In the last 7 to 8 years, the fintech industry has experienced immense growth all over. A countless number of fintech startups have begun their journey in the last few years and have already put their name on the list of top fintech companies.

As of 2020, the global market size value of the fintech industry is $110.57 billion. Fintech or financial technology is a form of technology that is challenging the traditional method of providing financial services to people.

Now in the fintech industry, there is a thing called credit score, and everyone is dependent on them, including consumers, business ventures, and purchasers. In this article, we will learn how credit scores play an important role in the fintech industry. So without any further, let’s get into the business.

“The major winners will be financial services companies that embrace technology.” – Alexander Peh

In simple terms, a credit score is a number that decides your creditworthiness. The number is between 300 to 850. The more your number is the more is your creditworthiness. This score actually depicts your chances to pay off the money that you owe to the lender.

This helps any kind of financial institution to understand if you are dependable enough to pay the loan if they lend you. If your credit score is high, then the chance of getting a loan and credit increases for you, if you want to buy something. If the score is lower then, the chances of getting a loan decrease.

There are different credit bureaus that check your credit scores and make a report on it and send it to you. The reports are based on many factors. There are three top and popular bureaus that count the credit scores of people.

There are there main international credit score bureaus that assess people’s credit score and they are:

Equifax

Experian

Transunion

Fintech Industry in India

The fintech industry in India has taken a huge turn in a few years, it has changed the way we used to enjoy financial services in the past. Currently, it wouldn’t be wrong to say that India is the hotspot for fintech startups.

As of 2021, the market size is $31 billion and it is said to be the third-largest in the world. By the next five years, we are going to see 22% growth annually. The country has 1860 startups in the fintech industry, out of those 17 have already got the Unicorn status. In the last two years, massive numbers of people have adapted to digital payments systems for any kind of transaction, and it’s only going to increase.

Role of Credit Scores in Fintech

The first thing the financial institution will do after getting your, request for the loan, is to check your credit history. If your credit score is good enough, then it will provide you with the loan and apart from that, loads of rewards and benefits. It is very good support for the fintech companies who are lending money to the borrowers.

How Credit Score is Calculated?

The way of calculating credit scores varies from bureaus to bureaus. They have their own model that they use to get the result. There are five things that are taken into consideration during the evaluation process and they are:

The credit scores help you in two ways and they are:

Your credit score lets you know where you are lacking, the complete report gives you an idea of how you can improve in that area to increase your score. The report consists of all the transactions that you have made.

Through a good credit score, you are eligible to get attractive offers on loans and credit cards. A credit score of 750 and above is the best to get good offers.

How to Improve Credit Score?

Pay your debt before the due date every month.

Don’t ignore your overdue bills pay them as soon as possible.

Keep in mind the credit card you use and its type.

Don’t spend too much on your credit card. Be aware of your spending and try to cut the unwanted ones.

Benefits of High Credit Score

A high Credit score has several advantages, some of which are listed below.

When your credit score is higher, you are eligible in front of banks to get loans and credit cards at considerably lower interest rates. Plus there is a chance of a discount on the processing fee of a high loan amount.

Those who have higher credit scores have a lower risk rate of not paying their debts. It basically means the chances of your loans getting approved are higher.

You are eligible for a credit card that offers good rewards and other offers like cashback as well.

Your credit limit increases, if you’re worthy, then the creditors know that you will pay your debt on time, this increases their trust which in return increases the credit limit.

Attractive Car insurance and home insurance rates are offered to those with good credit scores.’

Less number of documents is needed by lenders from you.

Guarantors are not needed when you are taking a loan if you have a good credit score.

Getting loans or credits can be quite a hassle but if you have a good credit score, then lenders won’t hesitate to lend you the money. Fintechs take the help of credit scores and realize who to lend money and who do not. The credit scores assure the fintech, about your credit risk and the money that they are about to lend,

FAQ

Why do financial institutions look at your credit scores?

Financial institutions take the help of credit scores to determine what kind of borrower you will be and if you are creditworthy or not.

Who uses credit scores?

Credit scores are used by financial service givers, especially lenders.

What is a good credit score?

A credit score of 700 or above is a good one as achieving the perfect 850 is quite hard.

What are the factors that affect credit score?

Payment history, Amount owed, Credit history length, Credit mix, and New credit are the factors that affect credit score.

Company Profile is an initiative by StartupTalky to publish verified information on different startups and organizations. The content in this post has been approved by Takeoff.

Investment is all about making your future a better place. It is for the financial security of their capital that one can enjoy in the future. When a person makes an investment, it is to ensure that they get to earn higher returns. Investing in mutual funds goal is not any different.

Mutual funds are a form of investment if people are able to understand it clearly. Now, individuals are able to invest on their own in mutual funds. For non-individuals like businesses, trusts, and others, Takeoff has taken responsibility since 2020. It is India’s first online mutual fund distribution platform for non-individuals.

StartupTalky brings all about Takeoff, the platform, its Startup Story, Founders and Team, Name, Tagline and Logo, Funding and Investors, Business Model and Revenue Model, Challenges, Competitors, Awards and Achievements, and more in the article ahead!

The service that Takeoff mainly provides is mutual fund distribution. The main USP is that the entire process is online and condensed from 30 days to 1 day. Companies can now have the luxury to choose from all the schemes from all the AMCs through an easy-to-access platform. They have 24×7 access and the support team is always just a call away.

Takeoff also provides KYC services for non-individual clients like businesses, trusts, government bodies etc. Gone are the days when one has to send mountains of documents to the AMCs and has to suffer the two months of hassle while their KYC was being processed. The Takeoff team takes only minimal documents and gets the KYC processed within just 7-10 working days.

The mutual fund industry has witnessed a growth of 30.82% from 2020 to 2021 with Rs. 26.07 trillion AUM (Assets under Management) in 2020 to Rs. 34.10 trillion AUM in 2021.

Split of investor accounts:

The total number of investor accounts of Takeoff as of March 21 was 9,78,65,529, from which 7,91,859 (0.81%) is Institutional investor accounts and 9,70,73,670 (99.19%) are Retail and HNI investor accounts.

Split of industry assets:

The Total industry assets of Takeoff as of June 21 is Rs. 34,10,403 crore, from which Retail investor assets is Rs. 18,33,568 crore and Institutional investor accounts are Rs. 15,76,835 crores.

Takeoff – Founders and Team

Prasad R. Lendwe – Founder of Takeoff

Takeoff is founded by Prasad R. Lendwe, an Electrical Engineer. He is an MBA droupout from Kalina University, Mumbai. Apart from being the founder of Takeoff, he runs a Finance based YouTube channel, Convey by Finnovationz as well and has more than 1.8 M Subscribers.

The current size of the Takeoff team is 15-18 members. The work culture in Takeoff is very relaxed and informal. They believe in working hard and playing harder. It basically means, during office hours, one can find them hunched over their laptops. During lunch, however, the team can be found engaging in spirited table tennis tournaments and other games.

Takeoff – Startup Story

Before starting Takeoff, the company was focused on their Youtube channel Convey by FinnovationZ. Through this channel, they were able to spread financial awareness for the past 6 years.

In Jan 2020, they decided to take some of their own advice and tried to invest on behalf of their company. There are some surplus in the current account and the fact that they are earning 0% interest on it bothered them a lot. After using platforms like Zerodha and Groww in the past, it was wrongly assumed that the process would be just as easy.

It was only after the actual process started, they realised how difficult it is in reality. As there was no dedicated platform working towards the mutual fund investment needs of non-individualism, the idea of the formation of Takeoff first came into their mind.

Takeoff – Mission and Vision

Takeoff’s short-term vision is to spread awareness and encourage more non-individuals to begin their mutual fund investment journey. They intend on doing this by providing top-quality service and exploiting their first-mover advantage.

Their long-term vision is to emerge as a complete investment solution for non-individuals and to become a one-stop destination for any kind of investment that companies and other non-individuals want to indulge in.

The core belief is centred on the fact that non-individuals, whether its companies, trusts, proprietors, or any of the others, deserve the same facilities and the same ease that individuals do. In the past few years, thousands of platforms have cropped up for retail investors, but companies have, sadly, been left out. It is Takeoff intention to right this wrong and fixes the imbalance.

Takeoff – Name, Tagline, and Logo

Takeoff logo

Takeoff Fintech Pvt. Ltd. is the officially registered name of the company.

Takeoff is working on a distribution model. The platform is currently free to use for all of their clients and it will always be free to use. Any non-individual can register and open accounts in Takeoff. No amount is charged from the clients. The revenue comes from the AMC (Asset management company). A fixed brokerage amount is paid for each AMC.

Takeoff – Challenges Faced

The lack of awareness among the non-individuals in India that they too can invest in mutual funds on behalf of their organization is the most challenging part of Takeoff. The conversion is not easy from a lead to an active investor, as the company has to explain the whole product and the industry at the same time over a very short span of time to their clients.

Takeoff – Growth

The journey from 0 to 100 Clients

The journey was of severe ups and downs, like a roller coaster. Takeoff got their first client in December 2020 on their beta version and after some infertile months, the platform started gaining recognition, through several marketing campaigns. Currently, they have over 550 registered users and the company is experiencing slow but steady growth, they believe in value over volume.

Customer Retention

Takeoff believes that the best customer retention can be achieved only through superior customer service. Investments are a fairly complicated process, even if one makes it seems as easy as possible, clients will still have doubts. It is very important to make the clients feel as though the company is with them at each step along the way, in case they encounter any kinds of difficulties. This process has helped Takeoff in retaining its clients.

Takeoff – Advertisements and Social Media Campaigns

Takeoff has tried various platforms and a plethora of campaigns to generate leads and convert them to active investors. LinkedIn ads and their own Convey YouTube channel have been proved a constant success for the company. The company is looking forward to more events and other activities so that they can reach out to the target audience and make the platform enriched with the soul vision of the company.

Takeoff – Future Plans

The company is doing quite well. It has started to make a name for itself and is experiencing a steady inflow of clients in future. Both their client base and the AUM have started to increase.

Takeoff is India’s first online mutual fund distribution platform for non-individuals. They help non-individuals like companies, government bodies etc to invest in mutual funds.

In the financial services sector, insurance is always an area that seems like quicksand for the people who lack proper knowledge. Besides, the insurance sector is one that has always been devoid of proper, credible advisors who would steer their clients to fortify their future. This is where the digital insurance advisory platforms are proven to be a huge boon. Ditto is one of the latest online insurance advisory platforms that was founded by the co-founders of Finshots in February 2021.

Ditto Insurance has been headquartered in Bengaluru and has already raised Rs 4 crore from Zerodha in an initial funding round, the latter also picked up a majority stake in it. With Ditto, the founders hope to reiterate the success they gained with Finshots, which was launched in 2019 and already boasts of a subscription of over 5 lakh readers.

So, let’s check out Ditto, its Founders and Team, Funding and Investors, Challenges, Future Plans, Products and Services, Name, Tagline and Logo, Startup Story, and more.

Finshots (The parent company of Ditto Insurance) is a 3-minute daily newsletter giving readers insights about all things economics and finance. Their vision is to create financial literacy among Indians by simplifying finance and financial products.

The core belief of Finshots is that financial literacy is like basic arithmetic every person should know. Everyone should understand what’s happening with the economy, or what’s going on behind a financial scam – but the news is often full of technical jargon, making it obscure to the layperson. Hence, their main aim is to simplify finance for everyone and give trustworthy information that people can rely on.

Ditto – Industry

Finshots caters to the Fintech industry. They don’t have a target market for Finshots. They want to build an inclusive community of people willing to learn and understand financial concepts. On the other hand, for Ditto, their target market is the working population looking for insurance for themselves and their loved ones.

Finshots currently has a user base of over 700K readers, while Ditto has helped more than 10,000+ people with their insurance queries.

The fintech industry has massive scope, since investments, as well as insurance penetration, is severely lacking in the country. Only close to 2-3% of Indians have invested in equities, and insurance penetration is a meagre 3%. So the scope for growth in the industry is immense.

Ditto – Starting Up

After completing their MBA course, Bhanu Gurram, Shrehith Karkera and Pawan Kumar Rai founded Finception in 2018. Lokesh Gurram, an IIT Delhi graduate, worked for Samsung in South Korea for two years before joining the venture.

They saw that financial news from major media houses was loaded with industry-specific terminology, as though it wasn’t intended for the masses. And so, Finception delivered explanatory long-form stories for a year. The objective was clear: To simplify financial news for the masses.

In 2019, a separate brand called Finshots came about when the team realized that audiences suffered from information overload.

Finshots delivers only one news a day. Readers spend just three minutes each day but in a month, they would have read about 28 topics.

Finshots doesn’t spend a dime on advertising. Finshots’s subscriber base has grown to 500,000 just by the word of mouth. While Finshots educates people about the financial markets, readers are still left asking which financial product is best-suited to their needs.

Then they launched Ditto, the latest product under the Finshots brand aimed at simplifying insurance policies for people. This is one of the many ways Finshots intends to simplify financial products and financial planning for the masses.

Finshots is a financial newsletter that one can read in no longer than 3 minutes. They also have a podcast that covers the same content as their newsletter. Their product tries to resolve the problem of lack of financial literacy among people by offering information in plain, simple, lucid English, which is their USP.

They started Finshots back in 2019 when they realised people wanted finance content simplified and this was a market gap they wanted to fill. They later launched Ditto Insurance, their latest venture which provides insurance advice. Ditto aims to help millennials make better financial decisions and they’ve started with insurance. They want to make a dent in the insurance industry by educating the masses so that people can compare policies, narrow down their choices per their requirements, avoid pitfalls and buy the policy best suited for them.

Ditto – Founders and Team

Ditto Founders

At IIMA, Bhanu, Shrehith Karkera and Pawan Kumar Rai were batchmates. At the time, Rai was working on a way to simplify stock markets for millennials. They say that millennials must be helped traversing these jargon minefields.

The founders were also a part of IIM Ahmedabad’s IIMAvericks program which gave them a monthly stipend. Nevertheless, Karkera taught part-time classes at coaching institutes like T.I.M.E. and Career Launcher, so Finshots could hire more interns and grow.

Shrehith handles most of Finshots content, while Bhanu & Pawan handle marketing and sales. Lokesh manages product and tech.

Finshots have over 80 employees at present, working from home. But they try to create a work environment that makes everyone feel like they’re having fun in what they’re doing, rather than being crippled with piles of work. They also organise monthly activities to keep up team spirit.

When it comes to hiring, they look more at the enthusiasm and work ethics an incoming employee brings to the team, rather than their background and resume.

Ditto – Name, Tagline, and Logo

Ditto Logo

The idea of Finshots is ‘financial shots’ – think of it like coffee shots you take in the morning. That’s exactly how they want people to consume financial information, one shot at a time.

“Our philosophy behind naming our insurance advisory as ‘Ditto’ is that we want to tell people what kind of policy we would buy if we were in their shoes. We want to tell them exactly what we would do, and they can then make a decision based on that. “

Ditto – Business Model and Revenue model

Finshots is completely free and they don’t intend to make any revenue off of it.

“That’s part of the mission behind Finshots – we want to democratise financial information, offering our content for free is part of it. “

Ditto, on the other hand, earns money through policy sales. They function as a distributor and help people with purchasing policies.

Ditto – Challenges Faced

The biggest challenge faced by Ditto was the fact that insurance is a push product. The industry practices include mis-selling policies and spam calling. The founders believe that a product like insurance has the power to make or break the financial strength of households and that’s why their approach towards insurance is to research, give the right advice, and simultaneously ensure peace of mind to families.

On the other hand, the biggest challenge for Finshots was expanding the reach of the newsletter. It’s definitely not easy to make lakhs of people subscribe to and read your content on a regular basis. And there aren’t any viral marketing shortcuts here. So they mostly relied on good-old word of mouth marketing, social media and college partnerships. They sent college newsletters to students and got their first 1000 readers.

The biggest digital payment brand, dominating the whole digital transactions companies around the globe, is Visa. Visa Inc. is widely famous across the globe and serves over 200 countries and numerous territories. Visa facilitates dozens of services at a broad level to the individual consumers, financial institutions, governments, and merchants. It offers authorization, settlements, and clearing services in the smoothest manner.

Visa Inc. does not issue debit or credit cards although it does authorize the service of debit, credit, and prepaid cards to the enterprises as well as consumers. Visa gains its most profitable deals by selling services to various financial businesses and merchants, acting as the middleman. Visa’s biggest business strategy comes from expanding its presence to various digital payments, E-Commerce, and others. The biggest rival to Visa is Mastercard Inc. and PayPal Holdings Inc. in the market. In this article, we will discuss the business model of Visa and how it makes money! Let’s get started.

Visa Inc. is a prominent global digital payment company that acts as the middleman in facilitating consumers, financial institutions, government, and other businesses. Visa’s services are available in more than 200 countries and territories across the globe.

The American multinational corporation, Visa works as a financial services provider headquartered in Foster City, California, United States. Visa was founded by Dee Hock in 1958 as the BankAmericard.

Visa is known as the second-largest debit and credit card payment corporation, after China’s UnionPay. This data is based on the number of card payments made and the number of card issues of the company, annually. Apart from this, Visa is the leading banking card company in the whole world, dominating around 50% market share of the entire card payments.

Where does Visa Operate?

Visa is a global payment company that serves more than 200 countries and territories, worldwide. It’s four secured data centers operated in Highlands Ranch, Colorado; Singapore; Ashburn, Virginia, and London, England.

Key Products and Services of Visa

Visa Inc. offers tons of services to its consumers such as clearing, authorization, and settlement services. Its major services and products are:

Services: Clearing, Authorization, and Settlement services. Moreover, mobile payments, top-up services, and money transfers.

Products: Visa provides its allotted credit cards, commercial cards, debit cards, prepaid cards, and other mobile and money transaction-based products.

Visa majorly targets the people with a good income to spend and those who need credit points. The company targets its consumers through various channels such as banks or other financial institutions.

The digital payment company believes in providing consumers with the utmost convenience of its stakeholders.

Business Model of Visa

Visa logo

Visa functions on a pretty different business model as compared to the conventional models. Who doesn’t have a Visa card nowadays? But it’s pretty amazing how its business model functions. The digital payment company, Visa is a publicly-traded company that comes in the listing of the New York Stock Exchange.

Visa follows the Multiple sided platform- business model. It functions by spreading its card services everywhere. And the maximum the customer through a Visa card makes will be accepted by the merchants and vice versa.

Visa mainly focuses its marketing campaigns on the customers holding Visa’s card and are the subsidy side of the company. Visa provides the best facilities for payment to consumers, businesses, and government organizations. In a further manner, Visa uses a proprietary transaction processing network of technology.

What is unique about the Business Model of Visa?

Visa’s mode of generating revenue is entirely different from any other organization. It functions with an open-loop system and follows a transaction-centric business model.

Visa’s business model is based on connecting the consumers to the business owners as the middleman. Visa’s revenue generation isn’t based on the money made by the discount offers of merchants or consumer’s membership fees for issuing the card.

Visa functions as a transaction-centric business model where it earns its revenue through the payments as well as transaction volume done from its personalized cards.

Visa charges little transaction fees from the merchants. Let’s suppose there is a certain amount the consumer transacted to the merchants. So around 2-4% of the total will be merchant fees. That 2-4% will be split between the consumers and the organization, based on the interchange fees. There is always a high risk of default payment by the consumer but the person with a Visa card keeps more generated money from the merchants.

Visa generates its revenue from transactional processing, payment volumes, and value-added assistance including dispute management, issue processing, value-added information services, loyalty services, and many more.

The revenue is distributed in four streams as Service revenue, International transitional revenues, data processing revenue, and other sources of generating more revenue.

Conclusion

Visa is an excellent digital payment company when it comes to serving customers promptly. Although it does make it the second-largest digital payment company after UnionPay of China. But apart from that, Visa is the first choice of everyone across the globe. It offers tons of amazing services to merchants, financial institutions, and others. Through this article, we got the knowledge on how the company makes its money as well as its business model. Stay tuned for more updates!

This article is contributed by Sanjay Sharma, MD, Aye Finance.

Getting a loan is something that bothers everyone with all the formalities and paperwork. But 2021 being the FY that has seen a financial crisis for various sectors, has been some or the other way boosted by various fintech companies that have helped them to manage and survive their businesses. Amongst various fintech companies, there are a few companies that made lending easy and hassle-free.

With $1 billion of loans disbursed to around 1.3 lakh MSMEs across India since its inception, Lendingkart has been growing rapidly in MSME financing and one of the major reasons for this is its credit intelligence platform. Lendingkart’s proprietary underwriting model has been instrumental in providing credit sanctioned loans to 250k loans over the past 6 years but it is important to understand how it is being utilized by the firm itself.

Aye Finance

Aye Finance – Lending Institution

Aye Finance founded by Sanjay Sharma MD is a commercial institution built around the mission to solve these challenges of funding MSMEs and enabling their inclusion into the mainstream of the economy. Aye Finance is equity-funded by three reputed Venture Capital Funds – Accion International, SAIF Partners, and LGT Impact ventures. It also has over a dozen providers who extend their debt funds for its MSME finance business. Aye offers Rs 1-3 lakhs line of credit for working capital to microenterprise owners who typically have sales of INR25-50 lakhs annually.

Aye has successfully enabled the inclusion of 3 lakh micro enterprises having disbursed over Rs 4,000 crore to them.

Ziploan is a tech-enabled RBI registered NBFC that provides loans to small businesses. The platform addresses the need of the SME sector, which has been ignored by financial institutions. The platform generates a unique ZipScore for each loan applicant by developing an automated underwriting algorithm.

Satya MicroCapital

Satya MicroCapital – Lending Company

Satya MicroCapital Limited is an NBFC-MFI that serves low-income entrepreneurs in rural and urban areas. The company provides prompt, convenient, and affordable collateral-free credit to unbanked and underserved people through a strong credit assessment and centralized approval system. Satya MicroCapital’s firm belief in modern technology and its potential to increase efficiency, reduce risks, and enhance the overall customer experience is apparent in its adoption of cutting-edge innovations to power its operations.

NeoGrowth is an SME lending platform, registered with the Reserve Bank of India (RBI). The NBFC’s approach includes innovative technology and a digital payment ecosystem along with flexible repayment options. NeoGrowth aims to bridge the credit gap for MSMEs by offering customized products to address customers’ multiple business needs.

Save Solutions Pvt. Ltd.

Save Solutions – Lending Company

Save Solutions Pvt. Ltd. is one of the country’s largest Business Correspondent Networks. The Bihar-based company is focusing on giving access to Financial Products via kiosk banking and customer service points (CSPs) to rural and semi-urban unbanked citizens. Expanding rapidly, the SSPL group has roots across India in 488 districts, with over 12,000 kiosks in rural areas. The company employs over 25,000 people across these locations at its Customer Service Points (CSPs) and Kiosks. All the employees are provided training in computer and cash management systems to improve client enrolment and service delivery, thereby helping improve Save Solutions’ overall service performance.

InCred is a new-age financial services group founded with the vision of providing credit to Incredible India and thus, furthering financial inclusion in the country. The company endeavors to disrupt the status quo in traditional lending that seems to exclude those most in need of credit, due to outdated, rigid, and often inefficient processes. The company has designed its products with a razor-sharp focus on serving the unique needs of these under-served segments of customers and leverages technology and data science to make lending quick, simple, and hassle-free. It aspires to be the key partner for all financial requirements of an Indian family.

Founded in the year 2016 by Bhupinder Singh, former head of Investment Banking Deutsche Bank Asia-Pacific, the company launched market operations in January 2017. InCred offers a broad portfolio of products that cut across key categories such as Personal Loans, SME Loans & Education Loans.

Bajaj Finserv Limited is an Indian financial services firm that specializes in lending, capital management, financial advisory, and coverage. Business loans of up to Rs 45 lakh are available from Bajaj Finserv at low-interest rates.

Like all and every firm, ‘Marketing’ is one of the most essential activities of the firm that engages in promotional and advertising activities such as marketing and advertising for goods or services, particularly in the modern environment where innovation strategy has accelerated exponential rate and implementation of these strategies can be a make-or-break determinant for businesses.

Middle-class and low-income families are mostly the target clients of this team. They have created commercials and marketing techniques that are suited exclusively for them. Offering them high-interest rates on investments, short-term loans, insurance plans, and other financial products. By making such great deals available, the name and fame of the company start spreading not only through marketing but also through word of mouth.

A marketing strategy is a well-thought-out comprehensive business plan. This plan assists in targeting consumers and eventually converting them into potential customers of offerings or services. Let us take a closer look into the particulars of such plans or strategies. In this article, we are going to give you a good overview of the marketing strategy of Bajaj Finserv.

Bajaj Finserv is more focused on keeping current clients than gaining new ones. They believe that keeping their existing customers satisfied will make their clients recommend them to others thus helping their firm to grow and expand.

‘More clients cannot equal more items per client, but the more delighted their customers are, the more inclined they are to collaborate with them on their next big project’. They are more inclined to refer Bajaj Finserv to their relatives and friends. The more people who suggest them, the less they have to worry about acquiring new consumers. They can focus more on existing clients if they do not have to worry about acquiring new customers.

Any buyer would check the company’s ratings before acquiring something. Satisfied existing customers will help in building a good brand image in the market thus helping them in competing against rivals.

Content marketing is a sort of business that entails the production and sharing of internet content that does not directly promote products and services but is meant to arouse interest in the product or offerings.

Bajaj Finserv has been writing SEO-optimized blogs on a variety of themes to boost its brand’s visibility across all results. This will help them to be more visible to clients and build their belief in them.

From the first stage, which is the consciousness phase, in which the consumer understands the item, to the last step, which is the action stage, in which the client acquires the product, Bajaj Finserv has meticulously prepared its content marketing strategy.

Their very well-maintained attention stage for the simple purchasing of their clients is one of the unique aspects of this firm’s marketing strategy.

It is a well-known brand in its field, along with some of its rivals. It caters to a specific demographic and is one of the most effective marketing methods available. So, let us dig deeper into the rivals of this well-reputed company.

Bajaj Finserv Forms Alliances with the World’s Best Companies

Bajaj Finserv Alliances and Partnership

This company’s predilection for the best in the world stems from our fixation with achieving our Big Goal. When their consumers purchase a product or service from them, they think they are putting their trust in their firm. Trust is a sensitive subject in and of itself. It necessitates both skills and experience. Bajaj Finserv is executing zero-tolerance policies to compromise when they work with SalesForce for their internet skills, Microsoft for our software, TCS for process analysis, and CRISIL for audits.

They are not a partner who can be both hot and frigid at the same time. They are just as committed to their business associates as they are to each of you as clients. Even with their relationships, they have set new standards in terms of innovation by deploying their structures and procedures to build brave new realities.

Bajaj Finserv’s Deep Technological Investment

Bajaj Finserv uses technology to give you a better user experience, allowing you to make decisions even when you are being served. Since the result of technology is not the technology itself, but rather the inventiveness with which it is deployed.

This team has continued to expand our technological spending over time by putting our money where our mouth is. OPEX, not CAPEX, accounts for a significant chunk of technological expenditure. It provides us with the benefit of being unaffected by diminishing returns. It provides you with unrivalled flexibility in working with us for all of your financial needs.

The more satisfied you are, the more likely you are to pick us the next time you require financial assistance.

Bajaj Finserv is a pretty reputed company among both its rivals and its clients. The fact that they concentrate more on their present consumers to meet them and provide them with more facilities is a marketing advantage since every time a new consumer sees their ad and goes to obtain a review, there is a high probability that he will turn into a buying

This article will show you how Bajaj Finserv implemented its digital marketing strategy, and if you want to master comparable strategies and expertise, start learning online marketing right now.

Bajaj Finserv considered an essential factor while devising their approach for achieving the Big Goal is what are the specializations and strengths from the past, they might want to bring forward. One notion rang true across all of our alternatives, reflecting in all of their results throughout their existence – longevity. It is the imprint that their past has left behind. This is the result of the team’s parent company, the Bajaj Group, working for almost half a century. Distributed through each business invested into by the Group. This important filter must be applied to everything they do.

FAQs

Who are the target audience of Bajaj Finserv?

Bajaj Finserv’s target audience consists primarily of middle-class and low-income group of families.

What does Bajaj Finserv do?

Bajaj Finserv is an Indian financial services company. It is involved in lending, asset management, wealth management and insurance.

Who is MD of Bajaj Finserv?

Sanjiv Bajaj is the MD and Chairman of Bajaj Finserv.

Who are the top competitors of Bajaj Finserv?

Some of the Bajaj Finserv’s competitors in India are:

The intrinsic need of every human is to live a comfortable life. Leading a comfortable life is not easy if you don’t have some resources. It is important to note here that peace and comfort are not googleable. You need to do something to make your life a smooth sail. So that you have enough resources.

Speaking of resources, one of the most important resources is money. It is a battery for storing value. The more you have it, the more free you will(feel) be. And mark my words, “freedom” is the ultimate flex.

So to amass more of it, we people do many sorts of things. Some do business and others work for other businesses. If you look into the recent past you will notice how ‘investing’ as a domain has risen many folds. How people all over the internet are making portfolios. How stock market participants are rising. How everyone is hoping to get that IPO allotment. All these are examples of people trying to create some more income. Income leads to freedom. Not to mention how the “financial freedom” phrase gained momentum recently.

Getting into stock markets has been a fad for more than a year now. Chasing IPOs is another fad for some young investors. There is an intrinsic trait of IPOs that interests everyone. The hype of listing gains. Quick profits and the first come badge. A recent hot chase was the huge Paytm IPO. Which didn’t go well. This is the article about that failure and the behemoth PayTM. Read on to see through.

Have you heard this term before? Fin-tech is a word derived from amalgamation of finance and technology. This could be named as the word of the decade. You won’t ask the reason for this, because you probably know it already.

As the technology sector is rising, lines between companies are blurring. So much so that I would say that every company is a technological company now. With gaps blurring between sectors, the financial sector is the next most diffusing sector. It is hugely automated and also supported by countries’ governments. For example, in India the government is promoting digital payments after the demonetisation. This is a good boost for online digital payments companies, UPI (unified payments methods) and the like.

A Brief about Paytm

Paytm is a name that needs no introduction. The name is just enough. It is a leading digital payments company that is digitalizing India. Not to mention the immense support that the company is being provided by the government. Not only this, Paytm started the digital revolution in India.

From that, they became the leading payments app in the second most populous country in the world. Today, to the north of the 20 Million mark, merchants & businesses are powered by Paytm to Accept Payments digitally. This is because more than 300 million Indians use Paytm to pay at daily stores. That’s not all, the Paytm app is used to pay bills, Send money, do Recharges to friends & family, Travel tickets & Book movies.

The goal as the company mentions is to get unregulated businesses in the economy to the mainstream economy. Taking most of all the transactions happening in the country and enabling them digitally is an almost impossible thought. This is such a behemoth task but the digital payments provider is not looking backwards.

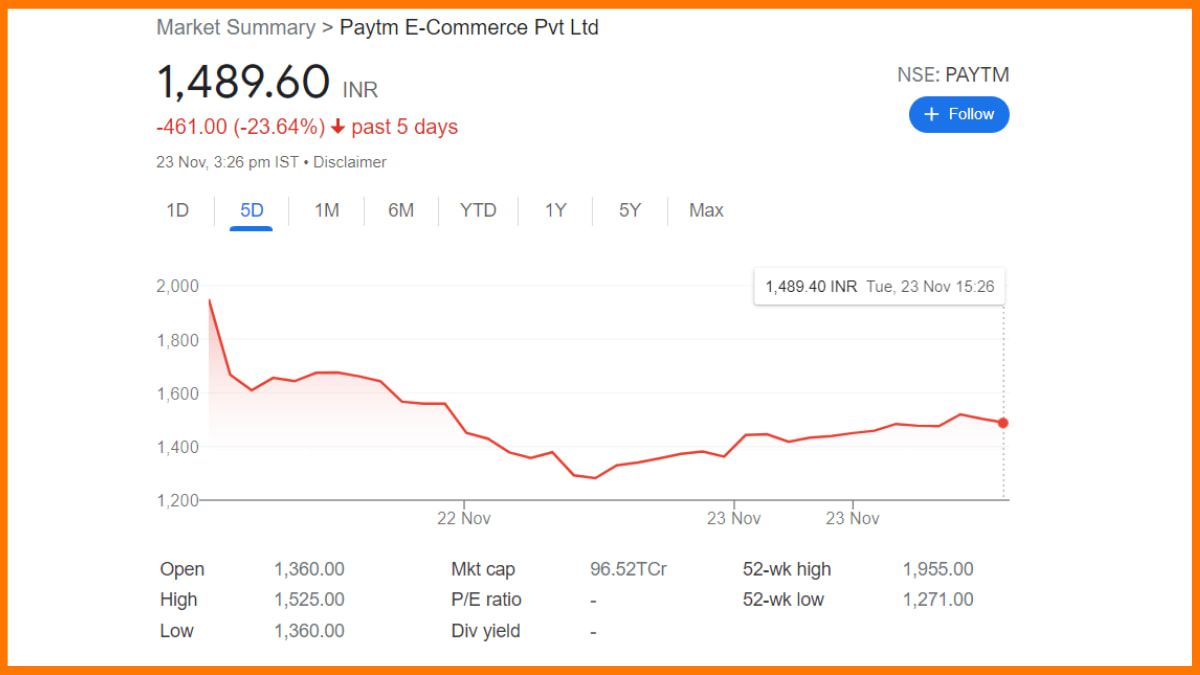

It recently was listed in the stock market. It was a huge IPO. Investors all around the world were excited. It is now the biggest IPO ever in the history of the stock market in India. Previously it was Coal India which raised about 15,000 crores. Paytm is now listing to raise 18,000 crores rupees.

Paytm has been a loss making startup for a long time now. It is not earning at all. The startup has losses of about 4000 crore in FY 2019. That went to 3000 in FY 2020 and then to 7000 crore.

Even though the losses are declining, this doesn’t hide the fact that the company is not earning at all. So why is that? Why a loss making company is valued so much. It is valued at over 16 billion dollars. Moreover it is able to raise money from big VCs. Asset management companies are pumping money into this loss making startup.

The reason why the company is left with such abundance of money is that it is a startup. An immensely successful startup. Which tries to get customers first, that is to capture a large market share.

After getting a good chunk of the market, they will monetise themselves and earn ridiculous amounts of real cash. This is how most startups model work. They hack growth and become big organisations. They try to establish a strong company and reduce the time that is required to build a strong company.

The startup has also already raised 8000 crores in its anchor round. Its initial public offering of Rs 18,300 crore. Top sovereign wealth funds around the world, financial investors such as Canada’s CPPIB, Singapore’s GIC, Alkeon Capital, BlackRock, Abu Dhabi Investment Authority are among those to have picked up stakes in this fintech.

The parent organisation of Paytm is One97 communications. Other than recent fundraising rounds, One97 communications has shareholdings by top capitalists and Asset management companies. It has a 2.8 percent stake by Berkshire Hathaway, the company of world’s best known investor Warren Buffet. It has Ant group as a shareholder, that is as a subsidiary of Alibaba, founded by China’s richest man, Jack Ma.

The promoter or the Chief executive officer of the company Vijay Shekhar Sharma has a stake of around 14 percent of the whole mammoth organisation. Other notable shareholders include Alibaba itself, Softbank, Elevation Capital. With all these big supporters this company recently filed for an IPO.

The IPO was huge and reportedly the biggest that Indian markets have ever seen. Unfortunately, The public offering of Paytm fell down immediately after the listing. In fact today is the second day of the shares trading in the market. They went as low as 37% since the IPO.

Let us discuss the whole public offering scenario in minute detail.

Paytm Initial Public Offering (IPO)

Initial public offering is the offering of shares to the general public. General public here means retail investors and big investors as well. When it happens for the first time, we call it the initial public offering. Accordingly it can happen second or third time also, in that case we will call it FPO or further public offering.

IPO or any public offering happens when a company decides to take money from general people and not raise more rounds of funding. The money is needed to fuel growth. It is needed to scale the enterprise and thus the money becomes the new capital.

In Paytm’s case, the company wanted to raise a little over 18,000 crores. This is the biggest amount ever raised in India. So the Paytm IPO is expected to be the biggest offering in Indian markets yet. The breakdown of the total money is that, 8000 something crores were new offering of shares. So, they were a fresh issue. And the remaining 10,000 crores were offered for sale, that is existing shareholders selling their share of stake. The price band of the shares ranged from 2080 to 2150 rupees per share. The valuation of the company at the time was about 1.5 lakh crores.

The RHP is a legal prospectus for every new listing company. The red herring prospectus (RHP) of this company said that it expects to incur losses for more years before it starts making profits. The opening IPO date was 8th of November and the last date to apply was 10th of November. Face value of the share was One rupee. So it was going to be listed at a premium.

Paytm Share Price

Paytm Listing Losses

The Paytm IPO was subscribed only 1.89 times on Nov 10, 2021 17:00. The public issue subscribed 1.66 in the retail category, 2.79 in the QIB category, and 0.24 in the NII category. It shows that investors weren’t much interested in it or the IPO was so big that it just covers up all the demand.

Paytm shares fell down by about 10.35% to Rs 1,402 against previous close of Rs 1,564.15 on BSE. Market cap of the company, which remained above the Rs 1 lakh crore mark on the listing day, faced down to about Rs 93,490 crore on the first listed day. This loss making startup is acting like a money guzzler.

Paytm IPO Reviews

Here are some reviews of the IPO from major and big fund coordinators and Asset management companies.

International Brokerage firm Macquarie published a report on Monday. A second report on Paytm, maintaining its earlier target price of Rs 1,200 and an ‘underperform’ rating after its first one on listing day, ruffled the feathers of investors. This means that they concluded that the price of the share should be Rs1200 and the listed price is well overvalued.

On the second day it went down to 40 percent. Exactly to the price what Macquarie anticipated but they released it after Paytm was listed on the stock market.

After the first day listing loss, investors panicked and tried selling this. This is a huge reminder that if you pick up a stock or an IPO to invest, do your own research. After an honest report only should you consider investing.

Mobikwik whose IPO was in the turn later in time also postponed their listing. Witnessing huge losses that investors incurred in Paytm’s IPO. Let us see some of the anticipated reasons that we all can see which led to the downfall of Paytm on the very first day of being listed.

Anticipated Reasons for the Downfall of Paytm IPO

Some of the most common seen and anticipated reasons for Paytm losing value are listed here. Let us figure out why this mega IPO is seen as a loser in the race for listing gains.

Overall Market Conditions

The current market conditions are also somewhat affecting the IPO listing. The current market trends show a downward trend. Today, you can see news of the market falling down 1170 marks. The day’s loss was the biggest for the index in over six months.

This downward trend of Sensex is mainly due to Reliance sliding down 4.4% after it announced reviewing of a recent deal. Outside India and around the globe, inflation tension is rising and so are the Covid cases in Europe. All these activities have also in some sense affected Paytm’s downward trend. It is at about 37% down now from the listing day.

Paytm’s Financial Situation

If you have invested in Paytm looking at the fundamentals then you know for a fact that Paytm is not going to make profit anytime soon the profitability game is slightly a long way ahead. We still don’t know when Paytm will become profitable.

Another fact is that the newly listed companies right now are also trying to be very smart because they know that there’s heavy retail participation in the market. A lot of people like me and you will go for listing gains so Paytm came out and did a mega IPO which was 18,000 crores.

Size of the IPO

Listing gains comes when supply is short and the demand is quite big. In layman language, when the offering is small, listing gains are expected. In Paytm’s case, the IPO is so big that it covers the overall demand and it leaves no space left for a force to push the price up.

The Paytm IPO was subscribed 1.89 times on Nov 10, 2021, 17:00. The public issue subscribed 1.66 in the retail category, 2.79 in the QIB category, and 0.24 in the NII category. So you see all the demand was covered with the hugeness of the IPO and less space was left to pump the price up.

What should you do if you have bought Paytm’s Share?

If you are someone or you know someone who is stuck with this stock. I would suggest two options. First is to just get rid of this stock as quickly as possible. Second, if you are an investor with a long term horizon then you can consider holding this stock. But keep this in mind that this stock will take a good amount of time to go profitable.

The reason is as we discussed earlier is that the company is making consistent losses for now. It also is forecasted that the company will only scale for now and it has no immediate plans to bring the profit perspective to the table.

As of now, the company is down to 30-40% and it is going to take time to take back these percentages of losses, only then one can expect some profits. Again if you are looking for quick listing gains, then maybe this might not be the probable right stock and time to stay invested in this stock.

For all the inventors who didn’t apply for this IPO this is the right moment to be aware of such scary situations. It is always best to research before you invest your money. It is really a scary situation when you invest in a big loss making startup, and you are stuck in it. Startups can be a blackhole for money for a very long time.

Conclusion

The reason for such a hype of this fintech company being listed is that, India is the second most populous country in the world. China, the top populous has already had their share of the fintech revolution. They are also harsh on regulations. Now it is India’s turn. India is the next hub for investors that may be domestic or foreign.

Digital payments are expected to grow up to 5% in the next five years. Digital commerce will likely move up to 3.3%. With these things in store, India becomes the next hot spot for investments.

Jio and digital revolution boosted the Paytm business. Demonetisation skyrocketed it. Their tagline “Paytm karo” became a household thing during these times. With the government promoting digital economy and cashless transactions, hope is high for fintech revolutionaries like Paytm.

The listing losses taught many people to do their own research before investing anywhere. The company is expected to take a long time to jump to profits.

Whether Paytm will change Indian payments face or it will dissolve, this is to be seen and only time will tell. One thing is for sure, it has massively added to the cashless economy that the world is striving towards.

FAQ

What is Paytm IPO?

Paytm is a digital payment system, the company lunched its IPO in Bombay Stock Exchange with largest initial public offering (IPO) with the value of Rs 18,300 crores.

Why did Paytm IPO flopped?

Some of the common reasons why Paytm IPO flopped was Overall Market Conditions, Size of the IPO, and Paytm’s Financial Situation.

Company Profile is an initiative by StartupTalky to publish verified information on different startups and organizations. The content in this post has been approved byYap.

Technology has transformed the way financial transactions and operations happen. Today making and accepting payments, receiving loans, everything has become simpler than ever before. All thanks to tech startups, that are coming up with amazing products that have made financial operations much easier for financial institutions, business owners, and consumers. Chennai-based ‘Yap’ is one such startup that this revolutionizing the way banks and other financial institutions offer services to their customers. Yap provides tools that let banks and financial institutions design customized and convenient solutions for their customers. Here is more about Yap.

Yap offers a payments-as-a-service infrastructure that can handle all types of retail payment assets. Yap’s Application Programming Interface (API) platform allows digital platforms, fintech companies, and offline businesses to offer personalized solutions to their end customers, by linking them with other fintech platforms and banking and non-banking financial firms.

Yap’s functional APIs, let its clients receive and transfer funds through Wallet & Cards, Cross Border Payments, Gift Cards, Fleet Spends, Just-In-Time Funding, UPI as well as other payment methods. Consumer, corporate, small business, and credit card loans are among the products it offers.

Yap’s modular platform ‘bank in a box’ enables its clients to offer products such as opening bank account, credit, online payment, toll payment, foreign exchange solutions, etc.

Many companies in Nepal, India, New Zealand, the UAE, Australia, and the Philippines are served by YAP. Around 20 Indian banks, including ICICI Bank, Yes Bank, and RBL Bank, as well as numerous consumer internet companies like Ola, Cred, Swiggy, and also large NBFCs like Muthoot, TVS Credit, Bharat pe, Razorpay, Finin, etc use YAP’s services on the lending space.

Yap – Latest News

In March 2021, Yap raised $10 Million in funding from investors like Flourish Ventures and Omidyar Network India. The fundraising round included participation from YAP’s current investors, including Beenext, 8i Ventures, and Better Capital.

“We are uniquely poised to cater to new cohorts of distributors as more firms embed financial services into their digital platforms. This investment allows us to strengthen our technology teams, build new capabilities as well as reach new markets across Asia,” Madhusudanan R, co-founder at Yap, said.

Madhusudanan R is the Chief Executive Officer & Founder at YAP. He is a fintech entrepreneur with deep-rooted experience in building and scaling Payments businesses across Asia.

Prabhu R

Prabhu R is the Co-Founder & Chief Operating Officer at YAP.

Yap – Startup Story

Madhusudanan R. and Muthukumar A and came up with the Yap idea during the office tea breaks. The founders who worked at Visa Inc in Mumbai from 2010 to 2012, often realized how big banks were lagging behind in digitizing their services. The focus of these conversations was always on how the financial industry might fix this problem. Finally, Madhusudanan and Muthukumar, came up with a solution themselves and founded Yap in 2014.

The Yap founders observed how banks work in India, through their combined expertise of over a decade working for Visa, Citibank, and Paypal. They understood that due to their aversion to developing new digital products, banks were unable to reach a whole new set of clients. Yap is a solution to these problems, Yap’s is empowering many banks, financial institutions, and businesses to offer various customized solutions to its customers.

YAP’s unique API (application programming interface) gives banks and fintech businesses the tools they need to create new payment systems. This shortens the time it takes for these businesses to acquire consumers who want simple and quick electronic payment options.

“When we started, banks in India didn’t use any APIs. In other markets, like the US, this phenomenon started ten years ago. In India, it started around 2014–15, when a few digital payment companies started to grow,” Madhusudanan, co-founder of YAP, told.

The firm claims to deal with 15 banks in India at the moment. Apart from providing an API for payment integration, including UPI payments, YAP also assists them in acquiring corporate clients, which are often digital financial institutions such as neobanks or the fintech divisions of big corporations.

“They don’t have to spend any money on this, and they can reach a lot larger audience without having to spend money on client acquisition,” Madhusudanan explained.

Yap – Mission and Vision

Yap’s mission statement says, “We are focused on user experience and customer retention. We are constantly thinking of new use cases and ways to serve our customers across all their financial needs as seamlessly woven into their daily routine life as possible.”

YAP is on a mission to transform every business into a fintech.

Yap – Name & Logo

Company Logo of Yap

Yap – Business Model and Revenue Model

Yap provides B2B tech solutions to financial institutions and businesses. The YAP platform connects companies to licensed banks, financial institutions, and financial infrastructure such as UPI/card networks through its extensive Application Programming Interface (API) libraries. Within a few weeks, a company may connect to YAP’s platform, choose goods and banking partners, and roll out financial products to its consumers or vendors. In addition, YAP oversees essential continuing activities like reconciliations and compliance monitoring. YAP now serves over 200 fintech with an API platform.

Madhusudanan R – Chief Executive Officer & Founder

Yap – Funding and Investors

Date

Round

Amount

Lead Investors

Mar 16, 2021

Series B

₹732M

Flourish Ventures, Omidyar Network India

Apr 21, 2020

Series A

$4.5M

BEENEXT

Feb 13, 2020

Seed Round

₹100M

Amrish Rau

Yap – Growth

Around 20 Indian businesses, including ICICI Bank, Yes Bank, and RBL Bank, as well as numerous prominent consumer internet companies like Ola and PaisaBazaar, use the service.

“We are uniquely poised to cater to new cohorts of distributors as more firms embed financial services into their digital platforms. This investment allows us to strengthen our technology teams, build new capabilities as well as reach new markets across Asia,” Madhusudanan said.

The 6-year-old firm offers comprehensive Application Programming Interfaces (APIs) to banks, startups, and consumer online businesses. The new funds (raised in March 2021) will be utilized to expand into foreign markets and bolster the team with new hires.

Yap’s major plans include expansion to new geographies and expanding the team. According to Madhusudanan R, co-founder of YAP, the company intends to grow to Bangladesh, Saudi Arabia, Oman, Egypt, Vietnam, and Indonesia.

India’s rapidly digitizing financial environment, according to Amol Warange, head of Omidyar Network India, would provide chances for YAP to expand.

“We think that digital enablers like YAP can catalyze financial inclusion and promote adoption of financial products among the next 500 million Indians who are projected to access the internet for the first time via their mobile phones” Warange added.

Yap – FAQs

What does Yap do?

Yap offers a payments-as-a-service infrastructure that can handle all types of retail payment assets. The company’s platform links banks, financial institutions, enterprises, payment networks, and merchants to build an interoperable payment platform that allows businesses to quickly design and carry out their own customized payment solutions.

Which country is Yap based in?

Yap is a Chennai-based, Indian fintech company.

Who founded Yap?

Yap was founded by Madhusudanan R and Prabhu R.

Which companies do Yap compete with?

Open Bank Project, Decentro, TrueLayer, Teller, Inc., Plaid, Konsentus, Figo, Quovo, and Instantor are the top ten competitors of YAP.

Company Profile is an initiative by StartupTalky to publish verified information on different startups and organizations. The content in this post has been approved byRecko.

Most entrepreneurs stress the challenge of reconciling transactions; it’s one of those necessary evils that everyone has to deal with but no one wants to do. We’ve heard individuals complain about the necessity to reconcile payments over the years in banking and payments. Over last few years, there has been a continual increase in the number of online payments, making it tough for many businesses, banks, and financial firms to keep track of expenses flowing around the organization. Recko is a corporation that specializes in financial reconciliation. Started with the mission to help businesses manage their financial operations with agility, simplicity, and innovation, Recko aids businesses that deal with several legs of payment processing as part of their daily operations in keeping track of and reconciling all financial transactions. Recko has reconciled over 250 million payments valued at over $2 billion in its first year alone.

In October 2021, Recko got acquired by San Francisco-based Fintech company Stripe. Stripe offers a wide array of services including payment and billing services, and tools for managing business operations. By acquiring Recko, Stripe is set to expand its services further. As per the deal, Recko’s entire team will join Stripe’s remote engineering hub and will work to develop and scale Stripe’s products.

About Recko and How it Works?

Through Accounting reconciliation, businesses can keep track of their transactions. With the expansion of business, reconciliation becomes a tough job. Especially with more and more online transactions being done these days, reconciliation has become even more cumbersome. This is where Recko helps.

Recko is a Software as a service reconciliation artificial intelligence-based software that assists finance teams at eCommerce marketplaces and transactional platforms in keeping track of the entire transaction cycle and business deals in order to avoid slipping and tripping hazards.

“The finance department on the merchants’ end is continuously dealing with this complexity of matching the right amount to right order, returns/ replacements and a lot of orders also move between months. All they have excels, spreadsheets and traditional ETL (extract, transform, load) tools which are cumbersome and error-prone. This is where we come into the picture,” said Saurya Prakash Sinha, Recko cofounder and CEO.

Recko was created with the goal of providing financial stability to businesses with significant transaction volumes, such as e-commerce platforms, insurance companies, and banks, by automating the entire reconciliation process. It ensures that each transaction is recorded and that all settlements are completed on time because it is an independent third-party transaction reconciliation layer.

“This also helps when customers have to be refunded as we use many different ways to make a single payment these days (including wallets, vouchers, gift cards, net banking and CC),” added Prashant Borde, cofounder and CTO at Recko.

Besides reconciliation, Recko also helps businesses in commission calculation, Payout creation, and reporting, to aid businesses to track, manage and account money end to end.

Recko’s current team consists of 60 people with extensive experience working for e-commerce and fintech companies such as Flipkart, Amazon, Nutanix, PhonePe, Ola Money, Razorpay, and others.

Recko – Logo

Recko’ s Company Logo

Recko – Founders and History

IIT Gandhinagar alumni Prashant Borde and Saurya Prakash Sinha launched Recko in 2018.

Founders of Recko – Prashant Borde and Saurya Prakash Sinha

Prashant and Saurya are serial entrepreneurs and have have robust industry experience. Prashant Borde co-founded shared computing platform GridAnts in 2012, which was later renamed Cubeit. The platform was acquired by Myntra in 2016, after which Prashant joined Jio.

Saurya worked for industry leaders like Flipkart and Phone Pe. In 2015, Saurya co-founded urban logistics and on-demand delivery platform ‘Townrush’, which was later acquired by Grofers. Saurya joined Grofers as AVP(product) after the acquisition of Townrush. In 2017, Saurya founded Recko along with Prashant.

The duo had hands on experience of developing processes that aided the product and finance teams in contributing to the company’s growth and accelerated financial governance. This led them to discover that organizations of all sizes battle to keep track of payments and face manual restrictions when it comes to reconciliation, computations, and scaled monetary operations management. Thus Saurya and Prashant decided to intervene and help businesses to manage their finances better by simplifying reconciliation, commission calculation, Payout creation, and reporting.

According to its founders, Recko reconciled transactions totaling $2 billion in its first year of business. Grofers, Dunzo, FreshMenu, and Meesho are just a few of its clients. It also has different monetizing methods in place, depending on the client’s needs, including volume and per-transaction costs.

Following are some of the primary gaps Recko is trying to close –

Unstructured data in large quantities

Use of a large number of people

Transparency and traceability of operations are lacking.

Time and expense spent on reconciliation have grown.

AI plays a role in resolving these issues on various levels. First, algorithms aid in the extraction of relevant information and analysis from more than 80% of data, which is critical in the financial domain because fintech models would be unable to function without data.

Furthermore, because they can’t always trace an error back to its source, most organizations set aside a specific proportion of revenue error to accommodate for reconciliation checks. To close this gap, Recko automates the reconciliation process, making it possible to track financial data throughout its full lifecycle. It accomplishes this by utilizing APIs to link with payment gateways, banks, and merchant order management systems, allowing firms to track receivables and uncover settlement problems. According to Recko, this reduces manpower investment by 50 percent to 60 percent.

Recko – Mission and Vision

Recko’s mission statement says, “Recko was started with the mission to help businesses manage their financial operations with agility, simplicity, and innovation. Today’s businesses need a collaborative interlock between their finance, product, and business functions to grow exponentially and stay ahead of the competition. Be it reconciliations, payment operations or complex commission calculations; Recko does it all.”

Reconciliation – Bringing your company’s transactions up to date in terms of accuracy, efficiency, and speed.

Commission Calculation – Automate your entire charge calculating procedure and keep track of external payment SLAs.

Payout – To disburse payments to customers and subcontractors, the company integrates easily with payment partners.

Recko – Business Model & Revenue Model

Recko is a B2B company, and earns revenue by charging subscription fee from its clients.

Without writing a single word of coding programs, Recko allows financial teams to ingest, enrich, and reconcile millions of transactions in hours rather than days. Recko cuts labor by 50 to 60 percent while keeping a close eye on transactions to guarantee money goes to the right parties at the right time with the correct deductions.

Recko is now processing enormous amounts of transactional data to digitize financial control within organizations, as well as developing Machine Learning models to detect abnormalities, risk, and intelligence in the money flow.

Recko – Revenue and Growth

The revenue for the Fiscal Year 2019 was USD 388K, up from USD 186K in the previous year. Recko’s customer’s includes top marketplaces like Grofers, Meesho and Dunzo.

Recko – Funding, and Investors

In its latest round of Series A funding raised on April 2020, Recko received $ 6 million. Vertex Ventures SEA and India led the financing, with Prime Venture Partners joining as an existing investor. Here are Recko’s funding details-

iPaymy, Pulse iD, SAP Concur, Sage Intacct, G2 Deals, Bill.com, Tradeshift, Invoiced, DocuWare, Spendesk, Riovic, and SureCash are among Recko’s main competitors.

Recko – Challenges Faced

The product needed to be stable because the company was working with extremely large data volumes. As they add features to the product, it continues to evolve. The aim is that the number of problems and inconsistencies will decrease as time goes on. Since the platform handles finances, the team at Recko needs to be extra careful so that nothing goes wrong.

“We needed to be precise, and we needed to be correct at scale. The crew spent a significant amount of time double-checking the figures.”, the Recko CEO said.

On the technology side, figuring out how to process these transactions was a significant issue for everyone on the team, since this used to take them over 3-4 days to handle more than 50-60 million transactions. They can now complete it in 30 minutes.

” for reconciliation, we are almost running at 100 million transactions in one hour. So the systems are becoming much faster. The idea is how do we do this at a much cheaper cost and faster. So this is where a lot of investment is going in,” said the CEO, Saurya Prakash Sinha.

Supporting scale was one of the issues they confronted. To make scale and security a basis in the architecture, Prashant says they had to redo a major portion of the first iteration.

“As we onboarded new customers, we realized that businesses looked at data very differently across industries. We did not want to leave any stone unturned, but we had a mission — to give the best of it. We added analytics, custom reports, commission calculation, and other integrations including storage services, payment gateways, and banks,” says Prashant.

The team quickly began working with clients from various industries and geographical places. Recko introduced geographies such as Southeast Asia and the European Union. Versioning was also released to support audit logs and time travel capabilities that needed to be reworked to allow future growth.

“We are planning to open APIs as well so that they can be integrated deeper into companies’ tech stack to solve a multitude of problems. Our long-term goal is to provide enough insights that enable businesses to make financial decisions in real-time,” says Prashant.

Recko – FAQs

What does Recko do?

Recko is a Software as a service reconciliation artificial intelligence-based software that assists finance teams at eCommerce marketplaces and transactional platforms in keeping track of the entire transaction cycle and business deals in order to avoid slipping and tripping hazards.

When was Recko founded?

Prashant Borde and Saurya Prakash Sinha launched Recko in 2017.

Which companies do Recko compete with?

iPaymy, Pulse iD, SAP Concur, Sage Intacct, G2 Deals, Bill.com, Tradeshift, Invoiced, DocuWare, Spendesk, Riovic, and SureCash are among Recko’s main competitors.

Company Profile is an initiative by StartupTalky to publish verified information on different startups and organizations. The content in this post has been approved byEzetap.

With mobile phones and applications changing the digital landscape, businesses have acknowledged the need for a shift in how they serve their consumers. Mobile point of sale programs, also known as mPOS apps, are becoming increasingly popular, according to industry estimates. Because of technological advancements in Bluetooth and Wi-Fi connectivity, mPOS adoption has been extremely successful all over the world including India. Bangalore-based startup Ezetap is a major mPOS solution provider in India. Here is more about Ezetap, the startup’s journey, and its functions.

As of February 2018, Ezetap announced the launch of EzeSmart, a smart GPRS gateway with Aadhaar payment and eKYC that is fully accessible.

EzeSmart, which is based on Ezetap’s global payment acceptance platform, is the first POS terminal in the country that can take all types of payments, including UPI, Bharat QR, and Aadhaar Pay. It can also take payments from a variety of mobile wallets as well as credit and debit cards. It’s a smartphone-integrated terminal that lets companies run any of their system apps on it.

The company stated to the press that EzeSmart is tailored to support the strategic and technical needs of various industrial sectors, including govt., by allowing a person with an Aadhaar-linked bank account to transact conveniently by simply touching their finger on the device’s fingerprint reader. This allows microfinance companies who deploy this terminal to provide services to rural consumers and accept payments online.

What is Ezetap?

Ezetap is one of the first companies that came up with digital payment solutions in India. The company’s first product launched in 2013, was an mPOS card reader that could be connected to a smartphone via the audio jack. Currently, Ezetap has a variety of digital payment solutions that let businesses accept digital payment seamlessly. Ezetap offers tailor-made payment solutions for different sectors like small and large retail shops, eCommerce and logistics companies, and government organizations.

From businesses to cab drivers to supermarkets and pizza delivery drivers, the technology allows anyone to accept cards. Online retailers, insurance companies, restaurants, and hotels are among the clients of the company.

Ezetap started with a single payment offering and pivoted to a SaaS model in 2020. Ezetap’s payment solutions come with many attractive features like multibank acquiring and auto-reconciliation and offer a variety of value-added services that businesses can opt for.

Ezetap – Name, Logo, and Tagline

Ezetap has made making and receiving payments as easy as a tap. That’s where the company name is derived from.

Ezetap’s Company Logo

Ezetap’s tagline is, “Transforming the world of payments”.

Ezetap – Founders and History

Ezetap was founded in 2011 by Abhijit Bose and Bhaktha Keshavachar. Both the founders had previous expertise in payments and hardware firms, and they merged their talents, skills, and knowledge to create this solution.

Abhijit Bose who served as the CEO of Ezetap exited the company in 2018, after which the then CFO of Ezetap, Byas Nambisan took over as the CEO.Presently Byas Nambisan is the CEO of Ezetap.

In 2019 Bhaktha Keshavacharalso exited Ezetap to start his own deep tech startup, Chara Technologies.

Founders of Ezetap – Abhijit Bose and Bhaktha Keshavachar

At the start of the decade, Internet connectivity and smartphones were becoming commonplace in India, and e-commerce companies were gradually gaining popularity. Ezetap founders Abhijit Bose and Bhaktha Keshavachar spotted an opportunity to make payments more widely accepted in India. Ezetap became one of the first startups to try to convert Cash on delivery shipments to electronic payments, which was one of the earliest application cases for Ezetap in the year 2013.

“We built an EMV-compliant payment device that could take payments in conjunction with a commercially available smartphone and a card reader designed and assembled in India. We also created a payments SDK that would work behind a company app, hiding the complexity and compliance rigmarole of payments behind the ‘pay’ button,” Bhaktha Chaterjee, Head of Products at Ezetap.

The company chose to stop producing its own gadgets in India in 2018 and instead started sourcing them from overseas manufacturers. The Ezetap team is highly focused on improvising its services, and there are even instances where Ezetap team members accompanied e-commerce delivery agents to the doorsteps of end-users to collect feedback on the payment experience.

Ezetap – Mission and Vision

Ezetap’s mission is to empower businesses to receive payment seamlessly via any mode of payment.

Ezetap’s mission statement says, “Our Mission is to be the single platform through which businesses complete any financial transaction with their customers, supporting every instrument and method that those customers want to use”

Ezetap’s Universal payments banking partners are Citibank, HDFC Bank, American Express, Axis Bank, ICICI Bank, Mashreq Bank, RBL Bank, State Bank of India, and Yes Bank. The State Bank of India also partnered with Ezetap as its MPOS partner, with the goal of expanding electronic payments and micro-ATM to every corner of the country. However, this SBI-Ezetap partnership came to an early end. Recently Ezetap partnered with Axis Bank for Launching the My Vyapaar app, an app dedicated to retail businesses. The app comes with many features like attractive buy now pay later options and encourages digital payment by offering exciting rewards.

Ezetap – Business Model

Ezetap pivoted to a Software-as-a-Service business model, allowing retailers to accept transactions online via physical cards, internet payments, and mobile wallets with a single click via UPI, at a time when PoS firms make money from transaction fees.

The startup has altered the payment procedures of brick-and-mortar merchants, e-commerce players, enterprises, government agencies, and financial inclusion institutions using a Software-as-a-Service payments system.

Ezetap – Revenue and Growth

Ezetap’s operating revenue increased by 3% to Rs 45.06 crore in 2017-18, up from Rs 43.77 crore the previous year. According to the papers, the net loss increased to Rs 40.47 crore from Rs 30.71 crore during the period. From Rs 78.69 crore to Rs 92.17 crore, the company’s expenses climbed by 17%.

During the time, employee benefit expenses, such as provident fund, gratuity, and compensated absences, increased by 14% to Rs 33.33 crore from Rs 29.01 crore.