credit card bills and get numerous offers and benefits. On the other hand, the users who like the app also share CRED with their family and friends.

CRED Mint – CRED disclosed its new feature, CRED Mint, on August 20, 2021, which is designed as a peer-to-peer lending platform that will help CRED users lend their idle money to creditworthy members. It is a rather transparent process that only allows the trustworthy CRED members boasting of a minimal credit score of 750 or higher to be the borrowers. Furthermore, the lenders can also withdraw their money whenever they want, with the interest that they have accumulated for the period.

There are 2 prominent ways via which CRED makes money,

Listing products and offers – CRED, as we know, lists an array of products and offers that benefit its users from a range of businesses. These businesses, in turn, pay CRED a fee for their visibility. Every time a user avails of the offers, CRED generates an income through it.

Using the financial data of the users, CRED accumulates the financial data from the users who use the platform for paying their bills and more. Along with providing CRED with the opportunity to introduce more offers to their users using these data, CRED also has other banks and financial institutions that pay them a fee for accessing these data. These companies, banks, and financial institutions would eventually approach the potential customers with their own set of products aligned to their tastes.

CRED has revealed that it does not charge any fees for the credit card payment options that it offers via its app. The company instead earns its revenues from the ancillary services it provides with the help of its technology and distribution platform.

CRED – Funding and Investors

Here’s a look at the CRED funding rounds:

Date

Transaction Name

Money Raised

Lead Investors

June 9, 2025

$72 million

Lathe Investment, RTP Global, Sofina Ventures, QED Innovation Labs

June 9, 2022

Series F

$80 million

GIC, Sofina, Alpha Wave and DF International

April 8, 2022

Venture Round

$200 million

GIC

October 19, 2021

Series E

$251 million

Tiger GLobal and Falcon Edge

April 6, 2021

Series D

$215 million

Coatue, Falcon Edge Capital and others

January 1, 2021

Post-IPO Secondary Round

–

–

November 30, 2020

Series C

$81 million

DST Global

July 26, 2019

Series B

$120 million

Gemini Investments, Ribbit Capital and Sequoia Capital India

April 16, 2019

Series A

$24 million

–

January 1, 2019

Seed Round

–

Rainmatter Technology

November 6, 2018

Seed Round

$30 million

Sequoia Capital India

CRED – Shareholding

CRED Shareholding Pattern as of March 2025

Here is CRED’s shareholding pattern as of March 2025, sourced from Tracxn:

CRED Shareholders

Percentage

Kunal Shah

10.8%

QED Innovation Labs

9.6%

Sequoia Capital

9.3%

Ribbit Capital

8.1%

Tiger Global Management

5.8%

Gemini Investment Management

4.8%

DST Global

4.5%

Alpha Wave Global

4.7%

Coatue

4.0%

Hillhouse Capital Group

2.0%

RTP Global

2.5%

General Catalyst

1.6%

Sofina

1.5%

Greenoaks

1.5%

GIC

0.9%

Prime Venture Partners

0.8%

Dragoneer Investment Group

0.8%

Insight Luxembourg

0.5%

Axiom Asia

0.2%

Marshall Wace

0.2%

Kalaari Capital

0.2%

Dream Duo

0.2%

Rise Global Capital

0.2%

Matrix Partners India

0.2%

SciFi

0.1%

Whiteboard Capital

< 0.1%

Rainmatter

< 0.1%

Greyhound Capital Management

< 0.1%

Bharat Innovation Fund

< 0.1%

Reddy Futures

< 0.1%

Venture Highway

< 0.1%

Future Shape

< 0.1%

Rajaram Family Trust

< 0.1%

Zarringhalam Ventures

< 0.1%

Mission Holdings

< 0.1%

Meridian Fund

< 0.1%

Cupola Venture Opportunites l

< 0.1%

Alteria Capital

< 0.1%

Valiant Capital Partners

–

ReDefine Capital Partners

–

Credence Partners

–

Ganesh Ventures

–

eWTP Capital

–

The Chatterjee Family Revocable Trust

–

AME Cloud Ventures

–

CRED

0.8%

Anxa Holding

0.6%

MVision

0.6%

GRACE software

0.3%

SFSPVI

0.2%

Stak3 International

0.2%

Spenny

< 0.1%

Strategic Asset Management

< 0.1%

Ra Hospitality

< 0.1%

Kuber Technologes

–

SF Roofdeck Capital

–

Angel

0.2%

Other People

1.3%

ESOP Pool

20.4%

Total

100.0%

CRED – Acquisitions

CRED has acquired five companies to date: Hipbar, Happay, smallcase, and Spenny. The recent acquisition is of Spenny on June 23, 2023.

Company Acquired

Date

Deal Value

Kuvera

February 6, 2024

–

Spenny

June 23, 2023

–

smallcase

August 2, 2022

$400 million

Happay

December 1, 2021

$180 million

HipBar

October 21, 2021

–

CRED – Growth and Revenue

CRED has shown steady growth throughout the years. Being a startup that was founded in 2018, it successfully joined the unicorn club on April 6, 2021, closing its Series D round where the company had mopped up $215 million. CRED controls “22% of all credit card payments in India every month,” said Kunal Shah in his statement released in April 2021. CRED’s valuation reached $6.5 billion in 2022 after a $200 million funding round.

Kunal Shah further took to his LinkedIn profile on July 10, 2021, and shared highlights of the milestones reached by CRED in June:

Kunal Shah shared financial progress of CRED on LinkedIn

CRED Financials

CRED saw its operating revenue grow by 71% to INR 2,397 crore in FY24, up from INR 1,400 crore the previous year.

Including other income, CRED’s total revenue increased by 66%, reaching INR 2,473 crore in FY24, compared to INR 1,484 crore in FY23.

However, despite the rise in revenue, the company’s net loss expanded by 22%, reaching INR 1,644 crore in FY24, up from INR 1,347 crore the previous year. CRED noted that its operating loss decreased by 41%, dropping to INR 609 crore from INR 1,024 crore in FY23. The company’s total operating expenditure, including one-time costs, amounted to INR 3,082 crore in FY24.

Whereas, CRED’s operating revenue has increased from INR 393.5 crore in FY22 to INR 1,400.6 crore in FY23. In terms of profit and loss, company losses increased from INR 1,279.5 crore in FY22 to INR 1,347 crore in FY23.

CRED Financials 2024

CRED Revenue Breakdown

Particulars

FY23

FY22

Revenue from Operations

INR 1,400.3 crore

INR 394.4 crore

Other Income

INR 84.4 crore

INR 28.2 crore

Total Revenue

INR 1,484.6 crore

INR 422.6 crore

Revenue more than tripled in FY23, led by a sharp increase in operational revenue from INR 394.4 crore to INR 1,400.3 crore.

CRED Profit/Loss

Losses remained high and consistent, increasing slightly from INR 1,279.6 crore in FY22 to INR 1,347.5 crore in FY23.

CRED Expenses Breakdown

The company’s total expenses rose from INR 1,702 crore in FY22 to INR 2,832 crore in FY23.

Particulars

FY23

FY22

Employee Benefit Expense

INR 788.9 crore

INR 307.6 crore

Finance Costs

INR 3.5 crore

INR 2.4 crore

Amortization & Depreciation

INR 59.4 crore

INR 14.3 crore

Other Expenses

INR 1,980.2 crore

INR 1,377.7 crore

Total Expenses

INR 2,832 crore

INR 1,702.1 crore

EBITDA

With a huge increase in EBITDA margin from -299.24% in FY22 to -86.42% in FY23, the company showed remarkable financial improvement. The ROCE increased from -42.66% in FY22 to -31.95% in FY23, demonstrating good improvement. These adjustments imply that the company’s financial performance is on the upswing.

EBITDA FY22-FY23

FY22

FY23

EBITDA Margin

-299.24%

-86.42%

Expense/₹ of Op Revenue

₹4.33

₹2.02

Roce

-42.66%

-31.95%

Quick Summary: Comparative Insights (FY23 vs FY22)

CRED introduced CRED Mint on August 20, 2021, which will serve as a peer-to-peer lending feature that can be used by the customers of CRED. CRED Mint was launched by CRED in collaboration with RBI-approved P2P Non-Banking Financial Company (NBFC), Liquiloans.

CRED Cash

CRED launched CRED Cash, a flexible credit line, in 2020. CRED Cash considers its members pre-approved for an active credit line of up to INR 5 lakhs without any documents, phone calls, forms, or physical visits.

Rent Pay

CRED launched Rent Pay in April 2020, which enables users to pay their monthly rent via credit cards.

CRED Store

CRED launched CRED Store, an eCommerce platform, which is deemed as a haven for customers with over 500 premium brands across a wide range of categories to shop from.

CRED, which was famous as a credit card bill manager, is now up with some more offerings, including mobile, DTH, and FASTtag recharge options. As per the latest reports dated April 1, 2022, the Kunal Shah-led company has launched its utility bill payments segment, with the help of which the users can now pay their utility bills, including electricity, water bills, and municipal tax, via the CRED app.

Tap to Pay Feature

With the Tap to Pay feature Android users with NFC capabilities can pay without physical cards or wallets by tapping their smartphones on merchant terminals. CRED launched this feature in February 2022.

BidBlast

BidBlast is a thrilling bidding game that CRED members can only play, and it was launched in December 2022. This will give the CRED members the excitement of bidding without using actual money by using CRED coins.

CRED Flash

CRED launched CRED flash in February 2023; with this launch, customers can make payments using BNPL products within the app and across more than 500 partner merchants.

CRED Escapes

The launch of CRED Escapes in March 2023 will provide a painstakingly designed platform with premium privileges, exclusive events, and lodging. This is consistent with CRED’s cutting-edge strategy, which offers members benefits like spa credits, hotel upgrades, and theme park admission.

P2P Payments

CRED launched a P2P payment feature in April 2023. With this feature, customers of CRED will be able to send money to other users via UPI IDs or contact numbers using P2P payment.

RuPay Credit card-based payments

In August 2023, CRED, in collaboration with NPCI in August 2023, launched Rupay credit card- based payment, and now customers can make UPI payments using their credit cards. This partnership benefits banks and merchants by increasing spending and credit sector inclusion.

Fourth Edition of AWP program

CRED launched its fourth version of the AWP (Accelerated Wealth Program), giving staff members the opportunity to purchase more ESOPs (Employee Stock Ownership Plans) with a quicker vesting period.

According to a March 15, 2024, report, this program gives employees the option to choose to have up to 50% of their pay come from special grant ESOPs. With this initiative, CRED hopes to encourage employee ownership and alignment with the company’s long-term growth trajectory while also rewarding and incentivizing staff members.

Paytm is the top competitor of CRED. It is a fintech app and payments platform that is headquartered in Noida, Uttar Pradesh, India, and was founded in 2010.

PhonePe is another notable competitor of CRED. It is also a digital payment and financial services platform headquartered in Bangalore, India, and was founded in 2015. This app has the largest market share of 50% as of December 2022.

Being a UPI platform that is a mass-volume player, Google Pay is another competitor of CRED. This digital payments platform was developed by the Search engine giant Google itself.

Amazon Pay is also a rival of CRED, which is now all set to provide diverse payment options. The online payments processing app was launched by Amazon and founded in 2007.

MobiKwik is yet another fintech company, that supports digital payment options and is a rival of CRED at the same time. It is headquartered in Gurugram, Haryana, India, and was founded in 2009.

Freecharge is also a company that CRED competes with, after the launch of its mobile bills and utility bill payment services. Originally founded by Kunal Shah and Sandeep Tandon, Freecharge is now owned by Axis Bank.

CRED allows credit card users to pay their bills through its platform and extends rewards for each transaction.The fintech platform also lets the users make their house rent payments, and also avail all the benefits of the short-term credit lines that the app now offers.

Who is CRED founder and CRED CEO?

Kunal Shah is the founder and CEO of CRED.

CRED started in which year?

Kunal Shah founded CRED in 2018.

Is CRED a fintech company?

Yes, CRED is a fintech company founded by Kunal Shah and headquartered in Bangalore.

Is CRED an Indian company?

Yes, CRED is an Indian fintech company.

How does CRED make money?

CRED earns money from listing fees that businesses pay to display their products and offers on its app – CRED collects your financial data as you use the app and continues to pay your bills to offer you better offers in the future. To gain access to this data, banks and credit card companies pay CRED.

Is CRED profitable?

CRED saw its operating revenue grow by 71% to INR 2,397 crore in FY24, up from INR 1,400 crore the previous year. Despite the rise in revenue, the company’s net loss expanded by 22%, reaching INR 1,644 crore in FY24, up from INR 1,347 crore the previous year.

How much is CRED revenue?

CRED saw its operating revenue grow by 71% to INR 2,397 crore in FY24, up from INR 1,400 crore the previous year.

What is CRED tagline?

The tagline of CRED company is Suraksha Aur Bharosa Dono.

Which is CRED parent company?

CRED doesn’t have a parent company. It is an independent fintech platform.

With the rise of technology, it was just a matter of time before people shifted to online transactions. While this mode of payment became popular, many companies introduced the idea of e-wallets. One company that stands out in this space is MobiKwik. It is an Indian fintech unicorn that has made digital payments simpler and more accessible for users.

Behind the success of MobiKwik is a determined leader, Upasana Taku. The company was founded in 2009 by Upasana Taku and Bipin Preet Singh. Taku has played an important role in building the company and taking it to greater heights. Under their leadership, MobiKwik became a prominent player in the fintech industry. In December 2024, the company went public with its IPO opening for public subscription.

In this article, learn more about MobiKwik’s co-founder Upasana Taku, her education, her career, the challenges faced, and more.

Upasana Taku – Biography

Name

Upasana Taku

Birthplace

Gandhinagar, Gujarat

Born

1980

Nationality

Indian

Education

B.Tech in Industrial Engineering (NIT Jalandhar), MS (Stanford University)

Profession

Entrepreneur

Position

Co-Founder, Executive Director & CFO of MobiKwik, Co-Founder of Zaakpay

Upasana Taku was born into a Kashmiri family in Gandhinagar and grew up in a family of academicians. She completed her schooling in Surat and went on to pursue engineering at the prestigious Dr B.R. Ambedkar National Institute of Technology, Jalandhar. Taku holds a B.Tech degree in Industrial Engineering from that institute. She did her MS in Management Science and Engineering from Stanford University, USA.

Upasana Taku – Career

After completing her Master’s, Upasana Taku’s career began in 2004 at HSBC Auto Finance in San Diego. She worked as a Business analyst in product management, where she was successful in many areas, like marketing and outreach, forecasting, and market research. She then joined PayPal in 2006. There, she worked as a Senior Product Manager. During her tenure at PayPal, she learned about payment systems in the Americas, Europe, and Asia. Apart from that, she also gained knowledge about risk detection and fraud management, user experience, and design at PayPal.

All these experiences laid a solid foundation for the founding of MobiKwik in 2009. In 2012, Upasana Taku launched Zaakpay, a payment service by MobiKwik. It offers mobile and online payment solutions to eCommerce companies in India, staying true to the values of its parent company.

Currently, Upasana Taku serves as the Co-founder, Executive Director, and CFO of MobiKwik, where she continues to work on the company’s financial strategies and growth.

Bipin Preet Singh and Upasana Taku – MobiKwiki Co-Founders

In 2008, although she had a comfortable life with her corporate job, she realized that she no longer wanted to be a corporate drone. According to her, work was becoming too easy, even though she worked on some high-impact projects and accumulated millions of dollars. But she wanted to come back to India and contribute to the Indian startup ecosystem. Well, this was the turning point of Taku’s career!

Her family didn’t support her decision to return to India, as they saw it as a big risk. At PayPal, she had a successful career, and she enjoyed a comfortable life. Despite all this, she was back in India in 2008.

While she was figuring out her next steps, she worked with Drishtee, a rural microfinance NGO, in Bihar and Uttar Pradesh, helping to empower local communities while gaining a deeper understanding of the challenges and opportunities in rural India.

In the subcontinent, she met a lot of people and extracted ideas about the buzzing sectors and unsolved gaps in the business and startup ecosystem. According to her, a wallet like PayPal was not popular in India. Therefore, users could never imagine a cashless world. Well, the example of India gave the idea to resolve this gap and work for the advancement of technology in the country.

While working on her ideas and project, she happened to meet Bipin Preet Singh in India through a common friend. Together, they started their fintech venture with a shared vision of disrupting the payments industry in India.

“It was a time when our parents would go to a nearby shop to recharge phones and that is when the idea of a mobile wallet business struck us which could pave a way to make consumer payments simpler. Fast forward to now, India is at the cusp of a digital revolution and the payments industry is witnessing a disruption like never before. We kind of saw this coming almost a decade ago,” said Taku in an interview.

Upasana Taku co-founded MobiKwik in 2009 with Bipin Preet Singh, who serves as the CEO and is also her husband. MobiKwik is one of India’s leading mobile wallets and financial services platforms. The app allows users to make payments like mobile recharges, bill payments, and bank transfers. It also offers services like instant digital loans, investment options in digital gold, mutual funds, fixed deposits, and credit card bill settlements.

A key feature of MobiKwik is Pocket UPI. This allows users to make UPI payments without linking their bank accounts. Under Upasana’s leadership, MobiKwik has expanded its services, making it one of the most trusted and widely used platforms in India.

Upasana Taku – The Journey of MobiKwik’s Growth and Milestones

Upasana Taku’s Mobikwik is very simple and need-based. Initially, they launched the company as a recharge platform, and soon, within a few years, it became the face of mobile wallets in the country. At a time when people were dependent on physical cash for a trivial amount like INR 10, Taku revolutionized the sector by bringing the concept of a physical wallet onto the big stage. Presently, a millennial or Gen Z cannot imagine going to a shop for small recharges; all he/she need is to use an app to cover all the recharges. Now, Mobikwik has grown exceptionally as a company. In 2010, the company hired its first employee, and it was somehow very difficult for the team to find someone with the same mindset to serve the community.

In 2011, the team grew very slowly, with a team member count of six! They were dependent on the home-office sector. Even on their wedding day, Taku and Bipin Preet had to work for the company! Later in 2011, they rented their first office which had five rooms. Within a short period, they were growing at an exceptional pace and were a team of 35 people by June 2012. In September 2012, the team applied for RBI’s PPI license, and they received it in July 2013.

This was a milestone for the team as it was a symbol of their growth. The first round of the company’s funding was $5 million, which enabled them to shift to a larger office in Udyog Vihar, Gurugram, with 50 employees. The second round of funding came in 2015, they were able to draw funding of $25 million from Sequoia Capital, American Express, Tree Line Asia, and Cisco Investment.

Under her leadership, MobiKwik achieved major milestones, becoming a unicorn startup in October 2021 and launching its IPO in December 2024.

Upasana Taku’s journey has not been easy. When she was starting MobiKwik, she faced some tough challenges, especially because she was a woman in a male-dominated field. During investor meetings, she was often asked personal questions like why she wasn’t married by 30 or how many children she had. People even mistook her for her husband’s assistant instead of recognising her as a co-founder. New employees at the company would also question whether they should report to her or a male manager.

Taku faced gender bias in the investor meetings as well. She shared that some financiers told her they preferred male founders. In response, she would confidently say that her male counterparts might not be able to answer their questions as well as she could. She made it clear that she would never work with such people.

Despite these challenges, she remained focused, communicated clearly, and continued working towards the success of her company. Even when she was pregnant, she didn’t slow down. Upasana continued working and even attended a board meeting just a day before her cesarean surgery. Coming from a lower-middle-class background, she worked hard to earn a scholarship to study at Stanford University in the US.

While things are slowly getting better for women in business, Upasana acknowledges that there is still progress to be made. Her story is a great example of how, with hard work, determination, and courage, women can overcome any challenge.

Upasana Taku – Success Mantra

Taku’s mantra “Kick up a storm or die trying” has helped her to stay focused in difficult times. According to her, Tenacity is the key. Hence, her hard work and desire to serve the startup community have made her an inspirational figure for many aspiring entrepreneurs.

Upasana Taku – Awards and Recognitions | First Woman to Lead a Payments Company in India

Forbes “Asia’s Women to Watch (2016)”

Best Woman Entrepreneur Award 2017 by Associated Chambers of Commerce and Industry of India (ASSOCHAM)

In 2018, she received an award from the President of India for being the First Woman to lead a Payment Gateway Startup in India.

Forbes Asia’s Power 25 Businesswomen (2019)

In 2024, she was honoured with the ‘Unstoppable Icon’ award and recognised as India’s Leading Tech Founder & one of the Top 15 Richest Self-made Women in India.

In April 2025, Taku was recognized in Fortune India’s “100 Most Powerful Women in Business 2025” list, celebrating her impactful leadership and achievements in fintech.

Taku has been appointed as the Vice-President of the Executive Committee at the Unified Fintech Forum (formerly DLAI).

Upasana Taku is the co-founder and CFO of Mobikwik, India’s leading mobile wallets and financial services company.

What is Upasana Taku age?

Upasana Taku was born in 1980 into a Kashmiri family in Gandhinagar and grew up in a family of academicians.

What is Upasana Taku education?

Upasana Taku’s education includes a B.Tech in Industrial Engineering from NIT Jalandhar and an MS from Stanford University.

What is Upasana Taku net worth?

While the exact net worth of Upasana Taku is not publicly available, in 2024, she was recognised as India’s Leading Tech Founder and one of the Top 15 Richest Self-made Women in India by CNBC-TV18.

What is Upasana Taku’s MobiKwik net worth?

As of May 12, 2025, MobiKwik’s market capitalisation stands at approximately INR 1,925 crore (around $232 million), based on its current share price of INR 247.80. This reflects a significant decline from its peak valuation of INR 4,102 crore (approximately $494 million) during its IPO debut in December 2024.

Who is Zaakpay founder?

Zaakpay, co-founded by Upasana Taku and Bipin Preet Singh (also MobiKwik co-founders), is a payment gateway service provided by MobiKwik. It focuses on fast, innovative digital payment solutions, tackling challenges in payments, reconciliations, and user experience. Recently, Zaakpay received RBI approval to operate as an online payment aggregator, further enhancing its capabilities.

Company Profile is an initiative by StartupTalky to publish verified information on different startups and organizations.

The payment was an area marred with currencies, chaos, and uncertainties. This ushered in the ATM facilities and the ATM-cum debit cards for banking customers. However, even after ATMs came into being in India, the effective usage of cards in physical shops and for other merchants was still fraught with numerous concerns. To mitigate these, Pine Labs was established.

Founded in 1998 as a simple card-based payment and loyalty program, Pine Labs now stands as an Indian merchant platform company to extend financing and last-mile retail transaction technology for the merchants and its customers.

However, it was in 2009 that Pine Labs’ real payments journey began when it ventured into the mainstream payments space and decided to provide solutions to the merchants by connecting to banks and other financial services with the all-new Pine Labs PoS machines. The company was acutely aware that merchants were seeking solutions to enhance their engagement with customers during the payment process. So, it began partnering with banks and payment aggregators and ensured its PoS machines could process all forms of digital payments.

Pine Labs currently provides merchant platform support and makes software for point-of-sale (PoS) machines. The company currently boasts of having more than 70,000 retailers in India including biggies like Mark’s and Spencer’s Retail, Pantaloons, Westside, and more. It is also a unicorn, which joined the coveted club of Indian unicorns in January 2020 by raising an undisclosed amount from the American multinational company, Mastercard, thus becoming the first Indian unicorn startup in 2020 to emerge as a unicorn.

StartupTalky covers the full journey that Pine Labs witnessed including all the information about the company, its Founders and Team, Name, Tagline and Logo, Mission and Vision, Business and Revenue Model, History, Challenges, Startup Story, Competitors, Funding and Investors, and more.

Pine Labs is an Indian merchant platform company that provides financing and last-mile retail transaction technology founded in 1998.

Every day merchants use Pine Labs PoS machines to increase revenue whilst reducing costs, complexity, and risks. This gives Pine Labs a unique opportunity to participate in its growth journey. It focuses on the merchants’ needs, revenue generation strategies, last-mile retail transaction technologies, data analysis, and experiences for their shoppers and customers. The company offers a full-stack merchant platform that is a unique blend of technology and financial solutions.

Pine Labs’ solutions, which are used by merchants from diverse sectors, are now used by over 100,000 merchants in India, and several other Asian countries. In India alone, the company’s cloud-based platform powers over 350,000 PoS in over 3,700 towns.

Pine Labs – Name, Tagline, Logo and its Meaning

Pine Labs is driven by the tagline “We make your business future-positive.“

The logo has a bright green double arrow symbol pointed Northeast and denotes growth, prosperity, and optimism.

Pine Labs Company Logo

Pine Labs – Startup Story

In the beginning, the company’s focus was clearly on large-scale, smart, card-based payment and loyalty solutions for the retail petroleum industry. It was in 2009 that the real payments journey of the company began when it ventured into the mainstream payments space to provide solutions with its PoS machines to merchants, connecting them to banks and other financial services. The company partnered with banks and payment aggregators and ensured that its machines could process all forms of digital payments.

By 2012, Pine Labs had redefined its payment technology offerings and grown into a company that pioneered the smart, cloud-based unified point-of-sale platform, designed to reduce costs and drive revenues for retailers. Its alliances with top banks and brands gave the company the ability to offer multiple services to the merchant through its platform.

Thus, it evolved into a merchant platform that encompasses solutions around payments, risk assessment, multi-channel analytics, merchant lending and insurance, brand offers, cashback, integrated billing, and more. It currently boasts a network of over 21 financial services institutions and 100 brands.

The year 2017 saw Pine Labs lay its first global footprint when it entered Malaysia with an exclusive partnership with CIMB Bank. And today, Pine Labs is well into building the world’s most robust merchant platform that brings together technology and financial solutions to meet every need of the modern merchant.

The founders of Pine Labs are Lokvir Kapoor, Rajul Garg, and Tarun Upadhyay.

Lokvir Kapoor

Lokvir Kapoor is recognized as the Executive Chairman and Co-founder of Pine Labs. Kapoor is an IIT Kanpur alumnus from where he obtained a BTech in Mechanical Engineering. He eventually went on to complete an MBA from IIM Bangalore. Lokvir previously worked with Schlumberger in the areas of financial management and business development in India and abroad before he co-founded Pine Labs in 1998.

Lokvir Kapoor, Founder of Pine Labs

Rajul Garg

Currently known as the Co-Founder and Managing Partner of Leo Capital Holdings, Rajul Garg has been the Co-founder of Pine Labs and also served as the CEO of the company for over 5 years post which he remained as a Board member for more than 4 years. Leaving the company Rajul co-founded GlobalLogic where he served as the Co-founder and COO and SVP. Garg then became a Consultant and Angel Investor for a considerable amount of time. Sunstone Eduversity was another company that Rajul co-founded. He was also the CEO of the company. Rajul Garg has a Btech in Computer Science from IIT Delhi.

Rajul Garg, Founder of Pine Labs

Tarun Upadhyay

Tarun Upadhyay was a Co-founder and CTO at Pine Labs. Upadhyay has an integrated MSc. in Mathematics and Computer Applications from IIT Delhi. Tarun has a streak of co-founding companies including GlobalLogic, hCentive, and Gallop.ai in most of which he served as the co-founder and CTO except for Gallop.ai, where Tarun was appointed as the CEO.

Tarun Upadhyay, Founder of Pine Labs

Amrish Rau is currently the CEO of Pine Labs. He assumed his office with the Noida-based fintech unicorn in March 2020. He has previous experience of being the CEO of First Data and Payu India.

Amrish Rau, CEO Pine Labs

Pine Labs has a company size of 1001-5000 employees.

Pine Labs – Mission and Vision

Pine Labs’ mission statement says, “Maniacal focuses on creating a product and services platform that widens access and accelerates commerce for merchants in each local market we operate in.“

“We believe that every business can grow exponentially with technology and capital” goes the vision statement of Pine Labs.

Pine Labs – Products and Services

The company provides mobile point of sale (PoS) machines that allow merchants to accept credit and debit card payments. Some offerings of Pine Labs include Instant EMI, Instant Discounts, Cashback Programs, PaybyPoints, Loyalty Solutions, e-wallet, Targeted Promotions, Dynamic Currency Conversion, and Gift Solutions.

Pine Labs announced the launch of the merchant commerce platform Plural on October 14, 2021, with which the company forayed into the payment gateway business. This sets Pine Labs as a direct competitor against companies like Razorpay, PayU-Billdesk, CCAvenue, and Paytm. Plural Gateway, Plural Checkout, and Plural Console are the 3 products that the company launched to serve its merchant base of over 5 lakhs. These products can be defined as:

Plural Gateway – Plural Gateway will help the merchants avail of a single payment dashboard for different kinds of payments, including Unified Payments Interface (UPI), and credit and debit cards.

Plural Checkout – Plural Checkout serves as a Mobile SDK (Software Development Kit), which aims to boost the performance of the payment gateways for Android and iOS users.

Plural Console – Designed as a Payment Orchestration Platform (POP), Plural Console will offer a single tech framework to trigger transactions via multiple payment gateways, as mentioned by the company in a press statement.

Pine Labs Plural is currently processing $380 mn in monthly transactions, as of August 6, 2022. This would grow by 10-15X in the next 2 years.

Pine Labs – Business and Revenue Model

After two decades of working closely with merchants, Pine Labs now helps merchants sell more, grow more, and build more with greater efficiency. It serves the merchants’ omnichannel needs. By leveraging technology and domain expertise, it caters to merchants of all sizes helping them to thrive in the changing global marketplace.

The Pine Labs business model is altered as per its merchants’ needs. The payments unicorn introduced advanced, cloud-based point-of-sale (PoS) machines that enhanced its engagement with customers during the payment process. Pine Labs has restructured the payment technology space whilst contributing hand in hand to the world’s digital economy as well. It is also credited as one of the oldest fintech companies in India.

Pine Labs depend heavily on the sale of their products, like the POS payments devices. Furthermore, it also gains commissions from the sale of its services. The company through the income it gets from the interest on fixed deposits and current investments.

Pine Labs – Revenue and Growth

Pine Labs has a network of over 150K merchants across 3700+ cities in India and Malaysia.

Transactions on Pine Labs machines can be initiated by cards, QR codes, or phone number billing. The company also offers working capital loans, loyalty services via PinePerks, etc. Pine Labs has always led the PoS business and has provided card-swiping terminals to merchants. To expand its set of offerings, Pine Labs is currently developing Buy Now Pay Later (BNPL), invoice management, gifting, and eCommerce solutions.

Some of its partners include Apple, Google Pay, Samsung, Sony, etc. The company has raised $310.8 Million from investors such as Sequoia India, PayPal, Temasek, Actis Capital, Altimeter Capital, Madison India Capital, and Sofina.

Here are some of the growth statistics of the company at a glance:

It is one of the oldest fintech companies in India.

It boasts of having around 140,000 merchants in India and other Asian countries.

Pine Labs platform powers over 350,000 PoS terminals in India across 3,700 cities and towns in India and Malaysia.

It has more than 70,000 retailers across India.

Pine Labs has partnerships with more than 15 major banks, 7 financial institutions, and more than 100 brands that are a part of Pine Lab’s platform that processes payments of around $30 Bn each year.

Pine Labs Launches Mini – A QR-Device

Pine Labs has recently introduced an innovative point-of-sale device known as the Mini, which stands out for its remarkably affordable price tag of only Rs 1,999, offering a cost-saving alternative that is roughly one-third the expense of traditional card-swipe machines.

What sets the Mini apart is its versatile functionality, as it not only can generate dynamic QR codes for UPI payments but also seamlessly accommodates contactless card payments, making it a convenient and cost-effective choice for businesses.

Navnit Nakra, CRO, Pine Labs, said, “QR-based and card tap payments are a perfect solution for Indian consumers on the go. On the merchant side, an absolute must is a fast checkout experience and the elimination of the cost barrier in point-of-sale digitisation. Addressing these needs, we are delighted to launch a QR-first, card-accepting, cost-effective PoS solution called Pine Labs Mini.”

This cutting-edge device is a departure from the norm in the Indian market, where most point-of-sale (PoS) devices are primarily designed for debit and credit card transactions. Pine Labs’ Mini device, on the other hand, places a strong emphasis on QR code-based payments and contactless card tapping, catering to the evolving preferences of modern consumers and businesses seeking a more versatile and seamless payment experience.

Pine Labs-owned Setu would now operate as an account aggregator

Setu, which is now owned by Pine Labs, has received an in-principle license from the RBI via its subsidiary, Agya Technologies, which can now operate as an account aggregator, as per reports dated July 7, 2022. For the uninformed, account aggregator AA acts as an RBI-regulated entity that has the NBFC-AA license and

helps individuals securely and digitally access and share information between two financial institutions, where one of them can be a provider where he/she has an account while the other can be any of the regulated financial institutions in the AA network. However, it is important to note that they cannot share data without the consent of the individual. The same AA approval was granted to PhonePe and NSDL E-Governance in 2021. The payment aggregator license acquired by Setu would, therefore, now make Pine Labs

Pine Labs – Financials

Over the past five financial years, Pine Labs has experienced modest revenue growth accompanied by increasing expenses, leading to sustained losses.

Particulars

FY24

FY23

FY22

FY21

FY20

Revenue from Operations

INR 1,317 crore

INR 1,281 crore

INR 1,017 crore

INR 726 crore

INR 846 crore

Expenses

INR 1,624 crore

INR 1,402 crore

INR 1,294 crore

INR 996 crore

INR 961 crore

Profit/Loss

INR -187 crore

INR -56 crore

INR -259 crore

INR -248 crore

INR -94 crore

Pine Labs Financials

Pine Labs Revenue

In FY24, total revenue grew by 2.8% to INR 1,317 crore, up from INR 1,281 crore in FY23. This modest increase was primarily driven by a 39.2% rise in device sales and other income, which offset a significant 44.5% decline in revenue from gifting solutions.

Revenue Source

FY24

FY23

Transaction Processing & Settlement

INR 805 crore

INR 793 crore

Gifting Solutions

INR 111 crore

INR 200 crore

Device Sales & Other Income

INR 401 crore

INR 288 crore

Total Revenue

INR 1,317 crore

INR 1,281 crore

Pine Labs Expense Breakdown:

Total expenses increased by 15.8% in FY24, reaching INR 1,624 crore compared to INR 1,402 crore in FY23. This rise was largely due to a 23.9% increase in other expenses, which encompass materials, travel, advertising, and maintenance costs.

Expense Category

FY24

FY23

Employee Benefits

625

607

Legal & Professional Fees

200

150

Other Expenses

799

645

Total Expenses

1,624

1,402

PineLabs Profit/Loss

Profit Metric

FY24

FY23

Gross Profit

INR 1,317 crore

INR 1,281 crore

Operating Profit

INR -307 crore

INR -121 crore

Net Profit/Loss

INR -187 crore

INR -56 crore

The net loss for Pine Labs escalated to INR 187 crore in FY24, a significant increase from the INR 56 crore loss reported in FY23. This rise in losses is attributed to the disparity between modest revenue growth and substantial increases in expenses.

Quick Summary

Revenue: Increased by 2.8% to INR 1,317 crore in FY24, primarily due to higher device sales and other income.

Expenses: Rose by 15.8% to INR 1,624 crore, driven by higher costs in various operational areas.

Net Loss: Tripled to INR 187 crore, reflecting the imbalance between revenue growth and escalating expenses.

These financial trends suggest that while Pine Labs is achieving revenue growth, the company faces challenges in managing rising operational costs, which are impacting profitability.

Pine Labs has seen 13 rounds of funding in total and has received nearly $1.2 bn in funding to date. Pine Labs is currently valued at over $5 Billion. The total valuation of the company had shot up to $3 billion after the $600 mn funding round that came on July 6, 2021, from Blackrock and Fidelity. Pine Labs’ valuation increased to $3.5 bn, as reported on January 4, 2022.

The last round of Pine Labs funding was worth $50 mn, led by Vitruvian Partners, which it received on March 29, 2022. The previous round was $150 million, which was led by Alpha Wave Global on February 18, 2022.

The fintech giant raised 3 rounds in the past year including the $100 mn round from Invesco and the massive July 6, 2021 round led by Fidelity, BlackRock, and others when it raised $600M. It has also raised $20 mn from the country’s largest commercial bank, SBI.

Pine Labs turned into an Indian unicorn company on January 25, 2020, thereby becoming India’s first unicorn in 2020 after it received an undisclosed amount from Mastercard in the month of January the same year. Here’s a look at the prominent Pine Labs funding rounds and how they were executed:

Date

Round

Amount

Lead Investors

March 29, 2022

Private Equity Round

$50M

Vitruvian Partners

February 18, 2022

Secondary Round

$150M

Alpha Wava Global

January 4, 2022

Corporate Round

$20M

SBI

September 16, 2021

Venture Round

$100M

Invesco Developing Markets Fund

July 6, 2021

–

$600M

Fidelity Management & Research Co. and BlackRock Inc. and others

May 17, 2021

Venture Round

$285M

Baron Capital Group, Duro Capital, Marshall Wace, Moore Strategic Ventures and Ward Ferry Management and other existing investors

December 21, 2020

Secondary Market

–

Lone Pine Capital

Jan 24, 2020

Corporate Round

–

Mastercard

May 31, 2018

Secondary Market

$125M

PayPal Ventures, Temasek Holdings

Mar 13, 2018

Private Equity Round

$22M

Actis

Jul 29, 2017

Corporate Round

$99M

Flipkart

Apr 20, 2017

Secondary Market

–

Madison India Capital

Mar 25, 2009

Seed Round

$1M

Sequoia Capital India

Pine Labs – Shareholding

Pine Labs’ shareholding pattern as of February 2025, sourced from Tracxn:

Pine Labs Shareholders

Percentage

Lokvir Kapoor

3.0%

Peak XV Partners

18.3%

Actis

6.9%

Temasek

6.9%

Alpha Wave Global

3.0%

Invesco

2.5%

Madison India Capital

2.4%

Lone Pine Capital

3.4%

HSBC

1.6%

Sofina

1.6%

Altimeter Capital

1.5%

Smallcap World Fund

1.4%

Tree Line Investment Management

1.4%

Baron Funds

1.1%

Ward Ferry

1.1%

Moore Ventures

0.9%

IIFL Asset Management

1.1%

Duro Capital

0.9%

MW XO Digital Finance Fund

0.6%

Kotak Mahindra Bank

0.5%

Ishana Capital

0.3%

BlackRock

0.5%

Neuberger Berman

0.3%

IC Partners Long Only Fund

0.2%

Lightspeed Venture Partners

0.2%

Falcon Edge Capital

< 0.1%

Bharat Inclusion Initiative

< 0.1%

White Venture Capital

< 0.1%

Octahedron Capital

< 0.1%

Dayzero Holdings

< 0.1%

Relational Capital LLC

< 0.1%

Redbrook

–

Capier Investments

–

PayPal

5.3%

Mastercard

4.7%

Raffles Nominees

2.5%

Marshall Wace

1.4%

Lenarco

1.4%

Nordmann

0.9%

State Bank of India

0.5%

Cgh Amsia

0.4%

DBS Bank

0.3%

Founders Global

0.1%

Citi

< 0.1%

MD Pai Partners

< 0.1%

Pine Labs

–

M3a

–

G1 Innovations

–

Angel

0.2%

Other People

0.3%

ESOP Pool

15.4%

Other Investors

4.2%

Total

100.0%

Pine Labs Shareholding

Pine Labs – ESOPs

Pine Labs has officially announced its ESOP buyback plan, which is worth Rs 100 cr. Amrish Rau, the CEO, and Co-founder of the company took to Twitter to express his happiness. Here is his Twitter post:

Great to have Vitruvian Partners invest in Pine Labs. We continue to build for the long term. Really happy that we did a 100 crores ESOP buy back. We have a great team here, and we have much to do! https://t.co/7q1juPBfkP

The company has again announced the buyback of its shares via the initiation of a buyback program worth $6.07 mn. As per reports dated April 12, 2022, Pine Labs’ board has approved the buyback of its shares from five executives including CEO Amrish Rau. Kumar Sudarsan, Kush Mehra, Dev Anand Sharma, and Rakesh Sharma are the other key executives among the mentioned batch, which the company filed in its regulatory filings in Singapore.

The biggest beneficiary of the buyback program is Amrish Rau, who offloaded shares worth $1.92 million. Kumar Sudarsan, the co-founder of Qwikcilver, the company that Pine Labs acquired in a deal worth $110 million in April 2019, is the next in line, selling shares worth $1.75 million.

Pine Labs – IPO

Pine Labs has already passed a resolution according to the regulatory filings, where it has decided to convert its Singapore-based holding entity from private to public. The company has been renamed Pine Labs Limited from Pine labs Pte to start preparing for its upcoming IPO. Pine Labs is eyeing its US listing within the next 10-12 months. The company is estimated to raise its valuation to $5 billion in the potential IPO ahead. The IPO of Pine Labs is estimated to be around $1 bn in 2022.

The new reports dated January 10, 2022 state that Pine Labs’ preparation for its upcoming US listing is on, where the company will be raising about $500 mn (down from the $1 bn reported previously) at a valuation of $5-7 bn. The plans of the Pine Labs IPO are still on in February 2022, and the company is planning to list on the US exchange at a valuation of $6-7 billion in the IPO.

Pine Labs – Acquisitions

Pine Labs has acquired 5 companies to date. Pine Labs last acquired Setu on June 23, 2022, in a deal worth $70 mn. Setu currently provides payments, data, investments, and lending via its APIs after the expansion of its offerings. After the acquisition, as per the deal, Setu will continue to run independently. Setu was in news on July 7, 2022, for it has received the in-principle license as an account aggregator.

Pine Labs previously acquired the Mumbai-based online payments startup, Qfix Infocomm on February 8, 2022. This acquisition will help its parent with the recently launched Plural platform. After this, Pine Labs acquired a majority stake in Mosambee on April 13, 2022, for an undisclosed sum. This investment increased the valuation of the acquired company by $100 mn. Post the acquisition, the Mosambee team was to operate independently.

The gift solution provider, QwikCilver Solutions, was the first Pine Labs acquisition, which happened on Mar 19, 2019, for $110 million. The Fintech platform from Southeast Asia, Fave was then acquired by Pine Labs in a deal worth $45 million on April 13, 2021.

Here’s a list of the Pine Labs acquisitions to date:

Name of the Acquired Company

Acquired Date

Amount

Setu

June 23, 2022

$70 mn

Mosambee

April 13, 2022

–

Qfix Infocomm

February 8, 2022

–

Fave

April 13, 2021

$45 mn

QwikCilver Solutions

March 19, 2019

$110 mn

Pine Labs – Partnerships

Out of several partnerships, here is a list of some of the prominent partnerships of Pine Labs throughout the years:

Pine Labs collaborated with Kotak Mahindra Bank to scale up its merchant acquiring and point-of-sale systems

The fintech company collaborated with OneCard on September 13, 2021, to enable the EMI options at POS for its customers

Pine Labs announced its partnership on July 22, 2020, with Fave with an aim to expand cashless payment solutions to offline SMEs and enterprises to accelerate digitization

Pine Labs entered the Malaysian market with an exclusive partnership with CIMB Bank in 2017, which asserted its first global footprint

Pine Labs won a list of awards in all these years it has been active:

It won the India Fintech Forum’s IFTA 2021 Award for the “Most Innovative Fintech Product” in November 2021.

The AllTap #WarriorsAtWork campaign of Pine Labs obtained the award for ‘Best Fintech Marketing Campaign’ at CMO Asia, 2021.

Pine Labs was announced the winner of the ‘Best Digital API’ award in the category of Best Technology Solutions at the 11th India Digital Awards conducted by the Internet and Mobile Association of India (IAMAI).

Pine Labs won a payment and fintech award in the category of Best Payment Technology/Solution provider at the 10th India Digital Awards in February 2020. This award was awarded to Pine Labs for enabling the EMI feature on its Android PoS.

Sanjeev Kumar, Chief Technology Officer, Pine Labs, won the Change Agents 2019 award in December 2019 at CIO500 Conclave & Awards 2019, conducted by Enterprise IT World.

Pine Labs won the 2019 Indian Merchant Platform Customer Value Leadership Award at the Frost & Sullivan – 2019 India Best Practices Awards in October 2019.

Pine Labs – Challenges Faced

India’s digital payments growth story has grabbed several eyeballs from international agencies as well as tech giants. From revolutionizing the use of QR codes to Unified Payments Interface (UPI) to enabling point-of-sale via mobile-like devices etc, the innovation in the Indian digital payments industry has awed the world.

While most of these innovative and disruptive ideas haven’t reaped profits, but point-of-sale (PoS) player Pine Labs did in 2017. This, however, is not the case anymore. Being one of the few Indian startups generating profits in FY17, the company spiralled into losses back in FY18. Continuing the trend in FY19 results, Pine Labs reported a net loss of INR 13.5 Cr for the year, as against INR 2.5 Cr net loss in FY18. Though Pine labs swung back to profits and happen to be one of the few companies in FY17 that brought in profits, the company again turned into a loss-making company when last recorded in 2021.

Pine Labs plans to launch its India IPO in H2 2025, according to CEO Amrish Rau. Despite weak market conditions, the fintech firm remains committed to its public listing. Pine Labs provides POS payment solutions, BNPL services, and fintech products, generating revenue from transaction fees, device sales, and lending commissions.

FAQs

What is Pine Labs?

Pine Labs is an Indian merchant platform company that provides financing and last-mile retail transaction technology.

Who are Pine Labs founders?

Lokvir Kapoor, Rajul Garg, and Tarun Upadhyay are the founders of Pine Labs.

How does Pine Labs make money?

Pine Labs earns its revenue from the sale and leasing of its devices, via the services it offers, and through the interest that it receives on fixed deposits and current investments.

What does Pine Labs do?

Pine Labs is an Indian merchant platform company that provides financing and last-mile retail transaction technology, founded in 1998. The company has more than 70,000 retailers across India, including major retail outlets such as Mark’s and Spencer’s Retail, Pantaloons, Shoppers Stop, and Westside.

What is Pine Labs net worth?

The Pine Labs valuation was last estimated to be over $5 billion.

How are Pine Labs acquisitions?

Looking at Pine Labs’ acquisition we can find that the company has acquired 5 companies to date, out of which 3 of the acquisitions came in 2022 itself.

How is the Pine Labs funding?

In terms of Pine Labs funding, the Singapore-registered company has seen 13 funding rounds so far equaling $1.2 billion in funding.

What is Pine Labs business model?

Pine Labs operates a merchant-focused payments and lending platform. It provides point-of-sale (POS) terminals, buy now, pay later (BNPL) services, gift card solutions, and payment processing for businesses. It earns revenue from transaction fees, device sales, and lending commissions.

Jio Financial Services collaborates with BlackRock to revolutionize wealth management and stockbroking in India, making significant strides in the financial sector.

Jio Financial Services, the financial arm of Reliance Industries, has recently tied up with US-based BlackRock to make significant strides in stockbroking and wealth management.

The company announced a significant agreement last month, signing with BlackRock Inc and BlackRock Advisors Singapore Pte Ltd to establish a 50:50 joint venture (JV) dedicated to launching a wealth management and broking business in India.

Jio Financial Services’ partnership with BlackRock, the world’s largest asset manager, is poised to revolutionize the way Indians access and manage their wealth, marking a significant milestone in the evolution of the country’s financial ecosystem. Notably, this marks the second collaboration between Jio and BlackRock, following their successful launch of an asset management venture last year.

With this new partnership, both entities are poised to further strengthen their presence in India’s financial landscape, leveraging their combined expertise to offer innovative solutions tailored to the evolving needs of Indian investors.

This article delves into the game-changing influence of Jio Financial Services and how it is revolutionizing the financial landscape. Jio Financial Services has emerged as a key player in the market, reshaping the way people access and manage their finances.

Jio Financial’s Role in Revolutionizing the Financial Landscape

Jio Financial’s entry into the financial industry has been nothing short of revolutionary. By leveraging technology and digital platforms, Jio Financial has disrupted traditional financial practices and introduced a new era of convenience and accessibility. With its user-friendly interface and seamless integration, Jio Financial has made financial services more accessible to the masses, breaking down barriers and empowering individuals to take control of their financial future.

Jio Financial Services Ltd (JFSL) was incorporated in July 2023. JFSL is a NBFC registered with the Reserve Bank of India. The company is a holding company and will operate its financial services business through its consumer-facing subsidiaries namely Jio Finance Limited (JFL), Jio Insurance Broking Limited (JIBL), and Jio Payment Solutions Limited (JPSL), and joint venture namely Jio Payments Bank Limited (JPBL).

Jio Financial Services is redefining the way people engage with banking, investing, and wealth management. Through its collaborative ventures, like the recent equal joint venture with BlackRock in stockbroking and wealth management, the company is not just expanding its offerings, but also setting new standards for transparency, accessibility, and customer-centricity in the financial sector.

BlackRock’s deep understanding of global markets, combined with Jio Financial’s local insights and digital prowess, creates a potent combination that promises to unlock new opportunities and drive unprecedented growth in India’s financial sector.

By leveraging BlackRock’s world-class asset management capabilities, Jio Financial aims to offer a wide range of investment products and wealth management solutions designed to cater to the needs of both retail and institutional investors.

One of the key areas of focus for the partnership will be the expansion of Jio Financial’s stockbroking and wealth management business. With India witnessing a surge in Demat accounts and a growing appetite for investment opportunities, the timing couldn’t be more suitable for JioFin and BlackRock to join forces and tap into this burgeoning market.

In March 2024, India’s financial landscape witnessed a historic moment as the total number of demat accounts surpassed the 15 crore mark for the first time. This milestone, driven by sustained bullish momentum in the Indian market, reflects the growing interest and participation of investors in the country’s capital markets.

According to Motilal Oswal Financial Services, a leading domestic brokerage house, the total number of demat accounts surged to 15.1 crores in March 2024.

The share price of Jio Financial has been a topic of interest for investors and financial analysts alike.

The soaring share prices of Jio Financial reflect the market’s confidence in its potential and growth prospects.

Should You Invest In RIL & JIO FIN Shares After Q4 Earnings?

Jio Financial Services stock soared to an unprecedented all-time high of Rs 394.70 per share on April 23, surpassing its previous record peak of Rs 384.85 per share. In the past one month, JioFin share has touched a peak of Rs 394.70 and reached a low of Rs 351. This surge underscores the remarkable momentum the stock has gathered in recent months.

On May 2, Jio Financial Services closed at 0.78% up at Rs 379.85 per share on the National Stock Exchange.

On May 2, at 2328 IST, BlackRock shares were trading at 0.56% up at Rs 755.85 per share on the New York Stock Exchange.

As more people recognize the value and convenience offered by JioFin’s services, the demand for its shares has skyrocketed. This surge in share price signifies the market’s belief in Jio Fin’s ability to revolutionize the financial sector and create substantial value for its investors.

We at StartupTalky spoke to financial expert Gaurav Goel, a SEBI Registered Investment Adviser on the current surge in Jio Financial services share price and his outlook about the company.

Considering the recent surge in Jio Financial Services’ share price, what factors are driving investor confidence in the company?

Mr. Goel: The recent surge in the stock price of Jio Financial Services is a reflection of the possibilities in the business model of the company. It is expected to disrupt the existing business models, use technology as a fulcrum, and provide seamless execution across the board. Backed by one of the most powerful and richest business groups in India, this NBFC has been created to provide a one-stop financial services company in the country. This includes payment services, insurance broking, and a newly formed 50:50 joint venture with Blackrock to enter the asset management business in India.

With the expansion of Jio Financial Services into stockbroking and wealth management through its joint venture with BlackRock, how do you assess the potential benefits for investors?

Mr. Goel: Blackrock is one of the biggest investment management companies across the globe, founded in 1988. It manages around 10 trillion dollars in assets (AUM) across a diverse range of equities, fixed income, and money market instruments with sound risk management practices. Their flagship product ‘Alladin’ has been a global disrupter in the financial space. They are not new to India either, having partnered with DSP earlier, but exited the business in 2018. Blackrock is known for its innovative investment strategies, technology-enabled products, and use of data analytics to run its business.

Their venture with Jio Financial is likely to be pathbreaking. They plan to invest up to USD 150 million each and create ripples in the 500-billion-dollar (and growing) asset management industry in India. While Blackrock will leverage its strength of asset management, Jio Financial will use its network and resources to reach out to millions of people across the country.

While the partnership looks attractive and the promise of disruptive delivery is exciting, it won’t be a cakewalk. A low-cost disruption like telecom won’t be easy due to regulatory challenges in the industry. Competition is well-established and intense and existing players will not give up that easily.

In what ways do you think Jio Financial Services’ innovative approach is reshaping traditional banking and investment practices in India?

Mr. Goel: The key differentiation lies in the use of technology, a comprehensive platform with a complete suite of products, risk management capabilities, financial muscle, use of existing network, and world-class strategic partnerships. The disruptor tag would ensure that it’s not taken lightly by other major players in the industry.

Jio Financial Services Financial Results

V.L.A. Ambala, a Research Analyst (SEBI Registered), and Co-founder of Stock Market Today (SMT) spoke to StartupTalky and commented on the company’s prospects.

As a research analyst, how would you advise investors to evaluate Jio Financial Services’ stock and its potential for long-term growth?

Mr. Ambala: My advice for those interested in Jio Financial Services’ stock would be to assess its potential for long-term growth and factor in its fundamentals to make an informed choice. For instance, the company’s recent collaboration with global giant BlackRock for JioFin development adds substantial credibility to the stock. Additionally, JioFin has delivered substantial returns since its listing, indicating promising growth prospects. Hence, I hold a bullish view of this stock. However, I would recommend individuals approach this stock with a long-term mindset, aiming for a holding period of 9 to 35 months to capitalize on its potential.

For those seeking short-term gains, caution is advised as the stock is currently trading in the overbought zone. So, investors may consider investing in parts or waiting for a dip before entering the market. A strategy for averaging could involve monitoring the 50-day Exponential Moving Average (EMA) and adding lump sums at the 200-day EMA to mitigate risks and maximize returns.