When it comes to managing expenses and bills, especially when one has low funds. This becomes really pressurizing and people start looking for sources to lend money from. In such situations, borrowing from friends and family could be embarrassing and hectic. And depending upon banks could cost major interests. So where should we look?

Well by acknowledging these situations and deals, online money lending apps are developed. These provide the facility to lend money through digital platforms without any further issues.

Multiple companies are providing the facility of offering loads immediately with minimal competitive interest rates and required tenure durations. These companies facilitate the loan very easily and quickly as compared to usual bank loans.

With keeping such progress in mind, India has developed numerous digital lending companies whose finances can manage smoothly. India is evolving to a great extent in the digital sector and financial inclusion. The country has cash for transactions. But with the evolving method of development and modernization, India is shifting toward a cashless economy. To understand its development more prominently, let’s look at the top 10 digital lending platforms in India.

Best Digital Lending Platforms in India – Lendingkart Website

The prominent digital lending platform, Lendingkart was founded in 2014. It works by offering different capital loans and company loans vary from small to medium-sized businesses across India. They are widely famous for providing capital completely through an online platform and require minimum documentation for the procedure to begin.

For young entrepreneurs, managing their finances becomes quite hectic and it deviates them from focusing on their business growth. That’s why Lendingkart has taken the initiative to make capital funding easily available for entrepreneurs so they don’t have to worry about the cash-flow gaps. Lendingkart is a company established in Ahmedabad, Mumbai and Bangalore. But, its services are accessible throughout the whole of India.

2. Pine Labs

Lending Platform

Pine Labs

Loan Amount

From ₹25,000 to ₹5 Lakhs

Loan Tenure

90 Days

Best Digital Lending Platforms in India – Pine Labs Website

Pine Labs is one of the leading fintech companies in India established in 1998 that provides digital lending services. The company is quite famous for its incredible facility of transforming the mobile NFC into a card machine and activating the service of accepting all types of payment digitally which also includes the ‘Tap n Pay’ card as well.

Pine Labs have brought tons of services for the retailers including multi-channel, different payment options, brand offerings, risk assessments, analytics, and many more.

It provides working capital loans for small to medium businesses. Their loan application process is quite simple and you can apply for a business loan through their website or their app myPlutus.

Pine Labs’ services and technologies are widely preferred and used by more than 100,00 merchants all across India and also, many Asian companies. According to the estimations, PineLabs’ cloud-based technology has the power of over 350,000 PoS terminals; that too in more than 3,700 cities.

3. MobiKwik

Lending Platform

Mobikwik

Loan Amount

Upto ₹5,00,000

Loan Tenure

6 to 36 Months

Top Loan Aggregators in India – MobiKwik Website

MobiKwik is a very prominent mobile payment company that works by connecting the consumers together with the merchants and many online sellers. The company is established in Gurgaon, Haryana, India.

Mobikwik is a private company that has more than 550 employees. Since the establishment of this company, the company has raised a total of 118 million USD from over 8 funding rounds.

Mobiwik provides instant personal loans. You can download its app and once the loan is approved it will be credited to your wallet.

₹1 Lakh to ₹15 Lakhs (unsecured) or up to ₹2.5 Crores (secured)

Loan Tenure

6 to 48 Months (unsecured), Up to 84 Months (secured)

One of the biggest lending companies, Shiksha Finance, is an education-based finance firm. Shiksha Finance provides the services of funding parents for school fees by reducing the school drop-out rates. It also offers capital to educational institutions for the development of buildings, properties and working capital.

Shiksha Finance has loans that range from INR 10,000 to INR 50,000 with a return duration of 6 to 10 months. The loans which Shiksha Finance provides can be utilized for educational based purposes such as school fees, tuition, luggage and stationary.

5. MoneyTap

Lending Platform

MoneyTap

Loan Amount

Upto ₹5,00,000

Loan Tenure

36 Months

Best Digital Lending Platforms in India – MoneyTap Website

The Bengaluru based lending company, MoneyTap is known for its huge service of offering credit lines for the consumers as their loans, with the partnership with RBL Bank. MoneyTap is now counted among the leading lending businesses. Recently, the company received the license of NBFC for co-lending space together with their lending partners.

MoneyTap has offered many great features among which, the minimal documentation procedure for a personal loan is the most special one. Moreover, its app version also provides the facilities for tracking down your borrowing records.

6. Paytm

Lending Platform

Paytm

Loan Amount

Upto ₹2,00,000

Loan Tenure

6 to 36 Months

Fintech Lending Companies in India – Paytm Website

The biggest digital lending wallet company Paytm is wildly famous in the minds of Indians. The company is established in Noida, Uttar Pradesh. Paytm has grown to a great extent and now, millions of downloads have been made.

The development the company has received is breathtaking. It employs more than 9000 people and has a revenue of a total of $118 million. Paytm is highly specialised in online shopping as well.

Best Digital Lending Platforms in India – PolicyBazaar

The company is counted among the top leading online insurance companies, PolicyBazaar was established in the year 2008 and headquartered in Gurgaon, Haryana, India.

It is online life insurance as well as a general insurance aggregator company. PolicyBazaar is very popular among Indians for its incredible services and holdings. It employs over 2500 people and has an annual revenue of $21 million (as estimated in 2017-18).

The current CEO of PolicyBazaar is Yashish Dahiya who is also one of the founders of this company. It has raised around US$ 346 million through 7 funding rounds.

8. Capital Float

Lending Platform

Capital Float

Loan Amount

₹50,00,000

Loan Tenure

Upto 36 Months

Best Digital Lending Platforms in India – Capital Float Website

Capital Float is one of the leading lending companies in India. It is acquired by CapFloat Financial Services. Capital Float is popular for its amazing service of specialised financial loans and business credits.

Capital Float has a partnership with some prominent companies such as Shopclues, Paytm and Uber. The company lends the potential borrower through its system of proprietary loans. Capital Float is now targeting established store owners and small merchants.

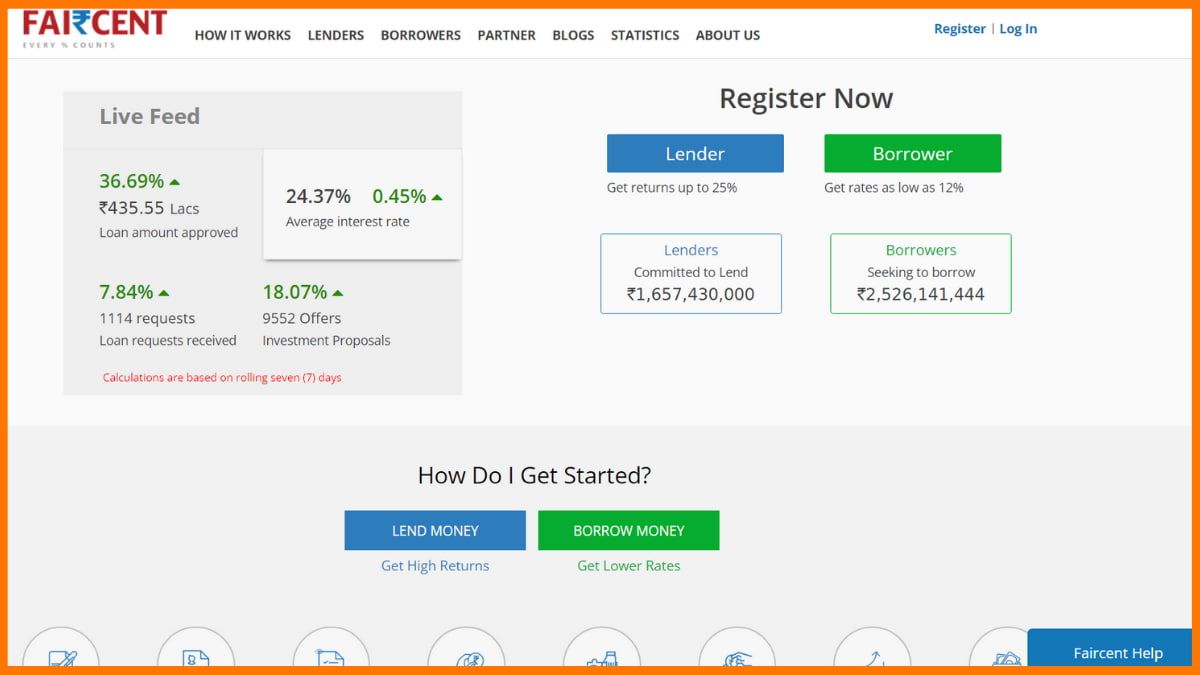

9. Faircent

Details

Information

Loan Amount

₹5,00,000

Loan Tenure

6 to 36 Months

Best Digital Lending Platforms in India – Faircent Website

The largest and first Indian peer-to-peer digital lending platform, Faircent is known to be absolutely amazing. It is officially registered by the RBI. It provides a safe marketplace for people to loan money to a borrower. Faircent facilitates the credit to organizations and individuals who are interested in lending money.

Faircent provides the absolutely convenient procedure of lending the required money to those who need it, at reasonable interest rates.

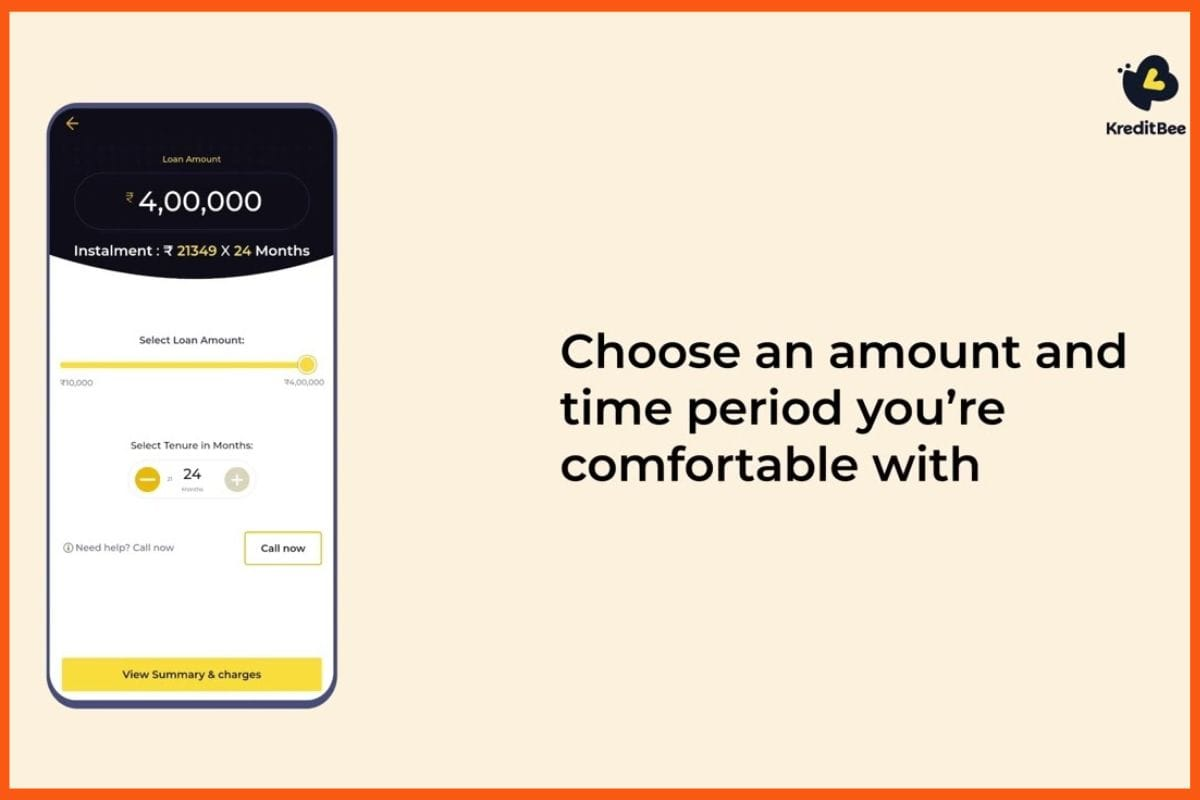

10. KreditBee

Lending Platform

KreditBee

Loan Amount

₹5,00,000

Loan Tenure

6 to 36 Months

Lending Service Providers in India – KreditBee

KreditBee is a Bangalore-based fintech that offers quick personal loans up to INR 2,00,000 for working professionals. Using easy online KYC, the loan process is fast and simple. KreditBee is one of the top lending companies in India.

Backed by trusted investors like ICICI Bank and supported by banks like AU Small Finance, KreditBee serves over 5 million customers.

The process is mostly paperless, sign up on the app, and within 15 minutes, approved loans are transferred instantly to your bank account.

In India, there are many fintech companies that are providing the service of digitally lending money very easily with the minimal documentation procedure. Today, many apps have been developed by these companies to make the transaction of money absolutely susceptible. And for those who require a personal loan or business loan, can easily get one. That’s why we listed these top digital lending companies in India.

FAQs

What are some of the top digital lending companies in India?

Lendingkart, Pinelabs, Mobiwik, Policybazaar, and Paytm are some of the top digital lending companies in India.

How does a lending company work?

Lending companies provide loans to an entity, which is then expected to repay its debt.

How many fintech companies are there in India?

There are around 2,000 fintech companies in India.

India’s financial technology industry has seen an explosive surge in financing over the last several years, with assets totaling more than $8 billion allegedly invested across various stages. India has the world’s highest FinTech rate of adoption. India has 10,200 registered fintech startups in 2024 and is one of the fastest-growing FinTech industries in the world. The Indian FinTech business is expected to be worth $150 billion by 2025.

While Payments and Alternative Finance accounted for more than 90% of investment flows in 2015, there has been a major change toward a more fair distribution of investment across sectors since then, with InsurTechs, WealthTechs, and other areas garnering considerable attention. In India, around 17 Fintechs have been designated as ‘Unicorns.’

Insurance companies throughout the world, particularly in India, have a lot of opportunities to use technology to optimize distribution costs and provide algorithms for personalized pricing. A believer of the same, Varun Dua, in the digital era, is commonly acclaimed for redesigning India’s insurance narrative.

“If you really want to change the plumbing, you will have to start manufacturing it,” is what he says. Varun Dua, the founder and CEO of Acko, is a renowned serial fintech entrepreneur. He co-founded and served as the CEO of one of India’s top online insurance aggregators, Coverfox, before launching Acko in 2016. Investors invested $30 million into Acko even before the formal debut, based on Varun’s proven records.

Varun Dua Biography

Name

Varun Dua

Birth

1981

Nationality

Indian

Occupation

Co-founder and CEO of Acko, Co-founder of Coverfox & Glitterbug Technologies

Acko’s Founder and Chief Executive Officer, Varun Dua, has over 10+ years of experience in the insurance market, with a wide spectrum of services and responsibilities. He was in charge of marketing analytics for direct business acquisition and technology for effective customer service. Coverfox Insurance Broking Pvt. Ltd. was his company, and he was its CEO and Co-founder.

He completed his Bachelor’s degree from the University of Mumbai. Later, he pursued a master’s at a prominent business school in India called MICA. Known for his extensive experience in product management and business development, Varun Dua’s educational background reflects a solid foundation for his professional journey.

Varun Dua – Family

Varun Dua’s father’s name is Chander Mohan Dua. His mother is Rashmi Dua and he is married to Sapna Rana.

Varun Dua – Career

Varun Dua, the founder of Coverfox, an online insurance aggregation platform, followed the road less traveled in a startup climate where the mantra is “act rapidly and damage things.”

Varun worked as a Trainee at Leo Burnett Advertising for less than a year after graduating. He subsequently went on to work for Tata AIG Life Insurance and Franklin Templeton Investments as a marketing manager. Varun launched two prior companies before founding Coverfox in 2013, Glitterbug Technologies and Enser Communications.

One of the key motivations for founding Acko, according to Dua, was the awareness that there had been an open chance to use the World Wide Web to bring interesting ways of selling insurance products.

Despite the fact that Dua had just come into contact with insurance by chance, he was rapidly pulled into its world and learned everything there was to know about the market’s intricate inner workings. It wasn’t long before he had the desire to start his own business.

In his own words, “I started off not really clear about what I wanted to do, but I definitely didn’t want to do what I was doing.”

The firm takes a D2C strategy, using its web platform to market traditional insurance services. This makes underwriting and risk selection substantially easier. Acko, his company, also offers unique and bite-sized insurance solutions, including rider insurance, ticket cancellation, mobile and appliance protection, and more, in addition to vehicle, bike, and health insurance. Acko also touts partnerships with more than 15 key digital ecosystem firms, including Ola, RedBus, OYO, Zomato, Urban Company, HDB Financial Services, and others.

Varun Dua on the Future of Insurance

Varun Dua – Acko

Varun Dua – Co-founder and CEO of Acko

Acko’s overall motto, according to its website, is “Insurance made easy: Zero commission. Zero paperwork.” Acko ran a campaign with the phrase “Full Paisa Wasool” to make people aware. The term “complete value for money” refers to insurance providing complete value.

Insurance schemes are how Acko makes money. Furthermore, Acko’s digital-only approach removes the retail costs of building physical storefronts as well as a parasitic reliance on a distribution network, both of which are factors that competing insurance firms rely on heavily.

Insurers, according to the owner of Acko Insurance, Dua, are obligated to hire salespeople to reach out to clients and market their goods because they all essentially provide the same or comparable products.

“Our focus on creating customised solutions will create the demand we are looking for, thus eliminating the need to hard-sell and invest a lot on a distributing network,” he adds.

Mumbai-based Acko, founded by Varun Dua, features a variety of customer-friendly programs. The organization has received several five-star ratings and over 4.5 crore satisfied customers as a result of its customer-centric initiatives.

Acko reported an operating revenue of INR 1,334 crore in FY22, which grew to INR 1,758 crore in FY23 and further increased to INR 2,106 crore in FY24. However, the company faced losses during these years. It recorded a loss of INR 482 crore in FY22, which widened to INR 738.5 crore in FY23 before improving slightly to INR 670 crore in FY24.

They deliver outstanding customer service, and as a result, Acko has gained their clients’ confidence. Narayan Murthy and Accel are also behind Acko’s amazing growth. Acko underwrote a premium of INR 41.56 crore in September 2019. In comparison to 2018, the firm had a 6x increase. The premium was previously valued at INR 6.53 crore.

Customers were unable to visit the showrooms because of the pandemic. Automobile purchases made through digital means, on the other side, have increased considerably. When compared with the year 2021, Acko, a digital insurance provider, saw a stunning 120 percent increase in sales of automotive insurance contracts in the first quarter of FY22.

Whether it’s for our vehicle, bike, or ourselves, pre-purchased insurance nearly always comes in useful, if not proving to be a lifesaver. Unfortunately, not all insurance service providers are glad to embrace a 0% fee and serve their customers online, but Acko is, which is why Acko is swiftly gaining steam.

Acko is here to provide premium insurance to the Indians. And moreover, the Mumbai-based Acko is now a unicorn. In the IPL 2022, Acko General Insurance signed on as an associate sponsor for three teams: Gujarat Titans, Kolkata Knight Riders, and Lucknow Supergiants. Two of these teams are new to IPL, having made their debut in the 15th edition.

Varun Dua has made 5 investments with the latest investment made in infinyte.club on August 12, 2024.

Date

Company

Round

Round Amount

Lead Investor

Aug 12, 2024

infinyte.club

Seed Round

INR 302 million

–

Jun 25, 2024

Plus Gold

Seed Round

$1.2 million

–

Sep 2, 2021

dezerv.

Seed Round

$7 million

–

May 23, 2017

Acko

Seed Round

$30 million

No

Feb 21, 2016

Charcoal Eats

Seed Round

$150K

No

Varun Dua – Challenges Faced

A basic challenge with his journey in the insurance sector, according to Dua, has been a lack of trust, which has created a big obstacle in his way in the beginning. Because of the complexities of the products on the market, the buying procedure, and the claiming process, the trust gap is exacerbated.

Customers have always found the insurance claims procedure to be a lengthy, time-consuming, and frequently iterative process. He wants to improve the consumer experience all the way through the value chain.

Varun Dua – Shark Tank India

Varun Dua – Shark Tank India

In more ways than one, the first season of the show, Shark Tank India has been a blessing to ambitious entrepreneurs in India. For watchers, it has been a huge hit! For openers, the show has brought those entrepreneurs a lot of attention, if not money.

The exposure, along with lucrative investments from the sharks, has paid off for some chosen ones. The Sharks’ banter, which is the most amusing segment for the desi population, helps to make the program what it is. It undoubtedly adds to the enthusiasm and provides some excellent items on Indian television. In the popular show’s third season, Varun Dua was one of the sharks at that time.

This is what he wrote on his X account:

To be a “shark” today for me is a strange feeling. I wasn’t born with a silver spoon. And with my average grades, I wasn’t what you’d call type A either. There was nothing in my resume, my repertoire or my background which should lead to the path of starting out a business, that should become large. And yet, here I am. My journey building @ACKOIndia has been anything but straightforward which is why being on Shar40k Tank is so meaningful. There is immense opportunity for young entrepreneurs in right now, as we are on the verge of a techtonic shift in India and India’s ambitions. I’m looking forward to contributing in this new ocean of opportunities with some awesome entrepreneurs.

Varun Dua is the founder and CEO of Acko Insurance.

What are Varun Dua education qualifications?

Varun Dua completed his Bachelor’s degree from the University of Mumbai. Later, he pursued a master’s at Mudra Institute of Communications (MICA), Ahmedabad.

Does Amazon own Acko?

Amazon is not Acko’s owner. While Amazon has been a major investor in Acko since 2018, contributing to its funding rounds, Acko remains an independent company with its own board of directors and management team.

What is Varun Dua net worth?

Varun Dua’s estimated net worth as of 2024 is INR 107 crore.

Who is Varun Dua wife?

Sapna Rana is the wife of Varun Dua.

What is Varun Dua age?

Varun Dua was born in 1981. He is 43 years old.

What is Acko net worth?

Acko’s valuation after its last funding round was $1.4 billion.

The super.money app, which is a credit-first UPI (Unified Payments Interface) payments gateway app developed by India’s eCommerce giant Flipkart, intends to rapidly transition into a secured lending role in the next months.

According to a press release issued by the fintech, the app had about one million downloads during the test phase, which resulted in more than ten million transactions. National Payments Corporation of India reports that monthly credit transactions on UPI exceed INR 10,000 crore.

As a First Offering, Super.money Offers a Rupay Credit Card

The RuPay credit card, which functions similarly to an interest-bearing wallet on the UPI platform, is the initial offering from super.money. Already, Super.money has released an additional product—unsecured personal loans—in partnership with leading banks in India.

“The retail credit industry is booming and offers a lot of potential,” according to Prakash Sikaria, founder and CEO of Super.money, who spoke with a prominent media outlet. “Secured credit products have not been developed further and have not experienced the proper level of adoption,” he opined.

According to Sikaria, the Tier II and III markets in India are where the credit on UPI opportunity lies. From the standpoint of the user, it presents a three- to fourfold potential compared to conventional credit cards. Specifically, he emphasised how the beta phase shaped the super.money experience and how they innovated at the forefront of UPI credit in a press statement.

However, Super.money will have to distinguish itself through its products rather than relying just on UPI-backed transaction volumes if it wants to stand out in the still-growing but highly competitive lending industry, which is dominated by banks and NBFCs.

Secured Vs Unsecured Loans

The fast growth of unsecured loans in India’s retail loans segment over the past two years has been brought to the attention of the Reserve Bank of India in both informal meetings with banks and the formal publishing of the Financial Stability Report, which is done half yearly.

The risks associated with certain categories of unsecured loans were given a higher weightage by the regulatory body in November of 2023. The intended outcome has already been achieved. Following the RBI’s action, the growth rate of credit card portfolios dropped from 30% to 23%. In a same vein, bank lending to NBFCs fell to 18% from 29% previously.

Secured loans (vehicle, home, loan against property) are safer bets than unsecured loans (personal loans, credit card loans, and other types of consumer durables and student education loans), which do not require collateral. Lending system vulnerabilities increase when combined with a regime of still-high interest rates.

Many fintech companies in India compete for customers in the secured lending market by offering digital loans collateralised by precious metals and fixed deposits. Banking institutions and non-bank financial companies (NBFCs) have a greater branch network and street fleet, allowing them to dominate other products like home and vehicle loans.

Sikaria has faith in the possibilities of the cosmos he intends to serve. According to his polls, a mere fifteen to twenty percent of individuals who apply for a credit card actually receive one. Financial product cross-selling is super.money’s goal in the unsecured lending market.

The plan is to attract and keep users with greater average revenue per user (ARPU) by offering them greater incentives. The goal for Super.money, similar to other fintechs, is to increase the percentage of users who purchase additional financial products through cross-selling.

2023 is a year that loan app companies and fintech companies may want to erase from their memory. Fraudulent loan app companies, extortion cases, and a rigorous crackdown by policymakers have meant that the whole cart is being painted black.

However, some loan app companies and fintech companies continue to pin their hopes on a better 2024 with consumer awareness programs, smarter risk-priced products, and collaborations to clean up the much-tarnished image of the sector.

Digitization has hit nearly every aspect of life, and credit availability is not very far behind. A report released by banking regulator Reserve Bank of India showed that loans disbursed by banks and non-banking finance companies through the digital mode multiplied 12 times between 2017 and 2020. With the rise in several disbursements, the grim underbelly of several loan app companies has also been exposed.

Earlier this month, Finance Minister Nirmala Seetharaman intimated the Lok Sabha, saying that between April 2021 and July 2022, Google Play had reviewed up to 4000 loan app companies and had removed more than 2500 loan apps from its Play store. Several debtors have been driven to death by extortion calls and threats, some even being sent morphed pictures of theirs, highlighting the dark side of loan app recovery agents.

However, some of the more reputed companies are trying their best to clean off this image of loan app companies.

“We continuously explain to our end consumers through online as well as offline mediums to not fall into offers that look very attractive or that are available through WhatsApp, SMS, and SMS calls,” said Rajesh Shet, founder of gold loan platform company Sahi Bandhu.

The regulators, too, are putting in all efforts to curb unsolicited apps. Recently, the Ministry of Information and Technology has asked the Reserve Bank of India to have more exhaustive Know-Your-Digital-Finance-App norms.

“This will ensure that only legitimate and scrutinized financial apps can access and use the Indian banking system, and further, if there is any violation of law, the KYDFA process will help in establishing the traceability and origin of the app for action under the law,” Minister for State for Electronics and Information Technology Rajeev Chandrasekhar told the news website Moneycontrol.com.

Risk-based Pricing

The issue of defaults within the loan app universe unravels a chicken-and-egg situation wherein companies are going overboard with selling products, thereby ending up sitting with bad loans on their books.

“Within the fintech industry, to increase the top line, some companies are trying to sell everything possible, even if customers are not looking for a loan or a credit card. They are trying to cross-sell and try to bring in lucrative deals or offers,” said Brijesh Chokhra, co-founder of the instant loan app company Wecredit.

Instant student loan app company Kuhoo Founder and Chief Executive Officer Prashant Bhonsle feels lending needs to be dealt with in a nuanced fashion to make it work for both the company and the customer.

“There are interpretations that a lender will have to do to fully understand, such as the income documents of the customer, the P&L, and the ITR. Some businesses you are evaluating are cash-flow businesses, and some are asset-heavy businesses. How do you interpret that information? And that interpretation is the secret sauce, which varies from lender to lender,” said Bhonsle.

Talking about Kuhoo’s focus area of student loans, the skill was to evaluate the potential of every student to get a job, Bhonsle said.

The regulators are, however, not taking any chances.

Recently, the RBI asked banks and non-banking finance companies to increase the risk weights on commercial loan exposure and credit card exposures to 125% from 100% earlier. Interestingly, several digital lending apps borrow from NBFCs too.

Rating agency ICRA recently observed in its press release that co-lending transactions by medium and small non-banking finance companies were “on the rise, largely seen in the unsecured loan segment, with the counterparty mostly being other NBFCs.”

Attributing to RBI data, Minister of State for Finance Bhagwat Karad said in the Lok Sabha earlier this month that NBFC’s share of credit to the industry was the highest at 12.83 lakh crore INR, registering a 12% rise year on year. This was followed by retail loans at 10.55 lakh crore INR, recording a near 26% rise on the year.

According to Bhonsle, appropriate “risk-based pricing” holds the key to a successful lending business.

“The Indian economy is growing rapidly, and with it, the demand for financial services. The coming years hold immense promise, and innovators across the world should explore these opportunities,” RBI’s Governor Shaktikanta Das said in a speech in September.

“Technological innovation has unprecedented potential to make finance more inclusive, competitive, and robust. It is crucial that technological advancements in the world of Fintech evolve in a responsible manner and are truly beneficial to the people at large. It is, therefore, vital for these innovations to be scalable and interoperable,” he added.

One of the ways to scale up operations for fintech companies would be through mergers, such as the one between the digital lending app Slice and North East Small Finance Bank in October. Touted as a breakthrough strategy to scale up, players are hoping for more such collaborations within the industry.

“I strongly believe that this industry will have to work closely and collaboratively, keeping common interests in mind. There will be competition, but there are common industry concerns and matters that require collaboration. And then, at some stage, there will not be enough room for many players. That’s when one will have to join hands and see who is good at what. Someone may be very good in tech, and someone may be very good in customer onboarding,” said Shet of Sahibandhu.

India’s growth prospects also hold promise as far as credit demand is concerned. Rating agency S&P revised its growth projection for India in 2023–24 to 6.4% from 6% earlier. For the next fiscal, however, it lowered its projection marginally to 6.4% from 6.9% earlier.

“India as an economy is doing so well, and this asset class (real estate) has shown returns year after year. I do see a lot of innovation on the FinTech side, particularly on the home loan side, because it seems like the norm of the regulators to allow the account aggregator framework to become more popular, which means that digital information will be a lot more freely available to many players who are part of the account aggregator framework,” said Pramod Kathuria, founder and CEO of AI-enabled fintech platform for home loans, Easiloans.

Conclusion

Fintech companies and digital lenders are hoping for a more responsible and cheerful 2024. While technological innovations unlock their potential further, the only thing that could put a spanner in their tracks would be unscrupulous lending by themselves.

Company Profile is an initiative by StartupTalky to publish verifiedinformation ondifferent startups and organizations.

In our haphazard daily life, we tend to get busy with several things and forget about payments and maintaining a log of all the financial transactions. This, sometimes, becomes extremely hectic and might even affect businesses adversely in a whole host of ways. However, with the emergence of numerous business management software, businesses and individuals can manage their businesses effortlessly. Khatabook is one of such reliable software solutions that makes managing business and personal ledgers a breeze!

Founded in 2018 in Bangalore, Khatabook is hailed as India’s fastest-growing SaaS company. Khatabook reminds you through WhatsApp or SMS when the money is due to be paid or collected. forgetting the due dates of payments to be made. Besides, handling multiple businesses will no more be a deal with Khatabook!

The micro, small and medium businesses of the country simply has a new name, Khatabook, which brings safe and secure business and financial solutions to increase efficiency and reduce costs.

Here’s diving into Khatabook’s journey in this StartupTalky article, where we will find out more about Khatabook Founders and Team, Funding and Investors, Startup Story, Tagline and Logo, Growth, Business and Revenue Model, Challenges, Competitors, Future Plans and more.

The latest campaign of Khatabook #DhandeKaDoctor featuring MS Dhoni, urging small businesses to use Khatabook to maintain their account.

Khatabook – Latest News

9th November 2021 – Khatabook has decided to shut down MyStore, the eCommerce enablement of the company, which has been a core product of the company, effective from 15th November onwards.

24th August 2021 – Khatabook concluded its Series C round of funding with a fundraise of $100 million led by Tribe Capital, Moore Strategic Ventures, Alkeon Capital, B Capital Group, Sequoia Capital, and more.

3rd February 2021 – Khatabook released its 2020 statistics. In 2020, Khatabook activated merchants in >95% Indian districts, recording over $100Bn+ in transactions with over 150Mn+ customers.

13th January 2021 – Out of the 7 Indian startups in Y Combinator‘s latest top companies’ list, Khatabook is one among them. India has emerged as an important market for Y Combinator.

Khatabook – About and How it Works?

Founded in January 2019, Khatabook is the fastest growing Saas company in India and one of the fastest-growing SaaS company in the world. It has become India’s leading business management app for MSMEs with 20M+ downloads in a remarkably short period of time. It operates the Android-based Khatabook app that enables companies to keep a digital log of their financial transactions and accept payments online.

Khatabook enables micro, small and medium merchants to track business transactions safely and securely. The app is available in over 12 vernacular languages, catering to a diverse audience in the country.

It helps businesses and individuals manage the business and personal ledgers on their phones and computer devices along with helping them recall the due dates with the help of effective SMS and WhatsApp reminders about the same. This Bangalore-based mobile app service shares WhatsApp and SMS reminders to users when the money is due to be paid or collected.

The Khatabook app has a free ‘Payment Reminders’ feature. With this feature, an automatic SMS is sent to your customers every time a transaction is recorded. Khatabook lets its users keep all details of credits and debits for any number of customers across multiple businesses ready and handy on their phones. Furthermore, Khatabook also helps its customers sync their transactions automatically, download, share and maintain reports of all the transactions, reap all the benefits of the effective QR code-based payments with 0% fees on transactions and more. In short, this app lets merchants do stress-free business.

Khatabook – Industry Details

Khatabook’s founder Ravish Naresh revealed on Twitter that Khatabook activated merchants in >95% Indian districts with 150Mn+ Customers. Based on the Indian MSME Data, Khatabook conducted research and analysis on the credit behavior of people across the country and also the impact of Covid-19 on small businesses.

Over 2020 @Khatabook activated merchants in >95% Indian districts, recording over $100Bn+ in transactions with over 150Mn+ customers. A good chunk of India's retail GDP is already being recorded on the platform and trade flows from across the country are getting digitized. pic.twitter.com/aVcZTlVBGM

Business volumes on credit are 45% higher for South Indian states vs the national average.

Credit given out by Khatabook merchants dropped by 40% in the initial Covid months. It has continued to recover to 80% of pre-pandemic levels by December.

Average days to recover debts increased by 25% during COVID for Khatabook Merchants.

Sectors like travel, construction, apparel were more impacted during 2020.

Khatabook – Founders and Team

Vaibhav Kalpe originally built Khatabook, which was later acquired by Kyte Technologies in 2018. Kalpe later joined the owning team of Kyte before he left the organization. The founding team of Khatabook currently has Ravish Naresh leading the company as the Co-founder and CEO along with other co-founders – Ashish Sonone, Dhanesh Kumar, and Jaideep Poonia.

Khatabook – Founders & Team

Ashish Sonone

The Co-founder of Khatabook, Ashish Sonone is a IIT Bombay Btech graduate in Computer Science. JetSynthesys Pvt. Ltd and Qiosk – News for Professionals were the companies where Sonone worked as a Software Engineer and Consultant respectively before co-founding Frodo and Kyte, in both of which he also served as a Backend Engineer. Khatabook is the third company that Sonone has co-founded.

Dhanesh Kumar

Another Computer Science and Engineering from IIT Bombay, Dhanesh Kumar started with Amazon as a Software Developer, who then realized his entrepreneurial and decided to co-found Knit Messaging, Kyte and now Khatabook, where he is still serving as a Co-founder.

Jaideep Poonia

Jaideep is an IIT Bombay alumnus from where he completed his Btech in Civil Engineering before completing S18 from Y-Combinator. Poonia has also been the co-founder of Knit Messaging, Kyte, and Khatabook as Dhanesh Kumar.

Ravish Naresh

Co-founder and CEO of Khatabook, Ravish Naresh completed his Btech from IIT Bombay, much like the other co-founders of the company, after which he co-founded Housing.com, where he also served as a COO. It was after leaving Housing.com, Ravish co-founded Khatabook, where he is still working as a CEO.

Khatabook currently works with around 300 employees.

Khatabook – Startup Story

The story goes back to 2016, when Ravish Naresh along with his team of college friends, started a digital spend manager app, Kyte.ai. The app helped users understand their expense patterns using their SMS alerts. Kyte initially had good traction but did not reach the expected growth scale. Also, the team realized all their users were based out of metropolitan cities.

On researching, they found that first-time online users did not deal with digital transactions, and they still rely on traditional khata or ledger books. As per Ravish, they wanted to build something that people want and then try to build a business around it.

That is when the idea for Khatabook developed, and they started to work on a simple cash management app, which they named Khatabook. The parent company of Khatabook is Kyte Technologies.

Khatabook – Mission and Vision

The mission statement of Khatabook says, “Empowering Udhari Khata (Book-Keeping)”.

“Started with a vision of transforming India’s small shops, today we are the biggest player in the small business segment digitizing a sector that forms the backbone of our economy. We are looking to work closely with the government and financial institutions to strengthen our market leadership and help MSMEs increase their income while making them more efficient and competitive,” said Ravish Naresh, CEO of Khatabook.

Khatabook – Tagline and Logo

The tagline of Khatabook is Business Hua Easy! The app lets every business go digital instead of following the same traditional method of book-keeping and making it easy to grow their business.

Khatabook’s logo itself signifies what the company is all about. It maintains a digital record of all the transactions we make, something which our actual ‘Khatabook’ (the diary in which we maintain our financial record) does.

Khatabook Logo

Khatabook – Business Model

Khatabook is a mobile app that helps small merchants to digitize their accounting and credit balance recording. It helps to reduce the burden of bookkeeping and accounting. It is just like having a khata in your pocket. The business model of Khatabook is making “Bharat” / India come online.

It is 100% free to use and secure for all types of businesses with which shop owners can record credit (Jama) and debit (Udhaar) of customers. But Khatabook has no revenue source at present.

Ravish Naresh, CEO of Khatabook, said they’re now developing the app to provide a complete financial solution for small businesses. The startup has plans to bring a host of new features onto the platform and UPI payment is next on the line.

Khatabook has seen some growth in the past two and a half years, where it has emerged as an integral part of the MSME community in almost every district in India. A majority of the merchant users on the Khatabook platform have embraced the digital practices dumping their offline business practices.

Furthermore, Khatabook has also introduced 3 other solutions apart from the Flagship Khatabook for the benefit of the MSMEs:

Biz Analyst – This is a leading SaaS business management solution from Khatabook designed to offer premium value-added on-demand services like sales and purchase reports, livestock updates, and other MIS reports. Biz Analyst can be integrated with Tally ERP9 and allows an overall view of the business operations.

Pagarkhata – This is a staff management platform for businesses by Khatabook which aims to help merchants to turn the staff attendance, payroll/wages, attendance updates, leaves, payments, and other processes digital.

Cashbook – Cashbook is another platform by Khatabook built as a cash handling and tracking solution. Furthermore, it also helps with cash sales and expense management.

In 2020, Khatabook has active merchants in 95% of Indian districts, recording over $100 Billion in transactions with over 150 million customers.

Khatabook has recorded total revenue of Rs 17 crore during FY21, thereby registering a 25.3% decline from Rs 24.4 crore. The startup’s revenue from operations, currently recorded at Rs 16.9 crore, witnessed a dip of around 30.7% from Rs 24.4 crore that it posted in FY20. On the other hand, the other income of the startup rose from Rs 12.7 crore in FY20 to Rs 21 crore in FY21.

Diving into the profit-loss segment, it has been discovered that Khatabook has managed to reduce its loss by 63%, which has been brought down from Rs 89.5 crore to Rs 33 crore. This is primarily due to the selling of its intellectual property, some of which it sold to its holding company, Kyte Technologies Inc. for around Rs 57 crore.

In FY22, the company experienced significant growth in its operating revenue, surging from Rs 17 crore in 2021 to an impressive Rs 71 crore. However, this growth was accompanied by a corresponding increase in total expenses, which escalated from Rs 109 crore in FY21 to Rs 189 crore in FY22. Consequently, the company’s losses also saw a substantial rise, soaring from Rs 33 crore in FY21 to Rs 111 crore in FY22 during this period.

Here’s a look at the financials of Khatabook:

Khatabook Financials

Operating revenue for the Khatabook increased by 14% in FY23 to Rs 81 crore. Conversely, there was a marginal rise in losses of 4% to Rs 125 crore. Due to increased employee benefit costs (wages, salaries, PPF, etc.), which amounted to over Rs 142 crore, the company’s total expenses stayed steady at Rs 223 crore, a slight increase from Rs 189 crore in the year FY22.

Khatabook – Growth

Khatabook has registered around 10 Million monthly active users and the numbers are growing.

Growth had an excellent trajectory, which did take a hit during the lockdown in line with other external factors. With the relaxation of the lockdown, the company started reviving the business at a steady pace. The revival has been faster with users in tier-2 and tier-3 cities of India.

As a very relevant offering for merchants in the pandemic, the company also launched the MyStore app to enable them to take their stores online in 15 seconds and continue doing business through their preferred communication channels.

Within a month after the launch, more than 2.5 million merchants across India have installed MyStore. Khatabook also initiated work from home active, 24/7 call center support for merchants. Currently, the revenue model of Khatabook depends on its funding.

Some key growth highlights would include:

5 crore+ registered businesses

A spread over 4000+ cities of India

Powered by popular investors like Sequoia Capital, DST Global Partners, Y Combinator, Tencent, B Capital Group and more

Khatabook – Acquisitions

Khatabook has acquired Biz Analyst on March 25, 2021, which remains the company’s maiden acquisition.

Khatabook – Awards and Achievements

Some of the popular awards and achievements that Khatabook has seen so far are:

It was declared as the Winner of Nasscom League of 10 in the Emerge50 Awards 2020

The company’s app won the Best Innovative Mobile App award at IAMAI 2020

mCube announced Khatabook the winner of the Best Content in a Mobile Marketing Campaign in its awards ceremony in 2020

Khatabook – Partnerships

Khatabook currently partners with the former skipper of the India cricket team, M.S. Dhoni, who is an investor as well as the brand ambassador of the company. The strategic partnership was announced on March 17, 2020.

Khatabook – Challenges Faced

Khatabook also faced a shortage of money during its initial days just like other new startups. Ravish, the CEO of Khatabook realized that they need to look into serious funding options.

In the series A phase, they were struggling a bit with the funding. The growth hit them fast, so the seed round took place in 5 bridges. It was the highest in the history of funding for Sequoia.

“Well, the struggles were mainly money-related. We knew we were working on something important and kept going with it. Often it was difficult to imagine the future of our initiatives with no funding, but perseverance is what got us where we are today,” said Ravish Naresh.

He also said that the adoption of their product was not only dependent on the app’s visibility and convenience but also on educating users, not just for the app but also for using digital technology in general. The biggest hurdle was to persuade offline shopkeepers to come online and train them for digital transactions.

Switching away from the convention is understandably tricky and daunting for merchants who mainly have offline workflows. Persuading traditional enterprises to embrace the digital still remains a crucial challenge for them.

“It is important to build something that people want and then try to build a business around it, and that is exactly what the team did.” said Ravish.

Khatabook announced the shutdown of MyStore on November 10, 2021. The eCommerce enablement product was one of the core products of the company, which also contributed to the expansion of the company by raising funds along with helping the company with its bookkeeping requirements.

“Thank you for being a part of the MyStore journey. We are planning on discontinuing the MyStore App. Your MyStore App won’t work from 15 November 2021,” goes a blog post from the company.

The company has further asked its users to download their invoices by sharing order invoices before doing away with the app.

Khatabook had previously been dragged into a legal fight with its rival, Dukaan over the plagiarism of the name when MyStore was named ‘Dukaan by Khatabook’, in August 2020. Khatabook later decided to change it to ‘MyStore by Khatabook after a legal battle of around four months. The tagline of the app, however, remains the same, ”Create Your Online Dukaan in 15 Seconds” to date on Play Store.

Khatabook – Funding and Investors

Khatabook has raised a total of $186.5M in funding over 4 rounds. Their latest funding was raised on 24th August 2021, from a Series C round. Khatabook is funded by 34 investors in total. Tribe Capital and Moore Strategic Ventures are the most recent investors. The valuation of Khatabook was estimated to be around $600 Million in August 2021.

In a strategic move aimed at optimizing costs and prolonging the company’s financial runway, the organization recently made the difficult decision to implement workforce reductions, resulting in the departure of over 40 employees from various departments. These actions were undertaken as part of a broader effort to navigate the challenges faced by growth-stage companies.

While undoubtedly a tough choice, the company’s leadership recognized the importance of preserving its financial stability and ensuring a sustainable future. This move reflects a commitment to adaptability and resilience in an ever-evolving business landscape, with the hope that these measures will ultimately position the company for long-term success.

“Khatabook has laid off 42 employees across sales, marketing and analytics, and technology verticals,” said one of the sources requesting anonymity. “People who lost their jobs in the exercise have been given standard severance packages including 3 months salary among others.”

Khatabook – Future Plans

Khatabook plans to expand and achieve two to three times business growth by simplifying the traditional way of doing business. Remaining committed to India’s MSME segment, Khatabook will be adding services to streamline and simplify business processes for the merchants.

“Committing to a goal is essential for business directions and decisions. One thing that pandemic has taught us is that we need to think through the most unlikely scenario and make sure we are relevant in all possible scenarios or are agile enough to change our direction as per the need of the hour,” says Ravish.

Khatabook has already managed to build a widely accepted tech ecosystem for the MSMEs across the country and will now concentrate on the disbursement of financial services through its tech platforms. These financial services will further enable smooth lending, payment, and deposits in the MSME space.

Khatabook is eyeing the right partnership opportunities to seamlessly roll out the solutions that would benefit the economic aspirations of countless small businesses.

Khatabook has announced a buyback scheme of ESOPs worth USD 10 Million in order to acknowledge the contributions of its employees, the ex-employees and the early investors who stayed by the company and helped it grow. The employees who are eligible for the ESOP scheme would be able to sell up to 30% of their vested options. Meanwhile, Khatabook has also expanded its ESOP pool to $50 Mn.

Furthermore, Khatabook is also looking to strengthen its talent base by hiring employees for the engineering, product, design, analytics, and data science departments.

Khatabook – FAQs

What is Khatabook?

Khatabook is the world’s fastest-growing SaaS company. It is India’s leading business management app for MSMEs that enables companies to keep a digital log of their financial transactions and accept payments online. It’s like having a khata in your pocket.

Is Khatabook an Indian app?

Yes, Khatabook is an Indian app founded in 2019 with an aim to reduce the burden of bookkeeping and accounting.

Which company owns Khatabook?

Kyte Technologies is the Parent Company of Khatabook.

Who is the CEO of Khatabook?

Ravish Naresh is the CEO and Co-founder of Khatabook.

Who are the founders of Khatabook?

Khatabook was founded by Ashish Sonone, Dhanesh Kumar, Vaibhav Kalpe (Ex-Khatabook), Jaideep Poonia and Ravish Naresh in 2019.

How does Khatabook make money?

The Khatabook revenue model is non-existent at the moment. Naresh says their focus is now on developing the app to provide a complete financial solution to small businesses.

What is the use of Khatabook?

Khatabook app enables MSMEs to keep a digital log of their financial transactions and accept payments online.

What is the valuation of Khatabook?

The valuation of Khatabook was estimated to be around $600 Million.

Company Profile is an initiative by StartupTalky to publish verified information on different startups and organizations.

Indians are slowly and steadily considering Cryptocurrency as a safe mode of investment. Mostly the younger generation is taking interest in Cryptos. According to some reports, the average age of crypto investors in India is around 24 years. However, there are still many speculations about crypto trading and many investors are not comfortable with Crypto trading still. This is why the Bangalore-based startup, CoinSwitch Kuber was formed in 2017 to make crypto trading simpler for Indian Investors.

The startup enables trading in several cryptocurrencies, including Bitcoin, Ripple, Ethereum, Litecoin, Dash, and many others, using INR. You just need to download the CoinSwitch Kuber iOS or android app and start trading. In this StartupTalky article, we are exploring more about CoinSwitch Kuber, the story behind the startup, and what the startup is offering, which includes CoinSwitch Kuber website, CoinSwitch Kuber reviews, CoinSwitch Kuber deposit, CoinSwitch Kuber investors, CoinSwitch Kuber login, CoinSwitch Kuber fees, and how it is growing!

CoinSwitch Kuber is a cryptocurrency trading platform that aims to simplify investing in cryptocurrencies. CoinSwitch Kuber aggregates liquidity across major Indian and global crypto exchanges. The platform’s order matching engine provides the traders the best rates at the click of a button, thus making trading simpler than ever.

“We discovered that the price of crypto swings between exchanges based on supply and demand when trading in crypto ourselves. Choosing the correct exchange is crucial if you want to obtain greater profits from the market. “We created an aggregator of various exchanges that offered us real-time data on which exchange is the best to trade at any particular instant to obtain the highest return,” co-founder Ashish says explaining the idea behind the startup

CoinSwitch Kuber lets users trade across 100+ cryptocurrencies. Users can buy cryptocurrency using a credit or debit card at competitive prices on the CoinSwitch platform. After completing the KYC/AML processes, customers may use the pooled liquidity of India’s top exchanges to receive the best rate and trade instantly.

The CoinSwitch Kuber mobile app comes with a simple user interface that makes crypto trading a breeze.

While customers from over 200 locations in India invest in crypto through its platform, tier I cities account for 40% of its users, while tier II (36%) and tier III (24%) make up the majority of its clientele. On CoinSwitch, the average ticket size per user is 9,000 per month, however, this varies by city. The average ticket size in Tier I is Rs 11,600, compared to Rs 6,600 in tier II and Rs 3,500 in tier III.

What’s interesting or concerning, depending on one’s perspective, is that the average age of a crypto investor on CoinSwitch is 24 years, and Singhal claims that crypto is the first investment in any asset class for 65% of his customers outside of savings bank accounts and fixed deposits!

CoinSwitch Kuber’s tagline says, “Buy, Sell, Trade.” CoinSwitch Kuber has launched a new campaign with the catchphrase “Trade Kar, Befikar.”

CoinSwitch Kuber – Founders and Team

CoinSwitch Kuber was founded by Vimal Sagar Tiwari, Govind Soni, and Ashish Singhal in 2017.

Founders of CoinSwitch Kuber

Ashish Singhal

Ashish Singhal is the Co-founder and CEO of CoinSwitch Kuber. Former Amazon employee who interned at Microsoft, Ashish Singhal, is a computer science graduate from Delhi’s Netaji Subhas Institute of Technology. Besides handling various technical roles in companies like Livspace.com and Reap Benefit, Ashish founded startups like CRUXPay (an open-source protocol for blockchain naming services) and Urban Tailor, which is the first of its kind at home tailoring services. He left the position at Urban Tailor in September 2016, but continued with CRUXPay, before stepping down from that too in April 2020.

Govind Soni

CoinSwitch Kuber Co-founder and CTO,Govind Soni was also a former Amazon and Livspace employee. Besides CoinSwitch Kuber, Govind co-founded CRUXPay along with Ashish and Vimal. Soni was also a student of the same college as Ashish, where he studied Computer Engineering, and served as the Co-founder and CTO also at CRUXPay, before stepping down from it in January 2021.

Vimal Sagar Tiwari

CoinSwitch’s Co-Founder and Chief Operating Officer (COO), Vimal Sagar, worked with organizations like Zynga and Accenture. He graduated from the Jaypee University of Information Technology. Vimal is also a Co-founder of CRUXPay, and is still retaining the positions of Co-founder and COO at CRUXPay.

The CFO, CBO, and SVP quit their roles to start up a new initiative that will offer insights to web3 investors. Sarmad Nazki, Sharan Nair, and Krishna Hegde of CoinSwitch Kuber haven’t finalised the name of the startup yet, as per news dated July 8, 2022. Nazki has served in the position for a little more than a year. Nair joined CoinSwitch Kuber just after the company was launched in 2017, and held numerous positions during his long stint, whereas Hegde joined the unicorn crypto company in September 2021. CoinSwitch Kuber confirmed that the positions of CFO, CBO, and SVP will be taken up by Ramesh Bafna, Rishav Dev, and R Ventakesh. The trio has already been talking to Web3 focused-investors to raise a seed round ahead.

The CoinSwitch Kuber team has an employee count that somewhere ranges between 501-1000, as per its Linkedin profile.

The origin of CoinSwitch Kuber can be traced to the realisation of Govind, Vimal and Ashish, all of whom were computer engineers and friends, when they discovered that the price of cryptocurrency is dynamic. It varied slightly across all the prominent crypto exchanges, based on the demand and supply. Therefore, they thought that if the users wanted to get better returns from the market, especially when it comes to scale, they needed to choose a good cryptocurrency exchange. This is what made them decide to create an aggregator of crypto exchanges. Here, their main aim was to provide real-time data on the best prices and exchanges for cryptocurrencies to be traded.

Ashish, Govind, and Vimal, who are all in their early thirties, have been friends since their college days when Ashish and Govind were batchmates, and Vimal was a mutual friend of theirs. They were also tech whizzes who competed in hackathons as a group. Almost every big hackathon in India was won by the trio, including the ones organised by Sequoia, Google, Amazon, and LinkedIn. Surprisingly, CoinSwitch was inspired by a hack that the trio subsequently made public.

On one occasion, the founders-to-be of CoinSwitch created a simple crypto exchange aggregator in a hackathon, but little did they know that the hack would later turn into a full-fledged company.

CoinSwitch Kuber was founded in 2017, and as soon as it launched, the startup started to take users on board at a rapid scale. The users “needed simplicity in the crypto world”, said Ashish, and this made the simple and intuitive nature of the product work. The only goal that the founders of CoinSwitch had while working on the product was to make crypto easy to understand and accessible to the masses.

However, soon after CoinSwitch was launched as a product, RBI’s announcement came, where the body signaled a ban on the cryptos by asking the banks to refrain from supporting these currencies in 2018. This made the founders take their product, which was then simply known as “CoinSwitch”, to the global market.

Eventually, Sequoia Capital backed their venture, thereby making the CoinSwitch foray into success. Though the platform turned successful indeed outside of India, the hearts of the CoinSwitch founders were set only on their country.

This turned real when Supreme Court intervened, overruling the previous RBI ban, thereby making it an open season for the crypto-based businesses like WazirX, ZebPay, CoinSwitch and more. This was more than a silver lining for them. They soon launched CoinSwitch Kuber app just for the Indian market.

CoinSwitch Kuber – Mission and Vision

The CoinSwitch Kuber team believes in financial inclusion, which means that wealth, investment, and financial education should be accessible to all people.

CoinSwitch Kuber’s mission statement says, “Our Mission is to challenge the status quo. We believe that our platform democratizes cryptocurrency investment so the everyday man can make his money work for him – without a fancy degree or a boatload of money.”

The company’s vision is to make crypto trading simple and transparent.

CoinSwitch Kuber – Partnerships

NDTV and CoinSwitch Kuber have established a strategic collaboration to provide comprehensive and best-in-class cryptocurrency programming in August 2021. NDTV will create unique crypto destinations on gadgets360.com, ndtvprofit.com, and ndtvindia.in as part of this relationship. This bridge expansion includes a refreshing show on NDTV 24X7 and NDTV India every other weekend.

The need for trustworthy and accurate information is more important than ever as cryptocurrencies become more mainstream and more individuals begin to evaluate this asset class. With NDTV’s credibility and confidence, as well as CoinSwitch Kuber’s subject expertise and powerful trading platform, this collaboration aims to bridge that gap.

CoinSwitch Kuber Partners with Startup Karnataka for Blockchain Hackathon

The Blockchain Hackathon, Building Future Cities, an initiative decided by Startup Karnataka of Karnataka government, and Tejasvi Surya, Bengaluru South MP, will also have CoinSwitch as its partner. This initiative is aimed to recognize blockchain-based solutions and bring them to the citizens from across the country, in order to dissolve the everyday problems they face. Sequoia India will also be backing this hackathon.

CoinSwitch Kuber – Business Model and Revenue Model

CoinSwitch Kuber is one of just a few cryptocurrency companies currently functioning. Users may acquire shards of various major cryptocurrencies on the crypto market. On CoinSwitch, for example, a user may buy bitcoin and other currencies in tiny sachets for as little as 100 Indian rupees ($1.30), which proves really profitable for the users. Besides, where other crypto exchanges came up with products for the traders who are acquainted with the order books, and are well-versed with buying/selling orders, CoinSwitch distinguished itself by targeting the users who hadn’t see an order book before, and wasn’t aware of what it was.

CoinSwitch Kuber presents itself as an aggregator and don’t charge the users, in contradiction to other crypto exchanges, which usually charge transaction fees from the users. CoinSwitch Kuber, instead, of a maker, negotiates with the crypto exchanges on transaction fees.

Speaking on the business and revenue model of CoinSwitch Kuber, Founder and CEO, Ashish Singhal said, “We give a fixed price to users and aggregate supply on the backend, Our execution engine is where the revenue comes from. But going forward, earning models may evolve as innovations and regulations come into play.”

CoinSwitch Kuber offers its users free trading, deposit, and withdrawal facilities for the first 100 days. After that, a fee is charged on each transaction made through the platform. As per the terms of the company, there is no fee for the transfer of digital assets to the CoinSwitch Kuber wallet, however, withdrawal of digital assets from the wallet may attract charges. The platform also charges for the transfer of fiat currency through credit/debit cards or net banking.

CoinSwitch Kuber – Growth and Revenue

CoinSwitch Kuber has managed to impress investors with its concept and performance. In addition to Tiger Global Management’s $25 million investment in April 2021, Sequoia Capital, Ribbit Capital, Paradigm, Kunal Shah, the creator of Cred, and others have backed CoinSwitch. With the recent fundingreceived from Andreessen Horowitz and Coinbase Ventures in October 2021, CoinSwitch Kuber reached Unicorn status with a valuation of $1.9 billion.

CoinSwitch Kuber boasts of witnessing the highest number of downloads among the crypto startups in India in 2021 when it was downloaded more than 6.1 mn times.

CoinSwitch Kuber is the most downloaded crypto exchange app in 2021downloaded

Ever since CoinSwitch was started and was taken global after the RBI ban, the company started seeing huge transactions through their app. Within just 2 years, CoinSwitch Kuber has seen more users onboard its app than any other crypto exchange in India. This growth has been mainly due to the simplified UX that the app brought in, and its decision to not provide the users with certain trading features.

Singhal points out that unlike other startups they did not knock on the investors’ doors.

“We did not reach out to Tiger Global for funding. They contacted us and expressed their willingness to invest in our company. Tiger doesn’t invest less than $100 million but we said we just need $25 million,” says Singhal.

Kuber claims to have over 15 million users in India, and the monthly active user count of CoinSwitch Kuber is over 7 million. It has also been disclosed that more than half of them are under the age of 25. CoinSwitch Kuber claims to have handled $5 billion in transactions in the last 11 months.

The firm intends to expand its operations outside cryptocurrency in the future.

“We intend to expand into traditional finance, such as equities, mutual funds, exchange-traded funds, and bonds, and provide a full portfolio on our platform to retail customers,” says the company.

“We are not a capex-intensive business, and don’t need too much money. Hence, our EBITDA margins are in the range of 60-65%,” reveals Singhal.

CoinSwitch Rolls Out the Web3 Discovery Fund

CoinSwitch has launched the Web3 Discovery Fund, which is a fund that will invest in and help incubate early-stage startups that are engaged in building blockchain solutions for the Web3 space. This Web3 startups funding initiative of CoinSwitch is currently aiming to help up to 100 Indian startups, as per the reports dated August 10, 2022. Ashish Singhal, the CoinSwitch Co-founder and CEO stated that the fund has already received an initial corpus of $10 mn and the company is further looking to raise some more funds from marquee investor partners ahead.

CoinSwitch: some of the major growth highlights are:

It has over 2 crore+ users as of February 2024

It is backed by some of the world’s leading investors including a16z, Tiger Global and Sequoia Capital India.

On November 22, 2023, CoinSwitch launched the multiexchange trading platform CoinSwitch Pro on November 22, 2023. This platform marks a significant advancement for cryptocurrency enthusiasts and traders. This cutting-edge platform not only provides users with a comprehensive view of multiple tokens across various exchanges but also empowers them to make informed decisions by comparing prices and selecting the most suitable options.

What sets this platform apart is its seamless functionality, allowing users to effortlessly trade crypto assets in INR across a multitude of exchanges, all through a single login. This streamlining of the trading process not only enhances the user experience but also signifies a pivotal step towards greater accessibility and user-friendliness within the cryptocurrency realm.

There is a variable transaction charge associated with using the cross-exchange platform, depending on the crypto exchange that is used. The CoinSwitch Pro platform stands out for its flexibility in serving various users and exchangers.

CoinSwitch Kuber – Funding and Investors

CoinSwitch Kuber has raised over $300 mn over 4 funding rounds. It is now counted among the unicorn startups of India, with a valuation of over $1.9 bn.

Date

Round

Amount

Lead Investors

October 6, 2021

Series C

$260M

Andreessen Horowitz, Coinbase Ventures

Apr 22, 2021

Series B

$22.7M

Tiger Global Management

Jan 13, 2021

Series A

$15M

Paradigm, Ribbit Capital

Mar 24, 2018

Seed Round

$1.5M

–

Andreessen Horowitz is a CoinSwitch Kuber investor, who invested for the first time ever in India in the $260 mn funding round of CoinSwitch, and was joined by Coinbase Inc., which turned CoinSwitch into a unicorn. Some other investors of CoinSwitch are Tiger Global, Paradigm, Ribbit Capital etc.

CoinSwitch Kuber – ESOPs

CoinSwitch Kuber recorded their first-ever ESOP buyback programme on March 21, 2022, worth $2.5 million. This buyback round was a mixture of funding that came from both the internal and external sources.

CoinSwitch Kuber – LayOffs

CoinSwitch in a recent move, has undertaken a strategic restructuring initiative, resulting in the reduction of its workforce by 8%. This decision translated to approximately 44 employees being laid off from various departments. Presently, CoinSwitch boasts a total workforce of 519 employees, as per their LinkedIn profile.

The impact of these layoffs has predominantly been felt within the customer support team, where the majority of the affected employees were stationed. While such decisions are often undertaken as part of broader efforts to optimize and realign company resources, they undoubtedly bring about significant transitions for both the organization and the employees involved.

In the official statement company spokesperson said, “we right-sized our customer support team to align with the present volume of customer queries on our platform. This impacted the roles of 44 members of our customer support team, who voluntarily resigned from their roles after a detailed discussion with their managers earlier this month.”

CoinSwitch Kuber – Competitors

To mention, the top 10 competitors of CoinSwitch Kuber are:

CoinSwitch Kuber employs over 120 people and has over 4.5 million users on its network. In comparison to other applications on the market, the app provides consumers with a clean UI and UX design. However, it was recently discovered that the app does not support UPI payments.

On April 21, 2021, the organization announced on all of its official social media accounts that INR deposits in the CoinSwitch Kuber App will be disabled. CoinSwitch Kuber said on Twitter that the firm has temporarily blocked all INR deposits owing to unforeseen problems with their banking partner. The issue was later resolved and now INR deposits are enabled.

Cryptocurrency is a murky area in India. Despite the legalization of crypto investments in India, there are many fears and doubts related to the topic. When it comes to difficulties, Ashish believes the company’s sole issue is teaching people in India about cryptocurrencies and the ecosystem.

CoinSwitch Kuber had got into trouble in association with the idea of lending feature with the SEC, and as a result, Ashish had to drop the idea. However, the founders still are of the opinion that they would be able to use the lending and stakes feature to utilise them for earning revenues in the future. They have already started working to make it possible by working with regulators and gaining their confidence.

As the trading of cryptocurrency lacks defined regulations, CoinSwitch Kuber temporarily paused crypto withdrawals.

CoinSwitch Received ED Notice in Association with FEMA investigation

CoinSwitch reportedly received a notice from the Enforcement Directorate (ED) along with some other cryptocurrency firms like CoinDCX in association with the Foreign Exchange Management Act (FEMA) investigation. Here, ED is determining whether or not these companies were engaged in offences related to foreign currencies. On this, CoinSwitch mentioned that it has received notifications from ED and is ready to comply with them, as per reports dated July 12, 2022.

CoinSwitch Kuber – Future Plans

CoinSwitch has revealed plans to build a cryptocurrency investment platform by June 2024 that is targeted at retail investors as per news report of March 11, 2024. Through the provision of user-centric technology, this program seeks to democratize access to digital asset trading and enable users to navigate investments with confidence.

FAQs

What does CoinSwitch Kuber do?

CoinSwitch Kuber is a crypto trading platform for individual investors that is available only in the Indian market via a mobile application. It enables trading in several cryptocurrencies, including Bitcoin, Ripple, Ethereum, Litecoin, Dash, and many others, using INR and is available as a mobile application (INR).

Unocoin, WazirX, CoinDCX, Instamojo, Glidera, ZebPay, SmartCoin, IPaxful, Bitxoxo Bitcoins, and Coinbase are the top ten competitors of CoinSwitch Kuber.

When was CoinSwitch Kuber founded?

CoinSwitch Kuber was founded in 2017.

Who founded CoinSwitch Kuber?

CoinSwitch Kuber was founded by Vimal Sagar Tiwari, Govind Soni, and Ashish Singhal in 2017.

What is the CoinSwitch Kuber website?

The CoinSwitch Kuber website is coinswitch.co

What are the CoinSwitch Kuber fees?

CoinSwitch Kuber doesn’t ask the users anything such as the CoinSwitch Kuber fees. It rather poses itself as an aggregator and negotiates with the crypto exchanges on transaction fees.

How is CoinSwitch Kuber login done?

The CoinSwitch Kuber login procedure is really easy where the users need to download the app of the company and then they need to first have an account to log in to the same, with the same login credentials.

What are CoinSwitch investors?

Some of the prominent CoinSwitch investors are Ribbit Capital, Andreessen Horowitz, Tiger Global, Coinbase Inc., Sequoia, Paradigm and others.

What was the CoinSwitch deposit issue?

CoinSwitch deposit of rupees was temporarily disabled, but it was fixed after 2 long weeks.

What is wrong with CoinSwitch Kuber withdrawals?

When it comes to CoinSwitch Kuber withdrawals, the company has announced that it has temporarily disabled the withdrawal of cryptocurrencies.

Company Profile is an initiative by StartupTalky to publish verified information on different startups and organizations. The content in this post has been approved by Credgenics.

In India, where the credit demand of more than $600 Billion is being met through informal sources, digital lending is set to cross the $100 Billion mark by the end of 2023. Credgenics is a part of the financial industry, especially the lending and debt recovery ecosystem. Anand Agrawal, Mayank Khera, and Rishabh Goel founded Credgenics in 2018.

The SaaS-enabled debt recovery platformofCredgenics was designed to help lessen the burden of the lenders (banks, NBFCs, FinTech) through better data management and ensuring lesser cost and time consumption in the recovery process. At present, over 50 lenders are using the platform, which includes 07 banks with notable names like ICICI, Axis, and HDFC and more than 40 NBFCs, such as LoanTap, Drip Capital, and Udaan, among others. In the last three years, Credgenics has managed to grow MoM by 80–100%.

StartupTalky interviewed Mr. Rishabh Goel, Co-founder & CEO of Credgenics to learn the Startup Story and the roadmap of Credgenics. He also gave insights on the business model, when it originated, funding, growth hacks, working model, and expansion plans.

At Credgenics, the core product is the SaaS platform that comes armed with two unique offerings, the Automated Communication and Digital Legal Notice Module. Its SaaS-enabled debt recovery platform was designed to help lessen the burden of lenders (banks, NBFCs, FinTech) through better data management and ensuring lesser cost and time consumption in the recovery process. The legal module simplifies the entire journey of issuing a legal notice to the borrowers, sending a soft copy via digital channels (SMS, email, and WhatsApp) and physical modes (via courier partners).

Credgenics offers the creditors two solutions —

Where the creditor can purchase its software and undertake the rest of the process, and

The end-to-end recovery where the entire process from data management to Online Dispute Resolution and litigation processes undertaken by Credgenics’ designated teams.

The process entails uploading the data on the platform, generating actions using an automated rule-defining widget, issuing notices, and then approaching borrowers using any of the five modules, such as cloud-based calling, automated communication, and field executive being tracked by the Android app for on-field collection, legal notice, and litigation workflows. Thus, the Credgenics platform becomes a one-stop solution for creditors and their debt recovery woes. Within just a couple of months from its inception, Credgenics could demonstrate a strong product market fit.

Credgenics

Credgenics’ long-term focus is also to strengthen and build further from its present position, which includes equipping itself with a better-enabled team, to growing operations and business by expanding in multiple lending products, apart from the collection angle alone. The plans are also to continue researching and upgrading Credgenics platform features, offerings, and market presence because technology and legal, fields require a constant upgrade. Research and strengthening the core also becomes vital as the judicial and fiscal regulations in the target geographies have to be thoroughly studied, followed by the design and implementation of the Credgenics platform and offerings.

“Our core belief is based on the principle of ethically resolving the bad debt crisis that the economies are dealing with,” says Rishabh Goel, Co-founder & CEO, of Credgenics.

Credgenics is a part of the financial industry, especially the lending and debt recovery ecosystem.

The Debt Recovery Market is expected to grow at a significant pace. The Debt Recovery market provides the various factors that form an important element of the market. It includes the definition and the scope of the market with a detailed explanation of the market drivers, opportunities, restraints, and threats. India has the worst bad-loan ratio after Italy among the world’s 20 largest economies.