When it comes to managing expenses and bills, especially when one has low funds. This becomes really pressurizing and people start looking for sources to lend money from. In such situations, borrowing from friends and family could be embarrassing and hectic. And depending upon banks could cost major interests. So where should we look?

Well by acknowledging these situations and deals, online money lending apps are developed. These provide the facility to lend money through digital platforms without any further issues.

Multiple companies are providing the facility of offering loads immediately with minimal competitive interest rates and required tenure durations. These companies facilitate the loan very easily and quickly as compared to usual bank loans.

With keeping such progress in mind, India has developed numerous digital lending companies whose finances can manage smoothly. India is evolving to a great extent in the digital sector and financial inclusion. The country has cash for transactions. But with the evolving method of development and modernization, India is shifting toward a cashless economy. To understand its development more prominently, let’s look at the top 10 digital lending platforms in India.

Best Digital Lending Platforms in India – Lendingkart Website

The prominent digital lending platform, Lendingkart was founded in 2014. It works by offering different capital loans and company loans vary from small to medium-sized businesses across India. They are widely famous for providing capital completely through an online platform and require minimum documentation for the procedure to begin.

For young entrepreneurs, managing their finances becomes quite hectic and it deviates them from focusing on their business growth. That’s why Lendingkart has taken the initiative to make capital funding easily available for entrepreneurs so they don’t have to worry about the cash-flow gaps. Lendingkart is a company established in Ahmedabad, Mumbai and Bangalore. But, its services are accessible throughout the whole of India.

2. Pine Labs

Lending Platform

Pine Labs

Loan Amount

From ₹25,000 to ₹5 Lakhs

Loan Tenure

90 Days

Best Digital Lending Platforms in India – Pine Labs Website

Pine Labs is one of the leading fintech companies in India established in 1998 that provides digital lending services. The company is quite famous for its incredible facility of transforming the mobile NFC into a card machine and activating the service of accepting all types of payment digitally which also includes the ‘Tap n Pay’ card as well.

Pine Labs have brought tons of services for the retailers including multi-channel, different payment options, brand offerings, risk assessments, analytics, and many more.

It provides working capital loans for small to medium businesses. Their loan application process is quite simple and you can apply for a business loan through their website or their app myPlutus.

Pine Labs’ services and technologies are widely preferred and used by more than 100,00 merchants all across India and also, many Asian companies. According to the estimations, PineLabs’ cloud-based technology has the power of over 350,000 PoS terminals; that too in more than 3,700 cities.

3. MobiKwik

Lending Platform

Mobikwik

Loan Amount

Upto ₹5,00,000

Loan Tenure

6 to 36 Months

Top Loan Aggregators in India – MobiKwik Website

MobiKwik is a very prominent mobile payment company that works by connecting the consumers together with the merchants and many online sellers. The company is established in Gurgaon, Haryana, India.

Mobikwik is a private company that has more than 550 employees. Since the establishment of this company, the company has raised a total of 118 million USD from over 8 funding rounds.

Mobiwik provides instant personal loans. You can download its app and once the loan is approved it will be credited to your wallet.

₹1 Lakh to ₹15 Lakhs (unsecured) or up to ₹2.5 Crores (secured)

Loan Tenure

6 to 48 Months (unsecured), Up to 84 Months (secured)

One of the biggest lending companies, Shiksha Finance, is an education-based finance firm. Shiksha Finance provides the services of funding parents for school fees by reducing the school drop-out rates. It also offers capital to educational institutions for the development of buildings, properties and working capital.

Shiksha Finance has loans that range from INR 10,000 to INR 50,000 with a return duration of 6 to 10 months. The loans which Shiksha Finance provides can be utilized for educational based purposes such as school fees, tuition, luggage and stationary.

5. MoneyTap

Lending Platform

MoneyTap

Loan Amount

Upto ₹5,00,000

Loan Tenure

36 Months

Best Digital Lending Platforms in India – MoneyTap Website

The Bengaluru based lending company, MoneyTap is known for its huge service of offering credit lines for the consumers as their loans, with the partnership with RBL Bank. MoneyTap is now counted among the leading lending businesses. Recently, the company received the license of NBFC for co-lending space together with their lending partners.

MoneyTap has offered many great features among which, the minimal documentation procedure for a personal loan is the most special one. Moreover, its app version also provides the facilities for tracking down your borrowing records.

6. Paytm

Lending Platform

Paytm

Loan Amount

Upto ₹2,00,000

Loan Tenure

6 to 36 Months

Fintech Lending Companies in India – Paytm Website

The biggest digital lending wallet company Paytm is wildly famous in the minds of Indians. The company is established in Noida, Uttar Pradesh. Paytm has grown to a great extent and now, millions of downloads have been made.

The development the company has received is breathtaking. It employs more than 9000 people and has a revenue of a total of $118 million. Paytm is highly specialised in online shopping as well.

Best Digital Lending Platforms in India – PolicyBazaar

The company is counted among the top leading online insurance companies, PolicyBazaar was established in the year 2008 and headquartered in Gurgaon, Haryana, India.

It is online life insurance as well as a general insurance aggregator company. PolicyBazaar is very popular among Indians for its incredible services and holdings. It employs over 2500 people and has an annual revenue of $21 million (as estimated in 2017-18).

The current CEO of PolicyBazaar is Yashish Dahiya who is also one of the founders of this company. It has raised around US$ 346 million through 7 funding rounds.

8. Capital Float

Lending Platform

Capital Float

Loan Amount

₹50,00,000

Loan Tenure

Upto 36 Months

Best Digital Lending Platforms in India – Capital Float Website

Capital Float is one of the leading lending companies in India. It is acquired by CapFloat Financial Services. Capital Float is popular for its amazing service of specialised financial loans and business credits.

Capital Float has a partnership with some prominent companies such as Shopclues, Paytm and Uber. The company lends the potential borrower through its system of proprietary loans. Capital Float is now targeting established store owners and small merchants.

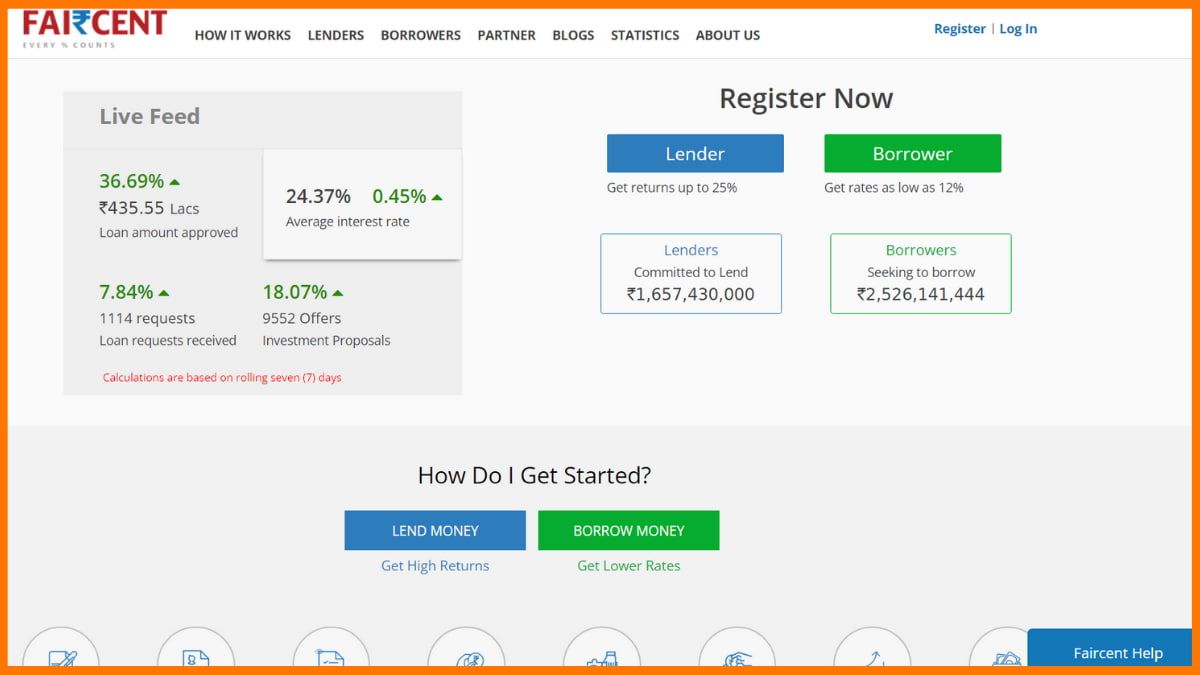

9. Faircent

Details

Information

Loan Amount

₹5,00,000

Loan Tenure

6 to 36 Months

Best Digital Lending Platforms in India – Faircent Website

The largest and first Indian peer-to-peer digital lending platform, Faircent is known to be absolutely amazing. It is officially registered by the RBI. It provides a safe marketplace for people to loan money to a borrower. Faircent facilitates the credit to organizations and individuals who are interested in lending money.

Faircent provides the absolutely convenient procedure of lending the required money to those who need it, at reasonable interest rates.

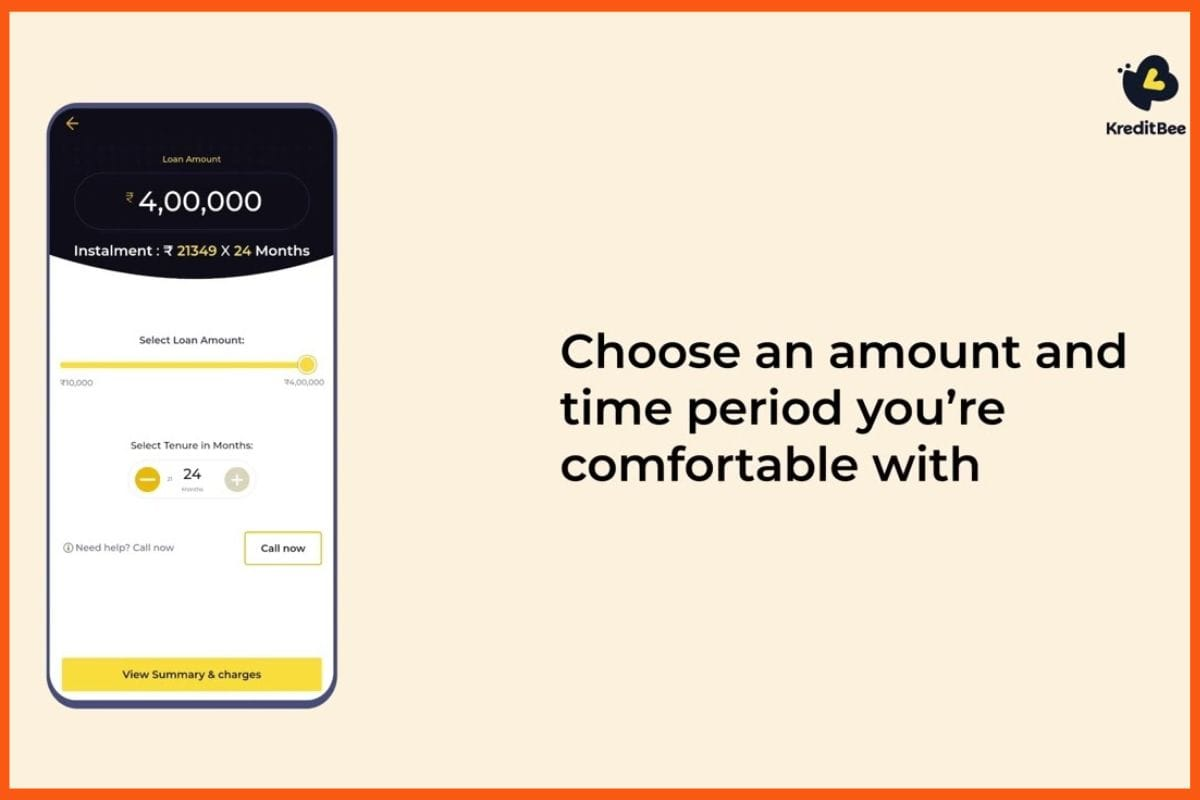

10. KreditBee

Lending Platform

KreditBee

Loan Amount

₹5,00,000

Loan Tenure

6 to 36 Months

Lending Service Providers in India – KreditBee

KreditBee is a Bangalore-based fintech that offers quick personal loans up to INR 2,00,000 for working professionals. Using easy online KYC, the loan process is fast and simple. KreditBee is one of the top lending companies in India.

Backed by trusted investors like ICICI Bank and supported by banks like AU Small Finance, KreditBee serves over 5 million customers.

The process is mostly paperless, sign up on the app, and within 15 minutes, approved loans are transferred instantly to your bank account.

In India, there are many fintech companies that are providing the service of digitally lending money very easily with the minimal documentation procedure. Today, many apps have been developed by these companies to make the transaction of money absolutely susceptible. And for those who require a personal loan or business loan, can easily get one. That’s why we listed these top digital lending companies in India.

FAQs

What are some of the top digital lending companies in India?

Lendingkart, Pinelabs, Mobiwik, Policybazaar, and Paytm are some of the top digital lending companies in India.

How does a lending company work?

Lending companies provide loans to an entity, which is then expected to repay its debt.

How many fintech companies are there in India?

There are around 2,000 fintech companies in India.

Company Profile is an initiative by StartupTalky to publish verifiedinformation ondifferent startups and organizations.

In our haphazard daily life, we tend to get busy with several things and forget about payments and maintaining a log of all the financial transactions. This, sometimes, becomes extremely hectic and might even affect businesses adversely in a whole host of ways. However, with the emergence of numerous business management software, businesses and individuals can manage their businesses effortlessly. Khatabook is one of such reliable software solutions that makes managing business and personal ledgers a breeze!

Founded in 2018 in Bangalore, Khatabook is hailed as India’s fastest-growing SaaS company. Khatabook reminds you through WhatsApp or SMS when the money is due to be paid or collected. forgetting the due dates of payments to be made. Besides, handling multiple businesses will no more be a deal with Khatabook!

The micro, small and medium businesses of the country simply has a new name, Khatabook, which brings safe and secure business and financial solutions to increase efficiency and reduce costs.

Here’s diving into Khatabook’s journey in this StartupTalky article, where we will find out more about Khatabook Founders and Team, Funding and Investors, Startup Story, Tagline and Logo, Growth, Business and Revenue Model, Challenges, Competitors, Future Plans and more.

The latest campaign of Khatabook #DhandeKaDoctor featuring MS Dhoni, urging small businesses to use Khatabook to maintain their account.

Khatabook – Latest News

9th November 2021 – Khatabook has decided to shut down MyStore, the eCommerce enablement of the company, which has been a core product of the company, effective from 15th November onwards.

24th August 2021 – Khatabook concluded its Series C round of funding with a fundraise of $100 million led by Tribe Capital, Moore Strategic Ventures, Alkeon Capital, B Capital Group, Sequoia Capital, and more.

3rd February 2021 – Khatabook released its 2020 statistics. In 2020, Khatabook activated merchants in >95% Indian districts, recording over $100Bn+ in transactions with over 150Mn+ customers.

13th January 2021 – Out of the 7 Indian startups in Y Combinator‘s latest top companies’ list, Khatabook is one among them. India has emerged as an important market for Y Combinator.

Khatabook – About and How it Works?

Founded in January 2019, Khatabook is the fastest growing Saas company in India and one of the fastest-growing SaaS company in the world. It has become India’s leading business management app for MSMEs with 20M+ downloads in a remarkably short period of time. It operates the Android-based Khatabook app that enables companies to keep a digital log of their financial transactions and accept payments online.

Khatabook enables micro, small and medium merchants to track business transactions safely and securely. The app is available in over 12 vernacular languages, catering to a diverse audience in the country.

It helps businesses and individuals manage the business and personal ledgers on their phones and computer devices along with helping them recall the due dates with the help of effective SMS and WhatsApp reminders about the same. This Bangalore-based mobile app service shares WhatsApp and SMS reminders to users when the money is due to be paid or collected.

The Khatabook app has a free ‘Payment Reminders’ feature. With this feature, an automatic SMS is sent to your customers every time a transaction is recorded. Khatabook lets its users keep all details of credits and debits for any number of customers across multiple businesses ready and handy on their phones. Furthermore, Khatabook also helps its customers sync their transactions automatically, download, share and maintain reports of all the transactions, reap all the benefits of the effective QR code-based payments with 0% fees on transactions and more. In short, this app lets merchants do stress-free business.

Khatabook – Industry Details

Khatabook’s founder Ravish Naresh revealed on Twitter that Khatabook activated merchants in >95% Indian districts with 150Mn+ Customers. Based on the Indian MSME Data, Khatabook conducted research and analysis on the credit behavior of people across the country and also the impact of Covid-19 on small businesses.

Over 2020 @Khatabook activated merchants in >95% Indian districts, recording over $100Bn+ in transactions with over 150Mn+ customers. A good chunk of India's retail GDP is already being recorded on the platform and trade flows from across the country are getting digitized. pic.twitter.com/aVcZTlVBGM

Business volumes on credit are 45% higher for South Indian states vs the national average.

Credit given out by Khatabook merchants dropped by 40% in the initial Covid months. It has continued to recover to 80% of pre-pandemic levels by December.

Average days to recover debts increased by 25% during COVID for Khatabook Merchants.

Sectors like travel, construction, apparel were more impacted during 2020.

Khatabook – Founders and Team

Vaibhav Kalpe originally built Khatabook, which was later acquired by Kyte Technologies in 2018. Kalpe later joined the owning team of Kyte before he left the organization. The founding team of Khatabook currently has Ravish Naresh leading the company as the Co-founder and CEO along with other co-founders – Ashish Sonone, Dhanesh Kumar, and Jaideep Poonia.

Khatabook – Founders & Team

Ashish Sonone

The Co-founder of Khatabook, Ashish Sonone is a IIT Bombay Btech graduate in Computer Science. JetSynthesys Pvt. Ltd and Qiosk – News for Professionals were the companies where Sonone worked as a Software Engineer and Consultant respectively before co-founding Frodo and Kyte, in both of which he also served as a Backend Engineer. Khatabook is the third company that Sonone has co-founded.

Dhanesh Kumar

Another Computer Science and Engineering from IIT Bombay, Dhanesh Kumar started with Amazon as a Software Developer, who then realized his entrepreneurial and decided to co-found Knit Messaging, Kyte and now Khatabook, where he is still serving as a Co-founder.

Jaideep Poonia

Jaideep is an IIT Bombay alumnus from where he completed his Btech in Civil Engineering before completing S18 from Y-Combinator. Poonia has also been the co-founder of Knit Messaging, Kyte, and Khatabook as Dhanesh Kumar.

Ravish Naresh

Co-founder and CEO of Khatabook, Ravish Naresh completed his Btech from IIT Bombay, much like the other co-founders of the company, after which he co-founded Housing.com, where he also served as a COO. It was after leaving Housing.com, Ravish co-founded Khatabook, where he is still working as a CEO.

Khatabook currently works with around 300 employees.

Khatabook – Startup Story

The story goes back to 2016, when Ravish Naresh along with his team of college friends, started a digital spend manager app, Kyte.ai. The app helped users understand their expense patterns using their SMS alerts. Kyte initially had good traction but did not reach the expected growth scale. Also, the team realized all their users were based out of metropolitan cities.

On researching, they found that first-time online users did not deal with digital transactions, and they still rely on traditional khata or ledger books. As per Ravish, they wanted to build something that people want and then try to build a business around it.

That is when the idea for Khatabook developed, and they started to work on a simple cash management app, which they named Khatabook. The parent company of Khatabook is Kyte Technologies.

Khatabook – Mission and Vision

The mission statement of Khatabook says, “Empowering Udhari Khata (Book-Keeping)”.

“Started with a vision of transforming India’s small shops, today we are the biggest player in the small business segment digitizing a sector that forms the backbone of our economy. We are looking to work closely with the government and financial institutions to strengthen our market leadership and help MSMEs increase their income while making them more efficient and competitive,” said Ravish Naresh, CEO of Khatabook.

Khatabook – Tagline and Logo

The tagline of Khatabook is Business Hua Easy! The app lets every business go digital instead of following the same traditional method of book-keeping and making it easy to grow their business.

Khatabook’s logo itself signifies what the company is all about. It maintains a digital record of all the transactions we make, something which our actual ‘Khatabook’ (the diary in which we maintain our financial record) does.

Khatabook Logo

Khatabook – Business Model

Khatabook is a mobile app that helps small merchants to digitize their accounting and credit balance recording. It helps to reduce the burden of bookkeeping and accounting. It is just like having a khata in your pocket. The business model of Khatabook is making “Bharat” / India come online.

It is 100% free to use and secure for all types of businesses with which shop owners can record credit (Jama) and debit (Udhaar) of customers. But Khatabook has no revenue source at present.

Ravish Naresh, CEO of Khatabook, said they’re now developing the app to provide a complete financial solution for small businesses. The startup has plans to bring a host of new features onto the platform and UPI payment is next on the line.

Khatabook has seen some growth in the past two and a half years, where it has emerged as an integral part of the MSME community in almost every district in India. A majority of the merchant users on the Khatabook platform have embraced the digital practices dumping their offline business practices.

Furthermore, Khatabook has also introduced 3 other solutions apart from the Flagship Khatabook for the benefit of the MSMEs:

Biz Analyst – This is a leading SaaS business management solution from Khatabook designed to offer premium value-added on-demand services like sales and purchase reports, livestock updates, and other MIS reports. Biz Analyst can be integrated with Tally ERP9 and allows an overall view of the business operations.

Pagarkhata – This is a staff management platform for businesses by Khatabook which aims to help merchants to turn the staff attendance, payroll/wages, attendance updates, leaves, payments, and other processes digital.

Cashbook – Cashbook is another platform by Khatabook built as a cash handling and tracking solution. Furthermore, it also helps with cash sales and expense management.

In 2020, Khatabook has active merchants in 95% of Indian districts, recording over $100 Billion in transactions with over 150 million customers.

Khatabook has recorded total revenue of Rs 17 crore during FY21, thereby registering a 25.3% decline from Rs 24.4 crore. The startup’s revenue from operations, currently recorded at Rs 16.9 crore, witnessed a dip of around 30.7% from Rs 24.4 crore that it posted in FY20. On the other hand, the other income of the startup rose from Rs 12.7 crore in FY20 to Rs 21 crore in FY21.

Diving into the profit-loss segment, it has been discovered that Khatabook has managed to reduce its loss by 63%, which has been brought down from Rs 89.5 crore to Rs 33 crore. This is primarily due to the selling of its intellectual property, some of which it sold to its holding company, Kyte Technologies Inc. for around Rs 57 crore.

In FY22, the company experienced significant growth in its operating revenue, surging from Rs 17 crore in 2021 to an impressive Rs 71 crore. However, this growth was accompanied by a corresponding increase in total expenses, which escalated from Rs 109 crore in FY21 to Rs 189 crore in FY22. Consequently, the company’s losses also saw a substantial rise, soaring from Rs 33 crore in FY21 to Rs 111 crore in FY22 during this period.

Here’s a look at the financials of Khatabook:

Khatabook Financials

Operating revenue for the Khatabook increased by 14% in FY23 to Rs 81 crore. Conversely, there was a marginal rise in losses of 4% to Rs 125 crore. Due to increased employee benefit costs (wages, salaries, PPF, etc.), which amounted to over Rs 142 crore, the company’s total expenses stayed steady at Rs 223 crore, a slight increase from Rs 189 crore in the year FY22.

Khatabook – Growth

Khatabook has registered around 10 Million monthly active users and the numbers are growing.

Growth had an excellent trajectory, which did take a hit during the lockdown in line with other external factors. With the relaxation of the lockdown, the company started reviving the business at a steady pace. The revival has been faster with users in tier-2 and tier-3 cities of India.

As a very relevant offering for merchants in the pandemic, the company also launched the MyStore app to enable them to take their stores online in 15 seconds and continue doing business through their preferred communication channels.

Within a month after the launch, more than 2.5 million merchants across India have installed MyStore. Khatabook also initiated work from home active, 24/7 call center support for merchants. Currently, the revenue model of Khatabook depends on its funding.

Some key growth highlights would include:

5 crore+ registered businesses

A spread over 4000+ cities of India

Powered by popular investors like Sequoia Capital, DST Global Partners, Y Combinator, Tencent, B Capital Group and more

Khatabook – Acquisitions

Khatabook has acquired Biz Analyst on March 25, 2021, which remains the company’s maiden acquisition.

Khatabook – Awards and Achievements

Some of the popular awards and achievements that Khatabook has seen so far are:

It was declared as the Winner of Nasscom League of 10 in the Emerge50 Awards 2020

The company’s app won the Best Innovative Mobile App award at IAMAI 2020

mCube announced Khatabook the winner of the Best Content in a Mobile Marketing Campaign in its awards ceremony in 2020

Khatabook – Partnerships

Khatabook currently partners with the former skipper of the India cricket team, M.S. Dhoni, who is an investor as well as the brand ambassador of the company. The strategic partnership was announced on March 17, 2020.

Khatabook – Challenges Faced

Khatabook also faced a shortage of money during its initial days just like other new startups. Ravish, the CEO of Khatabook realized that they need to look into serious funding options.

In the series A phase, they were struggling a bit with the funding. The growth hit them fast, so the seed round took place in 5 bridges. It was the highest in the history of funding for Sequoia.

“Well, the struggles were mainly money-related. We knew we were working on something important and kept going with it. Often it was difficult to imagine the future of our initiatives with no funding, but perseverance is what got us where we are today,” said Ravish Naresh.

He also said that the adoption of their product was not only dependent on the app’s visibility and convenience but also on educating users, not just for the app but also for using digital technology in general. The biggest hurdle was to persuade offline shopkeepers to come online and train them for digital transactions.

Switching away from the convention is understandably tricky and daunting for merchants who mainly have offline workflows. Persuading traditional enterprises to embrace the digital still remains a crucial challenge for them.

“It is important to build something that people want and then try to build a business around it, and that is exactly what the team did.” said Ravish.

Khatabook announced the shutdown of MyStore on November 10, 2021. The eCommerce enablement product was one of the core products of the company, which also contributed to the expansion of the company by raising funds along with helping the company with its bookkeeping requirements.

“Thank you for being a part of the MyStore journey. We are planning on discontinuing the MyStore App. Your MyStore App won’t work from 15 November 2021,” goes a blog post from the company.

The company has further asked its users to download their invoices by sharing order invoices before doing away with the app.

Khatabook had previously been dragged into a legal fight with its rival, Dukaan over the plagiarism of the name when MyStore was named ‘Dukaan by Khatabook’, in August 2020. Khatabook later decided to change it to ‘MyStore by Khatabook after a legal battle of around four months. The tagline of the app, however, remains the same, ”Create Your Online Dukaan in 15 Seconds” to date on Play Store.

Khatabook – Funding and Investors

Khatabook has raised a total of $186.5M in funding over 4 rounds. Their latest funding was raised on 24th August 2021, from a Series C round. Khatabook is funded by 34 investors in total. Tribe Capital and Moore Strategic Ventures are the most recent investors. The valuation of Khatabook was estimated to be around $600 Million in August 2021.

In a strategic move aimed at optimizing costs and prolonging the company’s financial runway, the organization recently made the difficult decision to implement workforce reductions, resulting in the departure of over 40 employees from various departments. These actions were undertaken as part of a broader effort to navigate the challenges faced by growth-stage companies.

While undoubtedly a tough choice, the company’s leadership recognized the importance of preserving its financial stability and ensuring a sustainable future. This move reflects a commitment to adaptability and resilience in an ever-evolving business landscape, with the hope that these measures will ultimately position the company for long-term success.

“Khatabook has laid off 42 employees across sales, marketing and analytics, and technology verticals,” said one of the sources requesting anonymity. “People who lost their jobs in the exercise have been given standard severance packages including 3 months salary among others.”

Khatabook – Future Plans

Khatabook plans to expand and achieve two to three times business growth by simplifying the traditional way of doing business. Remaining committed to India’s MSME segment, Khatabook will be adding services to streamline and simplify business processes for the merchants.

“Committing to a goal is essential for business directions and decisions. One thing that pandemic has taught us is that we need to think through the most unlikely scenario and make sure we are relevant in all possible scenarios or are agile enough to change our direction as per the need of the hour,” says Ravish.

Khatabook has already managed to build a widely accepted tech ecosystem for the MSMEs across the country and will now concentrate on the disbursement of financial services through its tech platforms. These financial services will further enable smooth lending, payment, and deposits in the MSME space.

Khatabook is eyeing the right partnership opportunities to seamlessly roll out the solutions that would benefit the economic aspirations of countless small businesses.

Khatabook has announced a buyback scheme of ESOPs worth USD 10 Million in order to acknowledge the contributions of its employees, the ex-employees and the early investors who stayed by the company and helped it grow. The employees who are eligible for the ESOP scheme would be able to sell up to 30% of their vested options. Meanwhile, Khatabook has also expanded its ESOP pool to $50 Mn.

Furthermore, Khatabook is also looking to strengthen its talent base by hiring employees for the engineering, product, design, analytics, and data science departments.

Khatabook – FAQs

What is Khatabook?

Khatabook is the world’s fastest-growing SaaS company. It is India’s leading business management app for MSMEs that enables companies to keep a digital log of their financial transactions and accept payments online. It’s like having a khata in your pocket.

Is Khatabook an Indian app?

Yes, Khatabook is an Indian app founded in 2019 with an aim to reduce the burden of bookkeeping and accounting.

Which company owns Khatabook?

Kyte Technologies is the Parent Company of Khatabook.

Who is the CEO of Khatabook?

Ravish Naresh is the CEO and Co-founder of Khatabook.

Who are the founders of Khatabook?

Khatabook was founded by Ashish Sonone, Dhanesh Kumar, Vaibhav Kalpe (Ex-Khatabook), Jaideep Poonia and Ravish Naresh in 2019.

How does Khatabook make money?

The Khatabook revenue model is non-existent at the moment. Naresh says their focus is now on developing the app to provide a complete financial solution to small businesses.

What is the use of Khatabook?

Khatabook app enables MSMEs to keep a digital log of their financial transactions and accept payments online.

What is the valuation of Khatabook?

The valuation of Khatabook was estimated to be around $600 Million.

Company Profile is an initiative by StartupTalky to publish verified information on different startups and organizations. The content in this post has been approved by muvin.

Neobanking services are revolutionising both the financial and Fintech sectors in India. Fintech ecosystem is gearing towards better usage of Artificial Intelligence and improving customer satisfaction with popular neobanks in India like- RazorPayX, Jupiter, and Kotak811, to name a few. muvin is an emerging startup that enables a seamless experience for teens which includes pocket money management, financial literacy, and understanding savings from a young age, amongst others. It is a pocket-money app that encourages children to learn to manage finances.

Read the startup story of muvin and know about its founders, business model, challenges, and growth.

While parents/guardians can create an account to enable their dependents/children with an independent wallet, muvin also empowers India’s college going students to set up their own wallets to conduct transactions.

As part of their focus on amplifying financial literacy amongst India’s teens, the muvin app offers an exhaustive library of enriching content to demystify concepts related to managing finance. They have onboarded Monika Halan, an entrusted Author and Speaker to curate and address theme-based topics in an easy, fun, and simplified manner. From taxes to what banking truly is, muvin is covering the fundamentals and more via rich byte-sized video and short blogs that are relevant for teens.

muvin – Industry

With new players entering this space, teen-centric pocket money apps and neobanks have become a competitive digital banking landscape in a short period of time. The space has grown exponentially in the last five years. In terms of transaction value, the Indian Neobanking ecosystem is expected to clock US$47.94bn in 2022 setting the foundation for substantial growth potential in the coming years.

muvin – Founders and Team

Mukund and Vineet have known each other for over 20 years from their time at Mindtree in the early 2000’s. They share a passion for enabling access to banking services for the youth and believe that finance is a life skill that everyone should acquire by the age of 21.

Mukund Rao, Co-founder

Mukund Rao, Co-Founder, muvin

Mukund is an accomplished business leader with experience across financial services and technology. Former Capital Markets Head at Mindtree, Mukund founded derivIT in 2007 and grew it across 7 countries with a team of 400+ employees. He subsequently exited derivIT to Luxoft in 2017.

After graduating from Bangalore University, he pursued his MBA from Ecole des Ponts Business School.

Vineet Gupta, Co-founder

Vineet Gupta, Co-founder, muvin

Vineet has over 25 years of experience spread across technology and financial businesses, driving innovation and digital business models. Vineet moved on from Mindtree in 2015 after building out their Digital Business and subsequently founded a tech enabled NBFC focussed on business credit.

He graduated from IIT-Delhi and went on to pursue his MBA from IIM-Lucknow.

While both co-founders are actively engaged in all aspects of the business, Vineet looks after the Product, Operations, Finance & Technology functions at muvin, while Mukund looks after Marketing, Strategy and Business Development functions.

muvin – Startup Story

Despite India’s adoption of digital banking and contactless payments, the digital native generation still conducts over 80% of their transactions in cash. Both the co-founders, Mukund and Vineet, have teenage children who were using cash or their cards while spending money. They found the process of opening bank accounts for their kids and teaching them how to operate it within the restrictions on bank ATM/debit cards, rather cumbersome. The most common resort for parents like them was to hand over pocket money to their children. No wonder, teens often end up entering adulthood with little or no knowledge of financial management.

They saw an opportunity in enabling digital payments and offering financial products for this young consumer base- in an easy-to-understand, intuitive and friction-free manner. This is how muvin came into being.

They validated the hypothesis by empanelling Ipsos to conduct independent primary research of children and parents across 8 cities.

muvin – Name, Tagline, and Logo

muvin logo

muvin is a play on the word “moving”, where they would like their target audience to get moving and keep moving. The co-founders of muvin believe that Gen-Z is always on the go and they would like teens to get moving with their financial lives as soon as possible. The tagline, “payments for students”, addresses their audience and the core functionality of muvin, thereby avoiding any ambiguity.

muvin – Vision

muvin’s vision is to empower India’s 250 million youth with digital financial inclusion and financial literacy. muvin is unwaveringly moving forward in positioning the management of personal finance as an essential life skill and the need to inculcate it from an early age. muvin believes that India’s teens must be empowered to experience independence in their financial transactions and decisions in their day-to-day life.

muvin – Products

Bolstered by the pandemic, there has been widespread adoption of digital banking and contactless payments across the country which led to a permanent shift towards wallets, contactless cards, digital payment apps and other financial products. However, over 250 million teenagers and young adults in India are still precluded from not just financial education but banking services as well, conducting the majority of their transactions in cash. Gen Z are becoming financially aware and independent a lot earlier than a few decades ago. Pocket money apps for the teens are ideal in addressing their financial needs.

muvin has partnered with the parent community towards its larger vision of amplifying financial literacy amongst India’s digitally savvy teens. It has also understood some other critical issues that matter to parents, such as tracking of their household expenditure.

Parents now have the freedom to transfer pocket money allowance (one time /scheduled weekly / monthly) directly in their child’s wallet who can then spend the money through the app or through their own prepaid card. Parents no longer have to stress over tedious banking roadblocks. Monitoring their child’s spending habits was never this easy.

These are early days for teen-centric apps and they are in the first lap of a marathon. It is a new category and competition helps in both, creating and growing awareness about the product’s relevance and need amongst the key target user base. All the market players are addressing varied gap areas through their products, services and customer experience.

muvin is the first pocket money app to offer a RuPay co-branded keychain targeted at India’s teens. The keychain presents the most convenient and secured contactless payment mode with a simple ‘tap and pay on-the-go’ feature. The contactless keychain can be used across all RuPay NFC enabled merchants for fast processing and seamless transaction experience each time.

muvin also offers chat based banking on their website and whatsapp without the need of downloading the app. This allows customers to check their balance, view recent transactions, block their card etc.

muvin – Business and Revenue Model

There are no charges levied on customers for using the muvin services. muvin makes money from the interchange fees incurred by the merchant for card based transactions. Within the first six months of its product launch, muvin witnessed over 150,000 installs. Currently, the figures stand at approximately 50k app downloads every month.

muvin – Customer Acquisition

muvin’s journey started with the launch of its app and the ‘muvin card’ for teens in October 2021. In the same month, muvin onboarded Ace cricketer Hardik Pandya as their brand ambassador to propel its multi-channel marketing campaigns- a move which helped the brand to garner immediate attention and much-needed impetus from its target customers.

Teens need validation and approval from their parents/guardians and since its inception, muvin is consistently engaging with the parent community. Parents need to be assured on the trust front. muvin’s partnership with industry prominent players like RuPay has also helped it to strike a trust-worthy chord with the parents. Imparting financial responsibility as a trait has to be a consistent and an on-going approach. Parents are appreciating the educative, short videos and blog format content for their children which muvin offers on its digital platform. The early adopters of the muvin app have played an important role in expanding its reach amongst newer adopters.

muvin has adopted a multi-pronged approach in reaching out to potential customers. Developing a strong presence on social media has been key to building the muvin brand, as this is where Gen-Z spends a high percentage of their time. muvin is building itself out to be a young brand that teenagers can approach as an elder sibling or friend. They have also curated financial content in byte sized formats that is easy to understand and comprehend in under a minute. They have also partnered with multiple brands to serve their customers with offers and cashbacks relevant to their age group.

muvin – Customer Retention Strategy

To drive retention, muvin has partnered with multiple brands to serve their customers with offers and cashbacks relevant to their age group. They also run engaging contests and offers on the app which are refreshed on a weekly basis to keep their customers and audience engaged consistently. Through their insights led customer engagement platform and social media channels, they keep their users updated on the latest happenings on the app.

muvin – Challenges Faced

Neobanks and teen-centric pocket money apps like muvin have carved a niche category to address crucial consumer pain points which had not been addressed before. They have consistently channelised their energies to get their key consumer audience to shift from cash to digital transactions- which still continues to be a challenging affair.

Players like muvin get to interact with their customers digitally only which makes trust building especially amongst digital-savvy parents, a tedious and slower process. This requires utmost transparency and in this regard, muvin’s partnership with RuPay has helped them tremendously.

Earlier in January 2022, muvinraised USD 3 million in a pre-Series A round which was led by WaterBridge Ventures, with participation from India’s largest Venture Debt fund Alteria Capital and Krishna Bhupal, Co-Founder, Rational Pricing Technologies and board member of GVK Power & Infra.

Prior to that in April 2021, muvin raised a seed round of $1.5+ million from HNI’s Krishnakumar Natarajan (Managing Partner, Mela Ventures), Ambar Maheshwari (CEO, IndiaBulls Asset Management), Gani Subramaniam (Partner, WRVI), Shajikumar Devakar (Executive Director, IIFL Asset Management Limited), Sandeep Jethwani, and other prolific angel investors from the financial services industry.

muvin – Growth

muvin’s platform caters to India’s teens spread across leading cities in India. The brand is gearing towards engaging with one million registered users in the next 12 months. Its ambition is to enable 100 million financially literate students in the next 10 years- prepare them to confidently make the right financial choices by the age of 25 years.

With regular communication and feedback from their early adopters, muvin team plans to steadily enhance its product and introduce new features over the next two-three quarters that will substantially upgrade their users’ experience. To achieve additional scale, muvin is open to raising an additional round of funding towards the later half of this year.

FAQs

When was muvin founded?

muvin was founded in 2020.

Who is the founder of muvin?

Mukund Rao and Vineet Gupta are the founders of muvin.

Has muvin raised funding?

Yes, muvin has raised a funding of $4.5 million.

Is muvin app available on Google Play store?

Yes, muvin app is available on the Google play store and Apple app store.

Customers tend to purchase their products with various options when they buy through an e-commerce website. This could be through the various debit cards the customer has in their possession, through net-banking accounts, or through cash-on-delivery where they would pay for their products in form of cash once they receive the product you can pay for it next month when you have the money to do so.

There is a new trend that is emerging by the name of Buy Now Pay Later(BNPL). Say you find a good mobile phone worth say 10,000 rupees, but you don’t want to pay for it as it goes out of your budget for the time being (due to a cash crunch or whatever reasons it may exist). But say by opting for the BNPL alternative, the third-party BNPL company would pay the e-commerce site the 10,000 rupees and then you can pay the BNPL company the same 10,000 later.

There are various BNPL companies in India like Lazypay, ZestMoney, Simpl, MobiKwik, etc. Some companies, like Amazon in Amazon Pay Later and Ola in Ola Money Postpaid, have an intrinsic BNPL system built within them.

But then doesn’t it make you think, how do these BNPL companies make money in the first place, given the various instabilities associated with it potentially? How is it different from the conventional credit card? What is the market scenario of companies which offer the BNPL service in India? We will discuss all of these in this article.

BNPL companies make money mainly from two avenues:

Revenue from Sellers

For vendors, BNPL is an alternative payment method (others including credit & debit cards/wallets/Cash-On-Delivery) and thus, they have to incur a transaction fee like any other medium at a particular rate. However, a rate of 2-8% is higher than a normal credit-card discount rate, which is usually around 2.9% for e-commerce transactions and about 1 percent less for transactions made by credit cards in-store.

Thus, BNPL companies have to position their service offering in such a way that it convinces future customers of how enticing their service is, and this would further convince more vendors to buy into the BNPL service they are offering thus increasing the customer traffic.

Revenue from Customers

Most third-party BNPL providers do have their soft-credit checks to avoid giving money to people who have a poor record for repaying obligations, but this is not universal. Here is how BNPL provides monetizing from consumers:

1)Interest- This varies depending on the company. Some providers like Lazypay charge an interest of 10-30% on the “loan” amount, depending on the customer’s credit and duration of repayment. There are other organizations like Split in America which do not charge any interest rate as long as the installments are paid in due time.

2) Late fees- This forms a major chunk of the revenues of the BNPL organization (as high as 30%). Late fees occur when a charge is imposed on a customer for not paying the due amount on time and he thus has to pay later. Think of it like borrowing a book from a library, and then the various fines accumulated for not returning the book.

Difference between BNPL companies and Banks offering Credit cards

In India, there are mainly three differences between BNPL companies and banks that offer credit cards.

1)Eligibility Criterion- Banks have more stringent criteria to give out credit cards (such as their CIBIL credit score, whether they are earning above a certain criterion or not). BNPL companies are relatively less stringent in their criteria. This helps many consumer segments, such as self-employed people and lower-income category sections.

2) Accessibility- Unlike credit cards, where you have to fill various online forms going through multiple levels of authentication, we can get access to the BNPL option through a one-stop authentication using our UPI ID. Another fact to be noticed is there is no waiting time to avail of the BNPL option unlike say credit cards, where we have to wait 2-3 weeks after applying for one.

3)Interest Rates- BNPL companies tend to offer an interest rate of around 28-30% and as mentioned earlier, interest rates are only applied when the customer opts for a longer duration of repayment. Whereas for credit cards, this tends to be way higher than 36-42% annually. Cases of high-risk borrowers do exist in which BNPL companies offer their services at interest rates similar to credit cards.

Currently, as it stands, unlike other developed nations, BNPL in India is still in its infancy. But it has been widely speculated that it could take off in the future.

A market research firm by the name of Redseer estimates that India’s BNPL market will stand at 45-50 billion dollars by 2026 from the measly 3-3.5 billion dollars as it stands right now. The research firm also predicts that the number of BNPL users in the country could rise to 80-100 million customers by that time, from the 10-15 million users it currently has.

As per Upasana Taku, co-founder of MobiKwik, “Only 60-70 million Indians have access to credit today, which means 93% of India has no access to credit”. Thus, there are a lot of opportunities to be exploited by BNPL companies in the Indian market, where millions of people have little access to formal credit. The poor access to formal credit has further been exacerbated by the COVID-19 pandemic.

These things can be noticed in the fact that about one-fifth of the revenue of MobiKwik is due to the BNPL transactions and there has been a 45x growth in BNPL transactions for MobiKwik. Similar trends can also be noticed in other BNPL companies.

Currently, the major obstacle is, unlike those behemoth banks that offer credit cards, BNPL companies can only offer a maximum credit of 100,000 rupees (which roughly equates to 1310.17 dollars). But this can be overcome as long as the reach of BNPL companies spreads all-over India, especially in the tier-2 cities and villages of India.

Conclusion

Thus, this article documents how BNPL companies get to make their revenue in India, how they are different from banks that offer credit cards, and what is their scope in our country. In a country where a lot of people are transitioning from the lower-income group to the middle-class group, this appeals a lot to the Gen-Z and millennials of our country. The more people get access to credit, the more they spend on various goods which leads to the growth of the economy.

FAQs

Which are the BNPL apps in India?

Some of the best BNPL companies in India are:

Lazypay

ZestMoney

Simpl

MobiKwik

ePayLater

Flexmoney

Paytm Postpaid

Sezzle

What is the BNPL market in India?

According to the Q4 2021 BNPL Survey, BNPL payment in India is expected to grow by 89.5% on annually. It will reach US$ 6927 million in 2022.

Which are the E-Commerce website that allows Buy Now Pay Later option?

Top e-commerce websites that provide the payment option of Buy Now Pay Later for complete range of products are:

Company Profile is an initiative by StartupTalky to publish verified information on different startups and organizations. The content in this post has been approved by Takeoff.

Investment is all about making your future a better place. It is for the financial security of their capital that one can enjoy in the future. When a person makes an investment, it is to ensure that they get to earn higher returns. Investing in mutual funds goal is not any different.

Mutual funds are a form of investment if people are able to understand it clearly. Now, individuals are able to invest on their own in mutual funds. For non-individuals like businesses, trusts, and others, Takeoff has taken responsibility since 2020. It is India’s first online mutual fund distribution platform for non-individuals.

StartupTalky brings all about Takeoff, the platform, its Startup Story, Founders and Team, Name, Tagline and Logo, Funding and Investors, Business Model and Revenue Model, Challenges, Competitors, Awards and Achievements, and more in the article ahead!

The service that Takeoff mainly provides is mutual fund distribution. The main USP is that the entire process is online and condensed from 30 days to 1 day. Companies can now have the luxury to choose from all the schemes from all the AMCs through an easy-to-access platform. They have 24×7 access and the support team is always just a call away.

Takeoff also provides KYC services for non-individual clients like businesses, trusts, government bodies etc. Gone are the days when one has to send mountains of documents to the AMCs and has to suffer the two months of hassle while their KYC was being processed. The Takeoff team takes only minimal documents and gets the KYC processed within just 7-10 working days.

The mutual fund industry has witnessed a growth of 30.82% from 2020 to 2021 with Rs. 26.07 trillion AUM (Assets under Management) in 2020 to Rs. 34.10 trillion AUM in 2021.

Split of investor accounts:

The total number of investor accounts of Takeoff as of March 21 was 9,78,65,529, from which 7,91,859 (0.81%) is Institutional investor accounts and 9,70,73,670 (99.19%) are Retail and HNI investor accounts.

Split of industry assets:

The Total industry assets of Takeoff as of June 21 is Rs. 34,10,403 crore, from which Retail investor assets is Rs. 18,33,568 crore and Institutional investor accounts are Rs. 15,76,835 crores.

Takeoff – Founders and Team

Prasad R. Lendwe – Founder of Takeoff

Takeoff is founded by Prasad R. Lendwe, an Electrical Engineer. He is an MBA droupout from Kalina University, Mumbai. Apart from being the founder of Takeoff, he runs a Finance based YouTube channel, Convey by Finnovationz as well and has more than 1.8 M Subscribers.

The current size of the Takeoff team is 15-18 members. The work culture in Takeoff is very relaxed and informal. They believe in working hard and playing harder. It basically means, during office hours, one can find them hunched over their laptops. During lunch, however, the team can be found engaging in spirited table tennis tournaments and other games.

Takeoff – Startup Story

Before starting Takeoff, the company was focused on their Youtube channel Convey by FinnovationZ. Through this channel, they were able to spread financial awareness for the past 6 years.

In Jan 2020, they decided to take some of their own advice and tried to invest on behalf of their company. There are some surplus in the current account and the fact that they are earning 0% interest on it bothered them a lot. After using platforms like Zerodha and Groww in the past, it was wrongly assumed that the process would be just as easy.

It was only after the actual process started, they realised how difficult it is in reality. As there was no dedicated platform working towards the mutual fund investment needs of non-individualism, the idea of the formation of Takeoff first came into their mind.

Takeoff – Mission and Vision

Takeoff’s short-term vision is to spread awareness and encourage more non-individuals to begin their mutual fund investment journey. They intend on doing this by providing top-quality service and exploiting their first-mover advantage.

Their long-term vision is to emerge as a complete investment solution for non-individuals and to become a one-stop destination for any kind of investment that companies and other non-individuals want to indulge in.

The core belief is centred on the fact that non-individuals, whether its companies, trusts, proprietors, or any of the others, deserve the same facilities and the same ease that individuals do. In the past few years, thousands of platforms have cropped up for retail investors, but companies have, sadly, been left out. It is Takeoff intention to right this wrong and fixes the imbalance.

Takeoff – Name, Tagline, and Logo

Takeoff logo

Takeoff Fintech Pvt. Ltd. is the officially registered name of the company.

Takeoff is working on a distribution model. The platform is currently free to use for all of their clients and it will always be free to use. Any non-individual can register and open accounts in Takeoff. No amount is charged from the clients. The revenue comes from the AMC (Asset management company). A fixed brokerage amount is paid for each AMC.

Takeoff – Challenges Faced

The lack of awareness among the non-individuals in India that they too can invest in mutual funds on behalf of their organization is the most challenging part of Takeoff. The conversion is not easy from a lead to an active investor, as the company has to explain the whole product and the industry at the same time over a very short span of time to their clients.

Takeoff – Growth

The journey from 0 to 100 Clients

The journey was of severe ups and downs, like a roller coaster. Takeoff got their first client in December 2020 on their beta version and after some infertile months, the platform started gaining recognition, through several marketing campaigns. Currently, they have over 550 registered users and the company is experiencing slow but steady growth, they believe in value over volume.

Customer Retention

Takeoff believes that the best customer retention can be achieved only through superior customer service. Investments are a fairly complicated process, even if one makes it seems as easy as possible, clients will still have doubts. It is very important to make the clients feel as though the company is with them at each step along the way, in case they encounter any kinds of difficulties. This process has helped Takeoff in retaining its clients.

Takeoff – Advertisements and Social Media Campaigns

Takeoff has tried various platforms and a plethora of campaigns to generate leads and convert them to active investors. LinkedIn ads and their own Convey YouTube channel have been proved a constant success for the company. The company is looking forward to more events and other activities so that they can reach out to the target audience and make the platform enriched with the soul vision of the company.

Takeoff – Future Plans

The company is doing quite well. It has started to make a name for itself and is experiencing a steady inflow of clients in future. Both their client base and the AUM have started to increase.

Takeoff is India’s first online mutual fund distribution platform for non-individuals. They help non-individuals like companies, government bodies etc to invest in mutual funds.

Company Profile is an initiative by StartupTalky to publish verified information on different startups and organizations. The content in this post has been approved byYap.

Technology has transformed the way financial transactions and operations happen. Today making and accepting payments, receiving loans, everything has become simpler than ever before. All thanks to tech startups, that are coming up with amazing products that have made financial operations much easier for financial institutions, business owners, and consumers. Chennai-based ‘Yap’ is one such startup that this revolutionizing the way banks and other financial institutions offer services to their customers. Yap provides tools that let banks and financial institutions design customized and convenient solutions for their customers. Here is more about Yap.

Yap offers a payments-as-a-service infrastructure that can handle all types of retail payment assets. Yap’s Application Programming Interface (API) platform allows digital platforms, fintech companies, and offline businesses to offer personalized solutions to their end customers, by linking them with other fintech platforms and banking and non-banking financial firms.

Yap’s functional APIs, let its clients receive and transfer funds through Wallet & Cards, Cross Border Payments, Gift Cards, Fleet Spends, Just-In-Time Funding, UPI as well as other payment methods. Consumer, corporate, small business, and credit card loans are among the products it offers.

Yap’s modular platform ‘bank in a box’ enables its clients to offer products such as opening bank account, credit, online payment, toll payment, foreign exchange solutions, etc.

Many companies in Nepal, India, New Zealand, the UAE, Australia, and the Philippines are served by YAP. Around 20 Indian banks, including ICICI Bank, Yes Bank, and RBL Bank, as well as numerous consumer internet companies like Ola, Cred, Swiggy, and also large NBFCs like Muthoot, TVS Credit, Bharat pe, Razorpay, Finin, etc use YAP’s services on the lending space.

Yap – Latest News

In March 2021, Yap raised $10 Million in funding from investors like Flourish Ventures and Omidyar Network India. The fundraising round included participation from YAP’s current investors, including Beenext, 8i Ventures, and Better Capital.

“We are uniquely poised to cater to new cohorts of distributors as more firms embed financial services into their digital platforms. This investment allows us to strengthen our technology teams, build new capabilities as well as reach new markets across Asia,” Madhusudanan R, co-founder at Yap, said.

Madhusudanan R is the Chief Executive Officer & Founder at YAP. He is a fintech entrepreneur with deep-rooted experience in building and scaling Payments businesses across Asia.

Prabhu R

Prabhu R is the Co-Founder & Chief Operating Officer at YAP.

Yap – Startup Story

Madhusudanan R. and Muthukumar A and came up with the Yap idea during the office tea breaks. The founders who worked at Visa Inc in Mumbai from 2010 to 2012, often realized how big banks were lagging behind in digitizing their services. The focus of these conversations was always on how the financial industry might fix this problem. Finally, Madhusudanan and Muthukumar, came up with a solution themselves and founded Yap in 2014.

The Yap founders observed how banks work in India, through their combined expertise of over a decade working for Visa, Citibank, and Paypal. They understood that due to their aversion to developing new digital products, banks were unable to reach a whole new set of clients. Yap is a solution to these problems, Yap’s is empowering many banks, financial institutions, and businesses to offer various customized solutions to its customers.

YAP’s unique API (application programming interface) gives banks and fintech businesses the tools they need to create new payment systems. This shortens the time it takes for these businesses to acquire consumers who want simple and quick electronic payment options.

“When we started, banks in India didn’t use any APIs. In other markets, like the US, this phenomenon started ten years ago. In India, it started around 2014–15, when a few digital payment companies started to grow,” Madhusudanan, co-founder of YAP, told.

The firm claims to deal with 15 banks in India at the moment. Apart from providing an API for payment integration, including UPI payments, YAP also assists them in acquiring corporate clients, which are often digital financial institutions such as neobanks or the fintech divisions of big corporations.

“They don’t have to spend any money on this, and they can reach a lot larger audience without having to spend money on client acquisition,” Madhusudanan explained.

Yap – Mission and Vision

Yap’s mission statement says, “We are focused on user experience and customer retention. We are constantly thinking of new use cases and ways to serve our customers across all their financial needs as seamlessly woven into their daily routine life as possible.”

YAP is on a mission to transform every business into a fintech.

Yap – Name & Logo

Company Logo of Yap

Yap – Business Model and Revenue Model

Yap provides B2B tech solutions to financial institutions and businesses. The YAP platform connects companies to licensed banks, financial institutions, and financial infrastructure such as UPI/card networks through its extensive Application Programming Interface (API) libraries. Within a few weeks, a company may connect to YAP’s platform, choose goods and banking partners, and roll out financial products to its consumers or vendors. In addition, YAP oversees essential continuing activities like reconciliations and compliance monitoring. YAP now serves over 200 fintech with an API platform.

Madhusudanan R – Chief Executive Officer & Founder

Yap – Funding and Investors

Date

Round

Amount

Lead Investors

Mar 16, 2021

Series B

₹732M

Flourish Ventures, Omidyar Network India

Apr 21, 2020

Series A

$4.5M

BEENEXT

Feb 13, 2020

Seed Round

₹100M

Amrish Rau

Yap – Growth

Around 20 Indian businesses, including ICICI Bank, Yes Bank, and RBL Bank, as well as numerous prominent consumer internet companies like Ola and PaisaBazaar, use the service.

“We are uniquely poised to cater to new cohorts of distributors as more firms embed financial services into their digital platforms. This investment allows us to strengthen our technology teams, build new capabilities as well as reach new markets across Asia,” Madhusudanan said.

The 6-year-old firm offers comprehensive Application Programming Interfaces (APIs) to banks, startups, and consumer online businesses. The new funds (raised in March 2021) will be utilized to expand into foreign markets and bolster the team with new hires.

Yap’s major plans include expansion to new geographies and expanding the team. According to Madhusudanan R, co-founder of YAP, the company intends to grow to Bangladesh, Saudi Arabia, Oman, Egypt, Vietnam, and Indonesia.

India’s rapidly digitizing financial environment, according to Amol Warange, head of Omidyar Network India, would provide chances for YAP to expand.

“We think that digital enablers like YAP can catalyze financial inclusion and promote adoption of financial products among the next 500 million Indians who are projected to access the internet for the first time via their mobile phones” Warange added.

Yap – FAQs

What does Yap do?

Yap offers a payments-as-a-service infrastructure that can handle all types of retail payment assets. The company’s platform links banks, financial institutions, enterprises, payment networks, and merchants to build an interoperable payment platform that allows businesses to quickly design and carry out their own customized payment solutions.

Which country is Yap based in?

Yap is a Chennai-based, Indian fintech company.

Who founded Yap?

Yap was founded by Madhusudanan R and Prabhu R.

Which companies do Yap compete with?

Open Bank Project, Decentro, TrueLayer, Teller, Inc., Plaid, Konsentus, Figo, Quovo, and Instantor are the top ten competitors of YAP.

It might be surprising to know that India is the world’s largest growing industry of fintech companies. Fintech the short form for financial technologies and FinTech companies are those companies that sell technologies and services related to financial transactions.

With the world shrinking to one’s fingertips and everything from education to business shifting to the online mode, there is absolutely no limit to the extent to which fintech companies are growing across the world and especially in India.

Most of the firms today are investing in or are planning to invest in financial technologies heavily. It is expected that by 2023 the global fintech market will be valued at over $305 billion.

The growth of fintech industries in India has been really humble. It started to gain momentum in the country only after the government initiated liberalisation of the banking industry and the incorporation of technology.

Slowly more funds were received by the banking sector for Financial innovation. The sector started to experience the ripple effects of the financial technology revolution in the US and UK in the 2000s.

This enabled the Indian banking industry to slowly begin by offering services that are consumer-centric. In the early 21st century FinoPay Tech and EKO India were two startups that were curated in the Banking Correspondent Model (BCM). And that was just the beginning only to witness the emergence of revolutionary fintech startups like Paytm, FreeCharge, Mobikwik et cetera from 2005 onwards.

Since then there have been no turning back for the industry with a plethora of companies mushrooming across different segments like lending, investments, personal finance management et cetera.

According to the reports by Boston consulting group (BCG) and FCCI India’s fintech companies are going to be valued thrice than what they are valued today within the next five years.

It is estimated that Indian fintech companies will reach a valuation of more than $160 billion by 2025.

The establishment of fintech companies and their growth have been phenomenal in the last five years than ever before. This dynamic industry has more than 2100 companies among which 67% of them were launched in the last five years alone. The biggest achievements of the industry do not stop there.

In the first seven months of 2020, fintech companies in India received total investments worth $1.47 billion which was 60% more than what it had been in 2019. Among the trends and new answers of the industry, online brokerage was gaining more popularity and thereby encouraged investors to buy more equities, mutual funds, ETFs et cetera.

All these lead to increased activity in the industry as a whole which resulted in huge investments in the industry like never before. It saw the emergence of three new unicorns companies and five new soonicons (Companies that have a valuation of $500 million or more) just from the beginning of January 2020.

There is a total of 21 unicorns in India and out of which one-third of the companies are fintech companies, which is not a surprise anymore. Among the unicorns Paytm is the highest valued one at $16 billion.

Multifaceted Support From the Government

Among the activities of the Indian finch industries, online payments have always been at the forefront. In 2018 digital payment crossed over 24 .13 billion in 2018. These transactions are valued at over $3.5 trillion.

One of the major reason for the tremendous growth of Fintech companies in India is because of various government policies that allow and facilitate people to get on to the digital platform for storing and transacting money.

The extensive use of Aadhaar has made verification easier and policies like PMJDY (Pradhan Mantri Jan Dhan Yojana) has pulled more people onto the digital platform than ever. The introduction of the Unified Payment Interface or UPI has also introduced a large amount of unbanked population in India into the digital financial services which have further boosted the growth of fintech companies.

Apart from that demonetisation has opened vast opportunities for fintech companies for better service provisions and thereby making customers comfortable within the technologies like AI, blockchain, IOT et cetera.

Reports say that the introduction of such industry 4.0 technologies into the industry gave a jump of nearly a hundred per cent from an earlier $1.8 billion valuation in 2018.

The Future of Fintech Industry in India

The fintech industry in India will continue to conquer greater heights as it has already started to partner with various banks. Using these collaborations and the nuances of consumer behaviour, Fintech companies are all set to further use technology to capitalise on better levels of trust among people.

In 2021 and from then on it is expected that hybrid banking will become more mainstream. The performance of fintech industries in India in the first seven months itself has proved this to be true. In an environment of hybrid banking, more financial institutions that operate offline will take on to virtual banking as well.

There are also various government initiatives that aim at establishing fintech hubs along with an allocation of Rs.15 billion to boost digital payments alone. All these will further strengthen and immunise the industry in the years to come. With the incorporation of newer technologies into the industry, it is expected that by 2025 there will be more than 30 billion connected devices ranging from thermostats to refrigerators to lightbulbs.

The breakthrough advent of cryptocurrency and blockchain technology is also expected to be a game-changer in the industry, especially regarding money transactions, consumer payments et cetera. However, it will be completely dependent on the stand of the Indian government.

FAQ

How many Fintech companies are there in India?

At present there are more than 2,000 fintech companies in India.

When did the FinTech sector rise in India?

In 2015, the Indian fintech sector saw the emergence of numerous fintech startups, incubators, and investments from public and private investors.

How big is the fintech market in India?

The Indian Fintech market is currently valued at $31 billion and is expected to grow to $84 billion by 2025, at a CAGR of 22%.

Money related organizations, monetary methodology, and budgetary administrations have radically advanced and improved in the last couple of decades. With the development of the Fintech industry in India, the whole business has experienced a huge change in the manner in which the money related methods are completed and budgetary establishments are performed.

The coordinated efforts between account and innovation has prompted an extreme change in banking, venture, exchanging, and digital money. And that’s just the tip of the iceberg. This development has prompted the ubiquity of the term “Fintech“, a short structure for the expression of Financial Technology. This post reveals insight into Fintech and why has it turned fierce in the modern world.

Fintech is significantly more than only a reference to money related innovation. It is frequently alluded to as the inventive innovation used to improve customary money related strategies and create powerful answers for budgetary administrations, those which are at standard with the most recent mechanical patterns. Banking programming and portable financial applications are great instances of improvement in monetary innovation.

Progressively, the huge fintech industry comprises of new companies and lofty monetary organizations endeavoring to improve the budgetary administrations given by money related foundations around the globe. The organizations have endeavored to utilize continually advancing innovation and create present-day techniques for taking care of money.

A large number of us may not understand, yet innovation has constantly assumed a critical job in the money related division. In any case, the most recent 65 years have played a huge role in the development of the fintech industry and the creation of a few fintech arrangements.

The 1950s saw the dispatch of credit cards and 10 years later, ATMs changed the manner in which cash was withdrawn from banks. The proliferation of the internet during the 1990s propelled the fintech business to a new level; electronic installment framework, web-based business models, web-based shopping, portable banking, and digitization of banks have brought about a significant revolution.

What Is Fintech Industry | History of Fintech

The world’s first ATM was propelled in 1967 by Barclays and the IPO in 1971, the principal online installment stage Paypal was established in 1998, the primary digital money Bitcoin was propelled in 2009, Google propelled Google Wallet in 2011 and, Fintech startups have been all over the place since then. Earth-shattering advancements of innovation are paving the way for fintech upheaval.

Money related innovation is said to be a problematic power that is relied upon to reshape the budgetary division, plans of action, and banking structures. New money related innovation simply keeps on progressing, has pulled in speculators from different nations, and has cleared the way for the development of markets and the fintech industry itself.

Retailer banking and installments, protection, financier administrations, business banking, venture, and riches are affected the most by the development of fintech.

A NASSCOM report says that the fintech programming and administration advertising in India was around $8 billion in 2016; it was expected to develop 1.7 times by the end of 2020. The report includes that the exchange an incentive for the Indian fintech division was around $33 billion in 2016 and was scheduled to reach $73 billion in 2021 at a five-year compound yearly development rate (CAGR) of 22%.

The Indian FinTech scene is divided as follows: 34% in installment handling, trailed by 32% in banking, and 12% in the exchanging, open and private markets. Visakhapatnam is being created as FinTech valley and the nearby administration of Andhra Pradesh opened Fintech Valley to advance the interests in this area.

Fintech Industry Growth

In 2018, more than 12,000 new businesses grew in the Fintech space over the world with a monstrous speculation of $19 billion. Fintech includes innovative organizations that are going up against each other and working in unison with existing money related foundations. These organizations likewise work together with colleges and research foundations, government affiliations, and industry bodies.

India now has a system in place that gives new companies a chance to exponentially develop into enormous organizations. Directly from digging into a scope of unexplored portions to outside business sectors, new Fintech businesses are conveying advancement that was deemed hard to accomplish.

Growth Of Fintech Services

The Indian Fintech programming business sector is expected to touch $2.4 billion by the end of 2020 from the current $1.2 billion in FY 2019.

Over the last couple of years, the Indian economy, which is altogether money-driven, has exploited the Fintech opportunity. With a scope of choices that includes digital wallets, loaning, and protection, the assortment of administrations gave an enormous impact to change the manner of money-related activities.

A number of encouraging reasons are propelling the comprehensive growth of Fintech in India. Some of them are:

Easy Payments

Installments have seen a noteworthy transformation in the recent years, particularly due to the disturbance of internet business, versatile trade, and online installments. Budgetary consideration is substantially more than just installments and exchanges and installments are seen as the door for monetary incorporation. Shoppers and vendors will keep on grasping digitized installments while UPI will continue to have its firm ground for both P2P and P2M exchanges.

Partnership Between FinTech’s And Corporates

The Fintech Times says 2020 will be the time of brilliant coordinated efforts between Fintech trend-setters and corporates, where corporate organizations would ideally put resources into Fintech instead of acquiring arrangements. Likewise, banks will be collaborating with Fintech to sort out inconsistencies and offer benefits via administration, smooth client experience, and a progression in cutting-edge highlights to ease tasks.

There’s a rising change being experienced by Investment Advisory organizations with the improvement of electronic riches counsels, also known as “Robo-guides.” And by “Robo,” we mean computerized board-stages as real robots.