To broaden its fintech products under Zoho Payments, SaaS startup Zoho has introduced its line of point-of-sale (POS) devices, which includes an all-in-one POS device, smart POS device, and static QR with soundbox. Sridhar Vembu, a co-founder of Zoho, made the announcement on X.

In order to tackle “real business challenges and strengthen India’s digital payments infrastructure”, Zoho has also teamed up with NPCI Bharat BillPay Ltd (NBBL), a subsidiary of the National Payments Corporation of India (NPCI), Vembu continued. According to Vembu, the business is also working on integrating Zoho Pay with Arattai, its instant messaging app, so that payments may be made through the app.

Zoho Also Announces Pool of Payment Solutions

On the outskirts of today’s ongoing “Global Fintech Fest 2025” in Mumbai, Zoho also announced the availability of a variety of payment options, including payout capabilities, virtual accounts for collections, and marketplace settlements.

According to a statement from the firm, Zoho Payments now facilitates payouts, allowing companies who use Zoho Payroll to automate employee payroll procedures and make salary disbursements. Companies have a more dependable method of transferring money, can track payments made, and can pay salaries from any bank account with ease.

In February of last year, Zoho was granted final permission for a payment aggregator licence. After then, the business launched Zoho Payments, marking its entry into the payments market. At the time, Zoho said that companies could simplify their payment procedures by integrating Zoho Payments with its financial and operations apps, such as Zoho Books, Zoho Invoice, and Zoho Billing.

Zoho Strongly Backed by the Indian Government

The recent product introductions by Zoho coincide with a renewed interest in goods manufactured in India. Ashwini Vaishnaw, the minister of information technology, recently openly supported Zoho’s software package for official government work. In the meantime, Arattai has experienced a dramatic increase in downloads in recent weeks.

Additionally, Zoho launched a new sub-brand last week named Vani to provide “visual” workplace communication products driven by AI. Along with its extensive language model, the company unveiled a suite of AI tools in July to help organisations with automation, easy integration, and customised AI agents. In order to increase its robotics research and development skills, it also purchased the robotics firm Asimov Robotics earlier this year.

Quick Shots

•Zoho launches new POS devices and soundbox under

Zoho Payments to boost digital payment solutions.

•Zoho collaborates with NPCI Bharat BillPay Ltd

(NBBL) to address real-world payment challenges and strengthen India’s

digital infrastructure.

•Zoho plans to integrate Zoho Pay with Arattai messaging

app for in-app payments.

•Zoho introduces payout features, virtual accounts,

and marketplace settlements for businesses.

•Zoho received payment aggregator licence in Feb last

year, officially entering the payments market.

After 4.5 years of operation, the fintech startup Niro, which assisted consumer internet platforms in offering embedded credit products, has closed. Investors like Elevar Equity, GMO Venture Partners, Rebright Partners, Mitsui Sumitomo Insurance VC, Innoven Capital, Alteria Capital, and CRED founder Kunal Shah supported the Bengaluru-based company, which was established in 2021 by Aditya Kumar and Sankalp Mathur.

In a LinkedIn post announcing the shutdown, Kumar stated that after 4.5 years, $20 million in finance, $200 million in loan disbursements, and 30 collaborations, “we’ve had to shut down Niro.”

What is the Core Reasons for Niro’s Clossure?

Just as the company was changing its business model, Shah explained, it was struck by “a perfect storm of regulatory pushback on personal lending, credit deterioration, and sub-optimal capitalisation,” which led to its demise. By collaborating with banks and NBFCs, Niro’s primary offering was to assist online platforms in integrating credit products; in other words, it transformed big consumer apps into fintech distribution channels.

The business expanded quickly and was one of the first in this field. According to Kumar, Niro had accomplished the seemingly impossible by recruiting amazing people, raising patient, high-quality funding, and persuading major consumer internet platforms and top lenders to collaborate with us in order to unleash value at scale.

Within just over two years of its start, Niro had $100 million in assets under management, and at its height, its platform had over 170 million members. During its existence, it also signed 30 partnerships and disbursed $200 million in loans. However, the company was compelled to alter its strategy at an unfavourable moment due to the swift legislative changes in the digital lending environment, declining credit quality, and financial limitations. Kumar described the situation as “a perfect storm.”

Financial Dynamics of Niro

Tracxn, a market intelligence platform, reports that Niro raised $18.7 million in four investment rounds, valued at $58.4 million. It had about 290 employees at its height. With ten years of experience, Kumar is a fintech entrepreneur who founded Qbera, a digital lending company that InCred later purchased. He oversaw InCred’s consumer loan division after the acquisition.

The closure of Niro coincides with a number of fintech startups dealing with increasingly stringent laws, declining credit scores, and a more conservative investment climate, all of which have made it harder to scale lending operations.

Quick Shots

•Fintech startup Niro, backed by Kunal Shah and top

VCs, shuts down after 4.5 years of operations.

•Launched by Aditya Kumar and Sankalp Mathur to help

consumer internet platforms offer embedded credit products.

•Raised $18.7M in funding, valued at $58.4M,

disbursed $200M in loans, and had 30+ partnerships.

•Achieved $100M AUM and reached 170M+ users at its

peak.

•Closure reflects wider fintech struggles with new

regulations, investor caution, and scaling hurdles.

When it comes to managing expenses and bills, especially when one has low funds. This becomes really pressurizing and people start looking for sources to lend money from. In such situations, borrowing from friends and family could be embarrassing and hectic. And depending upon banks could cost major interests. So where should we look?

Well by acknowledging these situations and deals, online money lending apps are developed. These provide the facility to lend money through digital platforms without any further issues.

Multiple companies are providing the facility of offering loads immediately with minimal competitive interest rates and required tenure durations. These companies facilitate the loan very easily and quickly as compared to usual bank loans.

With keeping such progress in mind, India has developed numerous digital lending companies whose finances can manage smoothly. India is evolving to a great extent in the digital sector and financial inclusion. The country has cash for transactions. But with the evolving method of development and modernization, India is shifting toward a cashless economy. To understand its development more prominently, let’s look at the top 10 digital lending platforms in India.

Best Digital Lending Platforms in India – Lendingkart Website

The prominent digital lending platform, Lendingkart was founded in 2014. It works by offering different capital loans and company loans vary from small to medium-sized businesses across India. They are widely famous for providing capital completely through an online platform and require minimum documentation for the procedure to begin.

For young entrepreneurs, managing their finances becomes quite hectic and it deviates them from focusing on their business growth. That’s why Lendingkart has taken the initiative to make capital funding easily available for entrepreneurs so they don’t have to worry about the cash-flow gaps. Lendingkart is a company established in Ahmedabad, Mumbai and Bangalore. But, its services are accessible throughout the whole of India.

2. Pine Labs

Lending Platform

Pine Labs

Loan Amount

From ₹25,000 to ₹5 Lakhs

Loan Tenure

90 Days

Best Digital Lending Platforms in India – Pine Labs Website

Pine Labs is one of the leading fintech companies in India established in 1998 that provides digital lending services. The company is quite famous for its incredible facility of transforming the mobile NFC into a card machine and activating the service of accepting all types of payment digitally which also includes the ‘Tap n Pay’ card as well.

Pine Labs have brought tons of services for the retailers including multi-channel, different payment options, brand offerings, risk assessments, analytics, and many more.

It provides working capital loans for small to medium businesses. Their loan application process is quite simple and you can apply for a business loan through their website or their app myPlutus.

Pine Labs’ services and technologies are widely preferred and used by more than 100,00 merchants all across India and also, many Asian companies. According to the estimations, PineLabs’ cloud-based technology has the power of over 350,000 PoS terminals; that too in more than 3,700 cities.

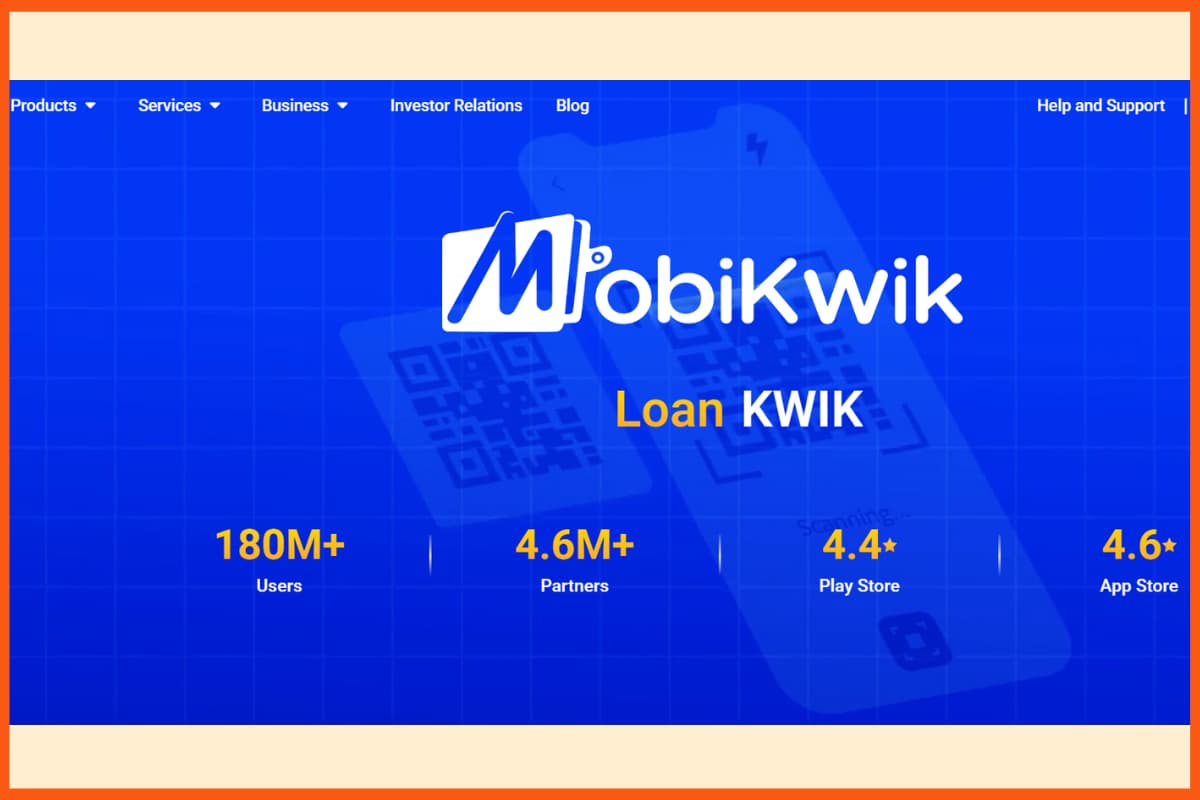

3. MobiKwik

Lending Platform

Mobikwik

Loan Amount

Upto ₹5,00,000

Loan Tenure

6 to 36 Months

Top Loan Aggregators in India – MobiKwik Website

MobiKwik is a very prominent mobile payment company that works by connecting the consumers together with the merchants and many online sellers. The company is established in Gurgaon, Haryana, India.

Mobikwik is a private company that has more than 550 employees. Since the establishment of this company, the company has raised a total of 118 million USD from over 8 funding rounds.

Mobiwik provides instant personal loans. You can download its app and once the loan is approved it will be credited to your wallet.

₹1 Lakh to ₹15 Lakhs (unsecured) or up to ₹2.5 Crores (secured)

Loan Tenure

6 to 48 Months (unsecured), Up to 84 Months (secured)

One of the biggest lending companies, Shiksha Finance, is an education-based finance firm. Shiksha Finance provides the services of funding parents for school fees by reducing the school drop-out rates. It also offers capital to educational institutions for the development of buildings, properties and working capital.

Shiksha Finance has loans that range from INR 10,000 to INR 50,000 with a return duration of 6 to 10 months. The loans which Shiksha Finance provides can be utilized for educational based purposes such as school fees, tuition, luggage and stationary.

5. MoneyTap

Lending Platform

MoneyTap

Loan Amount

Upto ₹5,00,000

Loan Tenure

36 Months

Best Digital Lending Platforms in India – MoneyTap Website

The Bengaluru based lending company, MoneyTap is known for its huge service of offering credit lines for the consumers as their loans, with the partnership with RBL Bank. MoneyTap is now counted among the leading lending businesses. Recently, the company received the license of NBFC for co-lending space together with their lending partners.

MoneyTap has offered many great features among which, the minimal documentation procedure for a personal loan is the most special one. Moreover, its app version also provides the facilities for tracking down your borrowing records.

6. Paytm

Lending Platform

Paytm

Loan Amount

Upto ₹2,00,000

Loan Tenure

6 to 36 Months

Fintech Lending Companies in India – Paytm Website

The biggest digital lending wallet company Paytm is wildly famous in the minds of Indians. The company is established in Noida, Uttar Pradesh. Paytm has grown to a great extent and now, millions of downloads have been made.

The development the company has received is breathtaking. It employs more than 9000 people and has a revenue of a total of $118 million. Paytm is highly specialised in online shopping as well.

Best Digital Lending Platforms in India – PolicyBazaar

The company is counted among the top leading online insurance companies, PolicyBazaar was established in the year 2008 and headquartered in Gurgaon, Haryana, India.

It is online life insurance as well as a general insurance aggregator company. PolicyBazaar is very popular among Indians for its incredible services and holdings. It employs over 2500 people and has an annual revenue of $21 million (as estimated in 2017-18).

The current CEO of PolicyBazaar is Yashish Dahiya who is also one of the founders of this company. It has raised around US$ 346 million through 7 funding rounds.

8. Capital Float

Lending Platform

Capital Float

Loan Amount

₹50,00,000

Loan Tenure

Upto 36 Months

Best Digital Lending Platforms in India – Capital Float Website

Capital Float is one of the leading lending companies in India. It is acquired by CapFloat Financial Services. Capital Float is popular for its amazing service of specialised financial loans and business credits.

Capital Float has a partnership with some prominent companies such as Shopclues, Paytm and Uber. The company lends the potential borrower through its system of proprietary loans. Capital Float is now targeting established store owners and small merchants.

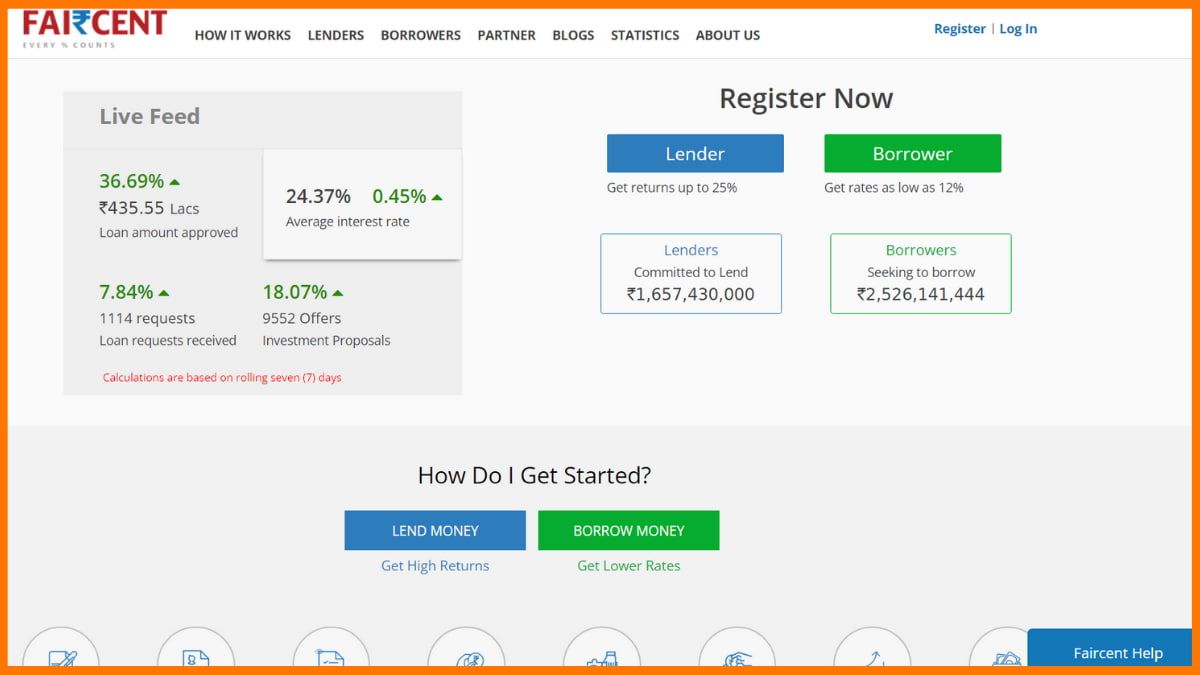

9. Faircent

Details

Information

Loan Amount

₹5,00,000

Loan Tenure

6 to 36 Months

Best Digital Lending Platforms in India – Faircent Website

The largest and first Indian peer-to-peer digital lending platform, Faircent is known to be absolutely amazing. It is officially registered by the RBI. It provides a safe marketplace for people to loan money to a borrower. Faircent facilitates the credit to organizations and individuals who are interested in lending money.

Faircent provides the absolutely convenient procedure of lending the required money to those who need it, at reasonable interest rates.

10. KreditBee

Lending Platform

KreditBee

Loan Amount

₹5,00,000

Loan Tenure

6 to 36 Months

Lending Service Providers in India – KreditBee

KreditBee is a Bangalore-based fintech that offers quick personal loans up to INR 2,00,000 for working professionals. Using easy online KYC, the loan process is fast and simple. KreditBee is one of the top lending companies in India.

Backed by trusted investors like ICICI Bank and supported by banks like AU Small Finance, KreditBee serves over 5 million customers.

The process is mostly paperless, sign up on the app, and within 15 minutes, approved loans are transferred instantly to your bank account.

In India, there are many fintech companies that are providing the service of digitally lending money very easily with the minimal documentation procedure. Today, many apps have been developed by these companies to make the transaction of money absolutely susceptible. And for those who require a personal loan or business loan, can easily get one. That’s why we listed these top digital lending companies in India.

FAQs

What are some of the top digital lending companies in India?

Lendingkart, Pinelabs, Mobiwik, Policybazaar, and Paytm are some of the top digital lending companies in India.

How does a lending company work?

Lending companies provide loans to an entity, which is then expected to repay its debt.

How many fintech companies are there in India?

There are around 2,000 fintech companies in India.

At present, the world has experienced huge growth in online payments, and with the Covid-19 presence, people preferred to use online payment methods for almost everything as it is safe and secure. More and more people are opting for a cashless way to transfer money. Here, comes the work of the payment gateway. A payment gateway is basically a merchant service that connects the users’ bank accounts with the platform where the users need to transfer their money. A bank may provide a payment gateway to its customers, there is also a specialized financial service provider such as a payment service provider which provides it as a separate service.

Whether you are a small business or you have an established E-commerce business, good payment service is an essential factor for it. An online payment gateway is a secure and convenient way for a website or online business to accept payments from customers. When a customer makes a purchase on an e-commerce website, they enter their payment information, which is then processed by the payment gateway. The payment gateway verifies the information, checks to see if the customer has the funds available, and then transfers the funds from the customer’s account to the business’s account.

A payment gateway platform gives authority to the users to conduct an online transaction through various payment modes such as net banking, credit card, debit card, UPI, and other online payment apps. It is a third-party platform that provides the ability for the user to securely transfer their money to the merchant’s payment portal. In this era of the digital world, E-commerce is leading the market. As times are changing fast online businesses are also moving. So, it is important to know about the payment gateways in India.

In order to use an online payment gateway, you will need to sign up for an account and integrate the payment gateway into your website or online store. This typically involves adding a few lines of code to your website and may also require you to obtain a merchant account.

There are many different online payment gateways available, each with its own set of features and fees. In this article, we will talk about the top payment gateways in India that allow customers to make payments online. So, let’s take a look at them.

Popular wallet-based gateway, supports UPI, cards, EMI, and Buy Now Pay Later options

1.75% onwards

Razorpay

Mobile Applications

Google Play Store

Accepted Payment Methods

Domestic and International Credit & Debit cards, EMIs ( Credit/Debit Cards & Cardless), PayLater, Netbanking from 58 banks, UPI and 8 mobile wallets

Razorpay – best payment gateway in India

Razorpay is one of the best payment gateways in India for your business. It was started in 2014. Many entrepreneurs who use Razorpay for their business, have seen some increase in their conversion rate. Razorpay has helped businesses to solve the problem of digital payments. It is due to their smooth user experience. Also, the refund process is easy and automated. If your customer applies for a refund, Razorpay will automatically get the refund, if you set it to, without any extra widget or code. You can use Razorpay Subscriptions to execute the automated recurring transactions on various payment modes, through a platform that’s built for automation.

Razorpay Features

You can improve your business sales as Razorpay provides cashback and discounts to your customers

Payment modes include credit cards, debit cards, net banking, payments through UPI, and popular wallets.

Razorpay allows you to accept international payments from over 100 countries.

Manage your marketplace, automate bank transfers, collect recurring payments, share invoices, and avail working capital loans.

Instamojo

Mobile Applications

Google Play

Accepted Payment Methods

170+ payment methods including RTGS/Bank Transfer/NEFT/EMI

Instamojo – best payment gateway in India

Instamojo is one of the top-rated payment gateways in India. It allows businesses to create a business account instantly and the account can also be activated within a few minutes to collect online payments. This is a Bangalore-based company and the target of Instamojo is selling digital goods and collecting payments online. You can enroll yourself at Instamojo with a bank account and start your online selling business. You can also collect payments for physical goods and workshops or events.

Instamojo Features

To set up the payment gateway, no extra payment is needed.

Different types of payment methods are available.

Special care is being taken for the security of the server.

Businesses can create discount codes for their products.

Paytm has emerged as a leading payment gateway in India due to its online customer base with the very popular Paytm wallet. It supports domestic credit cards like Visa, MasterCard, Maestro, Amex, Discover, and Diners. With Paytm online transactions can be made anytime and from anywhere. It is the best payment gateway solution provider in India which has served some biggest eCommerce companies.

Some of the most popular companies which use Paytm are Jabong, OLA, Cleartrips, Redbus, GoIbibo, Zomato, etc.

How to Create Payment Links from the Paytm Business Dashboard

Paytm Features

The latest technologies are used for secure online transactions.

It has the feature of saved cards, where a customer doesn’t have to put their card details again and again.

Paytm is not only available as a desktop application but also supports smartphones and tablets.

CCAvenue – Payment Gateway for Small Business in india

CCAvenue is an authorized payment gatewayprovider by Indian Financial Institutions and is known as the most secure and best payment gateway to transact money for online shopping. Customers can make online transactions via Credit Cards, Debit Cards, Net Banking, Digital and Mobile Wallets, Mobile Payment, and Cash Card modes. It offers smooth, fast, and secure transactions to its customers. Currently, CCAvenue powers more than 85% of businesses in India.

CCAvenue Features

CCAvenue provides “Smart Analytics” by which you can see a real-time comprehensive statistical online report and a transparent history of all your transactions.

It has a ‘Mobile Checkout Page’ which supports all mobile operating systems.

CCAvenue also has CCAvenue In-built Advanced Shopping Cart’, CCAvenue S.N.I.P. ( Social Network In-stream Payments), it is one of India’s first genuine Social Commerce facilities.

Payflow

Mobile Applications

App Store and Google Play

Accepted Payment Methods

Accept all major debit and credit cards supported by their processor, including Visa, Mastercard®, American Express, Discover, JCB, and Diners Club. Payflow Gateway also supports L2/L3 purchase cards, prepaid cards, foreign currencies, TeleCheck, and ACH.

Payflow Logo

Payflow is offered by PayPal. It is known for being a secure and open gateway for payments. Payflow accepts all major credit and debit cards. It adds over 173 million customers regularly and supports more than 100 currencies. In India, it is used by Merchants for receiving international payments.

Payflow Features

It accepts and offers different payment methods.

The checkout process is customized with the help of APIs.

It supports fraud protection services and allows you to install it for an additional fee.

UPI, EMI, digital wallets, Debit/Credit cards, and 100+ other payment options

Cashfree – top payment gateway in India.

Cashfree is a low-cost and popular payment gateway in India. Cashfree helps businesses in India to accept payments online from various payment channels. The best thing about Cashfree is that it has direct integration with multiple banks which makes Cashfree a fast and reliable payment gateway. It is the only payment gateway in India that provides a wide range of payment options such as Visa, MasterCard, Maestro, Rupay, and Amex, including 70+ more net banking options. Cashfree also supports UPI, NEFT, IMPS, and PayPal. TDR is the transaction discount rate that every payment gateway charges from the merchants for processing the transactions to their bank account.

Cashfree Features

The setup cost is not needed.

Cashfree also supports online wallets like Paytm, PhonePe, and GooglePay.

Cashfree is the fastest settlement cycle of 24 hours to 48 hours and also offers popup, iframe and seamless checkout modes

BillDesk

Mobile Applications

Google Play Store

Accepted Payment Methods

120+ Credit cards, Debit cards, Banks, Net Banking, Wallets

BillDesk – online payment gateway provider

BillDesk is an Indian online payment gateway company based in Mumbai, India. BillDesk provides bill payment and settlement services to large billers like electricity, water, insurance, and other service providers. BillDesk also provides the ability to customers to decide how and when to make payments. BillDesk is a one-stop solution for customers through which customers can make all their payments at any time and from anywhere.

BillDesk Features

The integration is developer friendly and is quite easy and flexible..

BillDesk offers various payment methods.

Customers can also receive payment reminders or alerts.

Atom

Mobile Applications

Google Play Store

Accepted Payment Methods

Visa, Mastercard, Discover and American Express plus Amazon Pay, Apple Pay, Google Pay, PayPal, and Venmo

Atom Online Payment Gateway

Atom consists of various payment options which accept payment through all major debit cards and credit cards. Atom has completed over 15 million transactions and is used by thousands of merchants across the country. Atom is completely secured as it is backed with PCI DSS version 3.2 and 256-bit encryption which ensures a safe and secure transaction.

Atom Features

Atom provides multiple payment methods.

The integration is quite simple and easy.

Atom provides invoices after every payment.

HDFC

Mobile Applications

App Store and Google Play Store

Accepted Payment Methods

All major credit, debit cards and net banking in India, including Visa, MasterCard, Visa Electron, Diners, Rupay, Discover or Maestro

HDFC Best Online Payment Gateway

HDFC is one of the largest banks in India that offers a payment gateway service for merchants and businesses to accept online payments from their customers. Many organizations like VSNL, Sify, and IRCTC use HDFC. If you want to use HDFC on your website or mobile app, you need to use their EPI payment gateway services. The HDFC Payment Gateway allows merchants to securely accept a wide range of payment options, including credit and debit cards, net banking, and UPI payments. The advantages of the HDFC payment gateway are instant settlement, a 100% chargeback facility, the facility to accept payment in 15 international currencies, easy integration with existing applications, and support for various shopping cart applications.

HDFC Features

The HDFC Payment Gateway supports a wide range of payment options, including Visa, Mastercard, American Express, and Rupay credit and debit cards, as well as net banking and UPI payments.

The HDFC Payment Gateway uses 128-bit SSL encryption to secure your transactions and protect your financial information.

The HDFC Payment Gateway can be easily integrated with your website or mobile app, allowing you to customize the payment experience for your customers.

The HDFC Payment Gateway provides detailed transaction reports and reconciliation tools to help you manage and track your payments.

It accepts 15 types of international currencies.

It provides 24×7 customer service.

PayKun

Mobile Applications

Not Available

Accepted Payment Methods

UPI wallet payments, subscription payments, Debit/Credit cards, Master Card, diners club card, net banking, wallets, UPI/BHIM

PayKun online payment provider

PayKunis an easy solution for online payments for all types of businesses including small businesses, and medium to large. Any kind of merchant including a freelancer, a YouTuber, a blogger, from an eCommerce website or mobile app, an offline and online seller at the shop or showroom, or an individual, every type needs to have an easy hand on the modern technology for the collection of digital payments. It provides free plugins and SDKs readily available on the internet to integrate with all the major platforms of websites and mobile applications.

PayKun Features

Paykun has zero setup fees and zero maintenance fees.

It provides different types of payment methods.

The server is safe enough to use.

PayU

Mobile Applications

Google Play and App Store

Accepted Payment Methods

100 different payment methods are supported, including EMI, UPI, net banking, cards, wallets, Buy Now Pay Later, etc.

PayU best multi-currency payment gateway

PayU (formerly known as PayU Money) is one of the best multi-currency payment gatewaysto accept online payments. The PayU payment gateway is designed to be secure, reliable, and easy to use for both merchants and customers.

To use the PayU payment gateway, merchants need to sign up for an account and integrate the payment gateway into their online store or website. This can typically be done through the use of a software development kit (SDK) or by integrating with a payment processor or shopping cart platform. Once the integration is complete, merchants can start accepting payments from customers through the PayU payment gateway.

You can start accepting payments securely and seamlessly within your iOS, Android, or Windows app, within minutes, with its 100% online hassle-free onboarding process.

PayU Payment Gateway: What is a payment gateway and how does it work?

PayU Features

PayUMoney supports multi-currency transactions and international credit cards.

PayU provides over 100+ payment methods

The transaction history is available through PayU.

Mobikwik

Mobile Applications

Google Play and App Store

Accepted Payment Methods

Supports UPI, MobiKwik wallet, credit/debit cards, net banking, EMI, and Buy Now Pay Later options.

Mobikwik Best Online Payment Gateway

MobiKwik (earlier called Zaakpay) is one of the fastest-growing eCommerce payment gateways, helping businesses run smoothly. It focuses on giving users an easy experience by automatically detecting OTP (One Time Password) during payments.

Some well-known clients include Business World, BlueDart, Uber, and Zomato. Businesses can also integrate this gateway into their website or app with the help of eCommerce development companies.

Mobikwik Features:

Strong PCI DSS security to keep transaction data safe

Website analytics to track payment data

Supports credit/debit cards, wallets, international cards, UPI, and EMI options

Conclusion

The payment gateway has become the most important part of the world of increasing eCommerce businesses. If a business provides a good payment service, it automatically creates a good impression in front of its customers. With the increase of E-commerce businesses in the world, the need for proper payment gateways is also increasing.

FAQs

What is a Payment Gateway?

A payment gateway platform gives authority to the users to conduct an online transaction through various payment modes such as net banking, credit card, debit card, UPI, and other online payment apps.

Where payment gateways are used?

Payment Gateways are used mostly used by E-commerce businesses.

What are some top 5 Payment Gateways?

The top 5 payments gateways are:

Razorpay

Instamojo

BillDesk

Paytm

Payflow

Which is better, Paytm or PayPal?

The choice between Paytm and PayPal will depend on your specific needs and preferences. It may be helpful to consider factors such as geographical availability, payment methods, fees, and security when deciding which platform is right for you.

Who regulates payment gateways in India?

In India, payment gateways are regulated by the Reserve Bank of India (RBI), which is the central bank of the country.

Which is the cheapest payment gateway in India?

Cashfree Payment gateway is as of now, one of the cheapest payment gateways in India.

Is UPI available only in India?

UPI is not limited to India and has been adopted by some financial institutions and payment service providers in other countries as well such as Bhutan, Nepal, UAE, and the UK.

Which is better, Razorpay vs Billdesk?

Razorpay is better for startups and online businesses because it offers easy integration, many payment options, and instant settlements. BillDesk is more suited for large enterprises and utility bill payments due to its reliability and strong security.

Which is better, HDFC Payment Gateway vs Razorpay?

Razorpay is better for startups and developers due to its easy setup, modern features, and instant settlements, while HDFC Payment Gateway is ideal for established businesses needing a bank-backed, secure solution.

Which is the best payment gateway for startups in India?

The best payment gateway for startups in India is Razorpay because it offers easy integration, multiple payment options, fast settlements, and low setup hassle.

Which are the payment gateway for website in India?

Razorpay, PayU, and Cashfree are top payment gateways for websites in India, offering easy integration and fast payments.

Which is the best payment gateway for online business?

The best payment gateway for online business in India is Razorpay due to its seamless integration, wide payment options, and quick settlements.

Not many things out there can match the convenience that comes with a credit card. After all, what can be better than spending money- money that you don’t have to hold or carry in your wallet? Moreover, we hover around, get 6-7 weeks to pay back the same, and then also earn rewards, discounts, or cashback on it. Well, these instruments are designed in such a way that they keep you hooked.

Kudos to the noble banks and fintech players, but then – every boon comes with a T&C. Founded in April 2018 by Kunal Shah, CRED has emerged as a pivotal fintech platform that redefines the way credit card payments, rewards, and management are perceived across the nation.

This platform stands out by prioritizing the credibility of its users, employing credit scores as a criterion to curate a community of trustworthy individuals, thereby simplifying the credit card bill payment process and rewarding timely transactions with exclusive offers and discounts.

With a robust user base of almost 16 million and a valuation soaring to $6.4 billion as of June 2022, CRED’s trajectory reflects its groundbreaking approach to imbibing a gated ecosystem that benefits both individual lenders and financial institutions by ensuring a circle of high trust.

CRED’s business model, which pivoted the startup to the much-coveted unicorn status within just over two years of its inception, has been simple yet phenomenal. The USP revolves around offering a meticulous balance between user convenience and enticing rewards. The platform allows users to effortlessly manage their credit card bills, track expenses, and avail themselves of P2P lending at competitive rates, and by doing so – the Fintech major not only enhances financial health but also ingrains a culture of financial responsibility.

The platform’s focus on amplifying user value through exceptional rewards for responsible financial behavior, coupled with its strategic partnerships for exclusive deals, sets a precedence in the CC payments space, accentuating the importance of credibility and trust in the digital era.

In this article, we will be exploring the CRED business model and understanding how CRED makes money and what is its revenue model.

CRED, established in 2018 by Kunal Shah, is an innovative Indian fintech company that offers a reward-based credit card payment application. It started with the idea of targeting creditworthy individuals, specifically those with a credit score above 750, ensuring a community of high trust. However, with time – the credit card payment enabler has become more lenient when it comes to profiling individuals. The platform verifies new members by checking their credit scores with major credit bureaus such as CIBIL, Experian, and CRIF, requiring only their full name and a valid Indian mobile number for initial setup.

Credit Card Payment and Management: CRED simplifies the management of credit card expenses by providing a detailed analysis of spending patterns and efficiency, which aids users in better financial planning.

CRED Protect: An AI-driven feature, CRED Protect, offers automated monitoring of credit card payments, sends due date reminders, and analyses spending habits to prevent fraudulent transactions.

Rewards System: Upon paying their credit card bills through CRED, members gain access to exclusive rewards such as event tickets, experiences, gift cards, and premium upgrades from well-known brands like Diesel, Perfora, The Man Company, AJIO, Myntra, and others.

Additional Financial Services: Besides basic card management, CRED has expanded its offerings to include house rent payments and short-term credit lines, providing more comprehensive financial solutions.

Value of Credit Card Transactions in India

User Impact and Market Presence

User Base and Transactions: As of 2021, CRED has processed approximately 20% of all credit card bill payments in India, with a user base exceeding 5.9 million. The market share has continued to soar and grow.

Investments and Financial Health: Supported by major investors like DST Global and Sequoia Capital, CRED has raised significant funds to fuel its growth, despite reporting substantial losses in 2020 due to aggressive marketing and advertising strategies.

Strategic Acquisitions: In its pursuit to broaden its service spectrum, CRED has acquired startups like Happay, focusing on expense management, and HipBar, a liquor delivery service.

CRED continues to upscale its platform with features that promote good creditworthiness and financial discipline while rewarding creditworthy behavior, positioning itself as a cornerstone in India’s fintech scene.

Understanding the CRED Business Model – How Does CRED work?

The business model of CRED revolves around creating a seamless experience for credit card users while partnering with businesses to provide exclusive rewards and incentives.

Three Pillars of the CRED Business Model

CRED’s Customers: CRED’s customers are an essential component of its business model. While many people use payment apps or log in to their bank accounts to pay their credit card bills, CRED provides an attractive alternative by offering rewards and incentives. As more people use CRED to earn benefits, they share those benefits more widely, creating a network effect that strengthens CRED’s position in the market.

CRED App: The CRED app is a key component of its business model. The app provides users with a user-friendly interface to see all the available offers for paying their credit card bills. As users continue to pay bills, they accumulate CRED coins, which they can redeem for rewards.

Businesses That Provide Offers On The App: This is another important pillar of CRED’s business model. By bringing businesses on board and forming tie-ups with them, CRED provides small and large businesses alike with visibility, as buyers of all types use the app. This partnership is beneficial for businesses, as it allows them to increase their customer base and revenue while also providing users with more rewards and incentives to use the app.

CRED Revenue Model – How CRED Makes Money?

CRED Revenue Model – How CRED Makes Money?

The progressive business model of CRED leverages multiple revenue streams to create a robust ecosystem for creditworthy users. Here’s a detailed breakdown of how cred makes money:

Revenue from Business Listings

Businesses pay to display their products and offers on the CRED app, generating significant listing fees for the platform.

Transaction-Based Earnings

CRED charges a processing fee ranging from 1 to 1.5% on various transactions, which includes payments made through CRED pay.

Additional revenue is earned through commissions on sales from advertisements optimized to encourage spending on the platform.

Interest and Commission from Financial Services

The platform earns interest on loans provided through peer-to-peer lending and CRED Stash.

A commission is also earned from transactions where users redeem CRED coins for offers from partnered brands.

Diverse Financial Offerings

CRED’s array of services, such as CRED Pay, CRED Store, and CRED Escapes, ensures a broad base from which to draw revenue, ranging from payment processing fees to premium subscriptions.

Strategic Revenue Sharing

A revenue share is obtained from partnered brands when users redeem points for rewards, integrating user engagement with profitability.

Thus, by focusing on a trust-based model, CRED not only secures a high-engagement user base but also creates a profitable framework through diverse revenue channels, making it a unique player in the fintech space.

Let’s decode the revenue streams of the Shah-led company and understand how they make the revenue model of CRED a big-time success.

Revenue Composition and Growth

Primary Revenue Sources

CRED’s positioning revolves around multiple income streams that the neo-fintech player has figured out over the years. The majority of its income, nearly 90% – is derived from three key services: CRED Cash, Cred Max, and various insurance products. These services cater to the essential needs of the platform’s creditworthy user base, ensuring a steady influx of revenue.

Operational Revenue Enhancement

CRED saw its operating revenue grow by 71% to INR 2,397 crore in FY24, up from INR 1,400 crore the previous year.

Including other income, CRED’s total revenue increased by 66%, reaching INR 2,473 crore in FY24, compared to INR 1,484 crore in FY23.

However, despite the rise in revenue, the company’s net loss expanded by 22%, reaching INR 1,644 crore in FY24, up from INR 1,347 crore the previous year. CRED noted that its operating loss decreased by 41%, dropping to INR 609 crore from INR 1,024 crore in FY23.

For the fiscal year 2023, CRED reported a substantial increase in operational revenue, which grew by 3.5 times to reach INR 1,400.6 crore, up from INR 393.5 crore in the previous fiscal year. This growth highlights the effectiveness of CRED’s business strategies and its ability to monetize its services efficiently.

Particulars

FY23

FY22

Revenue from Operations

INR 1,400.3 crore

INR 394.4 crore

Other Income

INR 84.4 crore

INR 28.2 crore

Total Revenue

INR 1,484.6 crore

INR 422.6 crore

CRED Financials 2024

Fee-Based Earnings

CRED capitalizes on transactional processes by charging a processing fee of approximately 1-1.5% on various transactions made through the platform. Additionally, the platform earns fees when users select offers from the ‘Discover’ section, further augmenting its revenue.

Interest Income and Financial Services

A significant portion of CRED’s revenue also comes from interest earned on peer-to-peer lending and CRED Stash, which provides an instant credit line to customers. This not only diversifies CRED’s revenue streams but also enhances user engagement by offering financial solutions within the app.

Strategic Financial Management

Despite a notable increase in revenue, CRED’s total operating expenditure, including one-time costs, amounted to INR 3,082 crore in FY24. Whereas, the company’s total expenditure rose by 66.4% to INR 2,832 crore in FY23 from INR 1,702 crore in FY22. The company has strategically reduced marketing and promotional expenses by 26.8% to INR 713 crore in FY23 from INR 976 crore in FY22, focusing more on direct integrations with banks to lessen payment processing charges. Through the continuous evolution of financial strategies and optimization of its service offerings, CRED is not just sustaining but also significantly strengthening its fiscal footprint in the competitive fintech arena.

CRED’s Value Proposition to Users

CRED’s value proposition uniquely intertwines convenience with rewards, offering a robust platform for creditworthy individuals to manage their finances effectively and enjoy exclusive benefits. Here’s how the CRED business stands out:

Kunal Shah Led CRED’s Value Proposition to Users

Rewards for Financial Responsibility: Users earn rewards for timely credit card payments, which not only encourages punctual bill settlements but also aids in maintaining a healthy credit score.

Suite of Financial Management Tools: With features like CRED Protect and Smart Statements, users can effortlessly monitor transactions, identify discrepancies in their credit reports, and initiate disputes to correct them, ensuring financial accuracy and security.

Exclusive Access to Deals and Offers: Membership in CRED opens doors to curated deals and premium packages, allowing users to make significant savings on various purchases, enhancing the shopping experience, and providing real value for money.

More Payment Options with CRED Max: Beyond credit card bills, CRED Max enables users to conveniently pay for rent, utilities, insurance premiums, and even subscriptions, simplifying the management of regular expenses.

Better User Experience: CRED’s interface is designed for ease of use, making financial transactions not just simple but enjoyable. This focus on user experience helps retain members and fosters long-term loyalty.

Security and Privacy: All personal data and transactions on CRED are securely encrypted, ensuring that users’ financial information remains private and protected.

Appealing to Diverse User Needs: CRED appeals to a broad segment of financially savvy users, from those seeking to improve their credit scores to privacy-conscious consumers, all finding value in the platform’s offerings.

Understanding user needs through innovative features and maintaining a high standard of security has led CRED to successfully deliver a compelling value proposition that resonates with its target audience.

Competitive Scenario and Differentiation Challenges

Operating in a Crowded Market: CRED operates in a highly competitive digital finance market in India, where numerous loyalty programs vie for consumer attention. Establishing a distinct presence amidst this crowd poses a significant challenge for how CRED works.

Effective Communication: The crucial task for CRED is to effectively communicate its unique value proposition. Many potential users are already familiar with traditional loyalty rewards programs, making it imperative for CRED to highlight its differences and benefits clearly and persuasively.

Competition and Market Positioning

Facing Established Giants: CRED encounters intense competition from well-established players in the payments and financial services sector, including the likes of companies like Gpay and PhonePe. These competitors offer similar services, which necessitates CRED to continually innovate and offer superior value to retain and attract users.

Differentiation Strategy: To stand out, CRED needs to keep differentiating itself through unique features, exceptional user experiences, and tailored services that resonate with its target audience of creditworthy individuals. It is even trying to do so by constantly gamifying the platform with animated contests, among others.

Future Prospects and Strategic Focus

Sustainable Monetisation: While CRED has successfully attracted a large user base and built a strong brand, the ongoing challenge is to monetize this base in a sustainable manner. The focus must be on creating long-term value for users without compromising upon profitability.

Playing Upon Brand Strength: CRED’s future prospects will heavily rely on its ability to make the most out of its brand and user trust to introduce new revenue-generating services and expand its market reach without compromising on user experience or data security.

CRED plans to grow by tapping into digital payments, promoting financial literacy, and using technologies like AI to enhance user experience. It aims to expand through strategic partnerships and new market entry. Additionally, CRED is part of the RBI’s e-rupee pilot, exploring India’s digital currency future.

CRED needs to address these challenges and capitalize on opportunities. If done in the right way, the CC leader can continue to enhance its market position and achieve sustained growth in the long run.

Looking ahead, the road for CRED is both challenging and ripe with opportunities. As the platform continues to hover through the market dynamics and explores sustainable monetization strategies, its innovation-led approach will be crucial. The significance of the CRED business model lies not just in its current achievements but in its potential to shape future financial behaviors and market trends.

Consequently, the broader implications of the company’s success extend far beyond its immediate ecosystem, potentially influencing the global fintech dream and offering insights into the power of trust and reward in building a financially responsible society.

FAQs

What does CRED do?

CRED is an innovative Indian fintech company that offers a reward-based credit card payment application.

How does CRED make money?

CRED earns money from fees charged to businesses for the privilege of showcasing their products and offers on the CRED app. In addition, CRED earns money from transaction-based earnings, interest and commissions from financial services, and diverse financial offerings.

What is the CRED membership process?

To make the most out of CRED, you must have a credit score (CIBIL) of 750 or simply own a credit card. Upon joining, CRED will request permission to access and verify your credit score from credit bureaus such as Experian, CRIF, and CIBIL to assess what services it would extend to you, based on your rapport.

What issue does CRED aim to address?

CRED was born out of Kunal Shah’s challenges with managing multiple credit cards. The platform aims to tackle the issue of late payments on credit card bills, which can lead to accruing interest and damaging one’s CIBIL score. CRED provides a solution by helping users manage their credit card payments more efficiently.

How does the CRED app work?

CRED is a credit card bill payment app that rewards users with cashback and discounts for timely payments. Users link their credit cards, pay bills through the app, and earn perks from various brands. The app also offers credit score tracking for financial monitoring.

Is CRED a profitable company?

CRED saw its operating revenue grow by 71% to INR 2,397 crore in FY24, up from INR 1,400 crore the previous year. Despite the rise in revenue, the company’s net loss expanded by 22%, reaching INR 1,644 crore in FY24, up from INR 1,347 crore the previous year.

What is the CRED revenue model?

The revenue model of CRED involves revenue generation through diverse channels, including, Revenue from Business Listings and Financial Institutions, Transaction-Based Earnings, Interest and Commission from Financial Services, Diverse Financial Offerings, and Strategic Revenue Sharing.

What is CRED business model?

The business model of CRED is built on three pillars – its customers who pay credit card bills, the CRED app, and the businesses that provide offers on the app.

How CRED works?

CRED is accessible only to individuals with a credit score of 750 or higher (CIBIL). The app verifies your credit score by requesting access from credit bureaus such as Experian, CRIF, and CIBIL. If you meet the eligibility criteria, CRED allows you to link your existing credit cards to your account.

Through its Indian distributor, Redington (India) Limited, SaaS fintech giant Zaggle has teamed up with Google to launch a scheme that would increase business productivity while giving staff members access to high-end technology through structured lease alternatives. By integrating with Zaggle’s employee benefits plan, this application, Smart Employee Purchase (EPP+), will assist companies in cost management and enhancing employee engagement. In terms of business optimisation, companies can maximise cash flow by using structured leasing models to take advantage of tax benefits and lease payments that are predictable. In addition, risks will be reduced with the aid of enterprise-grade security, frequent upgrades, and full lifecycle management. Additionally, companies will be able to purchase and manage devices’ lifecycles with a single provider.

With the five-year deal, Redington will act as a middleman between Google and Zaggle in a domestic relationship. The business affirmed that there are no related party transactions involved in the agreement and that Redington is not of interest to promoters or promoter group entities.

How Collaboration can Benefit Employees?

Employee benefits include discounted access to Google Pixel devices, which come with theft and ADLD (Accidental Damage and Liquid Damage) coverage. Compared to market prices, workers in higher tax groups could save up to 35%. The concept promises to improve financial planning by lowering the total cost of ownership and providing tax savings through salary packaging. According to Godkhindi, managing director and CEO of Zaggle, the company is providing organisations with a complete device management solution that combines cost-effectiveness, security, and easy administration through the Smart Employee Purchase (EPP+) program. This program gives businesses the ability to make investments in their employees, increasing employee satisfaction and engagement while making sure they are prepared for the future.

Recent Developments at Zaggle

Raj Narayanam founded Zaggle in 2011, and the company now offers businesses solutions for payments, costs, and corporate employee perks. It provides a variety of SaaS tools, including Zaggle Propel for employee incentives and rewards, Zaggle EMS for cost management, and Zaggle Save for managing expenses and rewards. The company claimed to have over 3,300 clients at the end of Q3 FY25, including BigBasket, Mumbai Metro One, Zomato’s Blinkit, and HT Media. The board recently approved the SaaS giant’s all-cash acquisition of a 16.67% share in Mobileware Technologies Private Limited, a supplier of digital payments services. In addition, Zaggle’s third-quarter (Q3) financial results for the fiscal year 2024–2025 (FY25) showed excellent financial performance. For the quarter in question, its consolidated profit increased 30% year over year (YoY) to INR 19.74 Cr. Similarly, in Q3 FY25, operating revenue jumped 69% YoY to INR 336.89 Cr.

When we look at a business, one of the reasons behind its success and survival is definitely hard work and persistence. The same goes for a relationship, if you want it to last long, you need to make efforts and give your best, that’s how it works. People say that your significant other is your biggest form of strength and support, when you are building your business from the scratch, this strength and support can be of great help.

Nothing can be better than your life partner becoming your business partner. The trust, mutual respect, and the level of communication that is needed between business partners are already present in the relationship between real-life partners. Both of them are familiar with each other and their working style and know quite well what fuels their passion.

In this article, we will talk about famous couples in business together, and with their hearts and brains, they are conquering the business world. So let’s get right into it.

“The price of success is hard work, dedication to the job at hand, and the determination that whether we win or lose, we have applied the best of ourselves to the task at hand.” – Vince Lombardi

Top Couple Entrepreneurs in India – Ghazal Alagh and Varun Alagh

One of the most successful personal care product brands, Mamaearth was introduced by the dynamic duo of Ghazal Alagh and Varun Alagh in 2016. While expecting their baby at that time, both the couple decided to launch personal care products for babies when they realized, there was a limited number of chemical-free products present in the market.

Now the brand is not only for babies but is making products for everyone. The ingredients used to make the products are all-natural and plant-based and right was the first unicorn of 2022 with its valuation of $1.2 Billion.

Top Couple Entrepreneurs in India – Vineeta Singh and Kaushik Mukherjee

Vineeta Singh and Kaushik Mukherjee started SUGAR Cosmetics in 2012. They wanted to make long-lasting makeup for young people in India. Their products suit Indian skin tones, weather, and lifestyle. Vineeta and Kaushik are one of the most successful business couples in India.

Today, SUGAR Cosmetics sells on its website, big online stores like Nykaa and Myntra, and in many shops and pop-ups across India. It has become a top makeup brand that is affordable and popular. Vineeta Singh is also seen as an investor on Shark Tank India.

Top Couple Entrepreneurs in India – Shubra Chadda and Vivek Prabhakar

This 2010 venture that deals with fashion and home décor products was founded by the couple Shubra Chadda and Vivek Prabhakar. The amount of courage to set their dream company they showed was immeasurable; they sold their apartment in Bangalore to establish Chumbak and struggled together to be where they are now. The company now has over 44 stores in India that sell a variety of lifestyles related products. The current value of the company is $30 Million.

Shikhar Singh & Nidhi Singh – Samosa Singh

Top Couple Entrepreneurs in India – Shikhar Singh & Nidhi Singh

Probably the most loved Indian snack in the country, Samosa has an immense fan following. It is not at all different for Nidhi Singh and Shikhar Singh as well. The couple decides to form Samosa Singh in 2015, a Samosa snack brand that offers different regional varieties of the said snack to its customers.

By using fresh and hygienic ingredients while making the food item, it has able to grasp the attention of the mass. They sold their apartment for a big kitchen so that they can cater to the orders of the corporate world. The sacrifice was definitely worth it as now the valuation of the company is $7.26 Million.

Rohan Bhargava & Swati Bhargava – CashKaro

Top Couple Entrepreneurs in India – Rohan Bhargava and Swati Bhargava

Friends turned life partners; Swati and Rohan founded CashKaro in the year 2013 and since then have never looked back. It is a platform that deals with coupons and cashback. The platform provides its customers with coupons that help them get discounts and cashback while shopping online.

People while shopping from popular E-commerce sites like Myntra, Flipkart, Amazon can use these coupons. The valuation of CashKaro is $2.2 Billion.

Top Couple Entrepreneurs in India – Anand Shahani and Mehak Sagar

WedMeGood is a platform that helps you organise your wedding, from finding photographers to setting up the perfect wedding venue and getting the best makeup artist for your big day, this platform does everything. Founded by the couple Anand Shahani and Mehak Sagar in 2014, the headquarters of the company is situated in Haryana, India.

Bipin Preet Singh & Upasana Taku – MobiKwik

Top Couple Entrepreneurs in India – Bipin Preet Singh and Upasana Taku

This payment service provider online platform was founded in the year 2009 by the married couple Bipin Preet Singh and Upasana Taku. The platform helps in booking tickets, recharging, paying bills for electricity and other services. Its vision was to transform the landscape of digital payments in India and it has been successfully doing that for a long time. Currently, the valuation of MobiKwik is $700 to $750 Million.

Arjun Shetty & Rati Shetty – BankBazaar

Top Couple Entrepreneurs in India – Arjun Shetty and Rati Shetty

BankBazaar was founded by the childhood sweethearts and married couple Arjun Shetty and Rati Shetty in 2008. This fintech company helps people compare offers related to debit cards, credit cards loans, mutual funds, and others with different banking and non-banking financial companies. The current value of BankBazaar is $280 Million.

Bhavna Anand Sharma & Siddhesh Sharma – Cureveda

Top Couple Entrepreneurs in India – Siddesh Sharma and Bhavna Anand Sharma

This company is mainly focused on solving some common illnesses like diabetes, thyroid, and heart-related problems. In 2014, the married couple Bhavna Anand Sharma and Siddhesh Sharma joined hands and started Cureveda which creates herbal supplements to solve common health-related problems. Various ranges of dietary and herbal supplements are produced for customers that are 100% Vegetarian.

Kuonal Lakhapati & Aayushi Lakhapati – Upnourish

Top Couple Entrepreneurs in India – Kuonal Lakhapati & Aayushi Lakhapati

Upnourish is a meal replacement product venture. It is mumbai based Health & Wellness startups that enables people to eat healthy yet low on calories meal in their busy life schedules. Upnourish aims to make health and nutritional food easily available and convenient to all aspirational people with busy lifestyle so that they do not have to compromise on their health goals.

Naina Ruhail & Prateek Ruhail – Vanity Wagon

Top Couple Entrepreneurs in India – Naina Ruhail & Prateek Ruhail

Vanity Wagon (‘VW’) is India’s first and largest clean beauty marketplace. One of the finest information-oriented beauty marketplaces, that pledges to bring only toxin-free and natural beauty products to its consumers. VW offers a trust-worthy platform where one of the most requested elements between a business and a customer, i.e, transparency would be paramount of our relationship. Be it beauty or personal care, it swears by to bring the safest solutions to your doorstep without any hassle. VW stands by the rule of never having to compromise in any manner to find the right products for our customers. It believes in sustainable beauty and stands firm in its mission to educate the audience and deliver what’s best for them. It is curating the best of clean beauty without compromising on efficiency and ensuring that the products are cruelty-free. Prior to onboarding any brand, it always check whether the brand is certified- cruelty-free by PETA and safe-to-use by ECOCERT or other recognized institutions.

Aarti Gill & Mihir Gadani – OZiva

Top Couple Entrepreneurs in India – Aarti Gill & Mihir Gadani

A spouse can be a life partner and a business partner at the same time. Valentine’s Day is all about signifying appreciation and love for one’s significant other. Like building and maintaining a relationship, business partnerships also hinge on chemistry between co-founders, trust, and effective communication. When life partners start a business together, there is a good compatibility which in turn helps the business grow because life partners understand each other the most out of anyone in this world.

The Indian startup ecosystem is buzzing with new startups every day, growing on the back of rising undertakings of capital interest. With the progress in the number of startups, love has found its way, in the form of a couple’s journey to build a successful business together. Their shared familiarity and values along with both their working styles can become powerful tools in fueling the passion for business.

These husband-wife entrepreneur duos have come together and made the most of their shared effective communication and trust in running a business successfully. Take a look at emerging Indian and popular brands started by couplepreneurs.

India’s first certified clean-label active plant based nutrition and wellness brand, OZiva was launched in 2016 by Aarti Gill and Mihir Gadani as co-founders. The brand is India’s first certified Clean Label Brand that offers an inspirational range of holistic plant-based nutrition, beauty and health products along with a fully digitized ecosystem intended to enable millions of Indians people towards living a healthier and better life. OZiva offers an inspirational range of holistic plant-based nutrition, beauty and health products. The brand recently launched the OZiva Clean Beauty Range and Kids Nutrition Range as well. Aarti’s technical and marketing wizardry alongside her youthful disposition and passion towards health & fitness along with Mihir true believer of combining the different aspects of Yoga, Ayurveda & Functional Fitness for optimal health, has been the driving force behind the rise of OZiva.

Sandeep Singh & Nikki Singh Arora – Blue Tribe

Top Couple Entrepreneurs in India – Nikki Singh Arora & Sandeep Singh

According to husband-wife duo Sandeep Singh and Nikki Singh Arora – the founders of Blue Tribe, the will to raise their daughter in a greener environment inspired them to build Blue Tribe as a one-of-a-kind food-tech company, which brings out plant based alternate meats like Chicken Keema, Chicken Nuggets, Mutton Keema, Chicken Momos, Chicken Sausage, etc. Through BlueTribe, they strive to arouse a lifestyle change in non-vegetarian food lovers so that everyone can take a conscious step towards healing the green planet. Their vision is to offer the perfect alternative of meat-based food items made entirely from plant-based ingredients. The best part is, these modernistic plant-based meat products are similar in taste, texture and quality and thus offer a genuine chance for meat lovers to choose a relatively more sustainable and eco-friendly substitute without compromising anything.

Nidhi Yadav & Satpal Yadav – AKS Clothing

Top Couple Entrepreneurs in India – Nidhi Yadav & Satpal Yadav

A Yuvdhi Apparels Private Limited brand, AKS Clothing, was started in 2014 by a hitched couple, Nidhi Yadav and Satpal Yadav. AKS clothing is renowned for its great taste in design and long-lasting material quality and has been the pinnacle of beautiful, graceful, and stylish women’s attire. The AKS clothing line comprises the best and most fashionable fabrics available.

Conclusion

When your significant other becomes your business partner, starting with your dreams become much more interesting because they are familiar with their working styles and characteristics.

Finding a perfect business partner can be quite a tough job but if it is your life partner, the difficult path may not become easier but you will definitely get the courage to face the upcoming challenges. The above couple entrepreneurs proved that the couple that hustles together, reach the peak of success together.

FAQs

Can a couple start a business?

If a couple starts a business, it might turn out to be a dream job, as they already have the required bond and mutual respect that is needed between business partners.

Who are some of the top successful couple entrepreneurs?

Varun Alagh & Ghazal Alagh, Shubra Chadda & Vivek Prabhakar, Shikhar Singh & Nidhi Singh, and Bipin Preet Singh & Upasana Taku are some of the successful entrepreneurs.

Who is Aarti Gill husband?

Mihir Gadani is the husband of Aarti Gill. They have founded OZiva company.

What can be the best business for husband and wife to start?

A husband and wife can start a business that matches their skills and interests. Some great options include a café or bakery if they love cooking, an online store for fashion or handmade products, a consulting business in their expertise, or a content creation venture like blogging or YouTube. They can also explore franchise businesses, event planning, or a fitness studio. The key is to choose something they enjoy and can manage together efficiently.

StartupTalky presents Recap’24, a series of exclusive interviews where we connect with founders and industry leaders to reflect on their journey in 2024 and discuss their vision for the future.

Fintech sector of India is going a transformation, with digital lending emerging as a key driver of financial inclusion. High demand for hasstle-free lending pushes companies to adopt AI risk management and automated processes. Technology is reshaping the whole industry, the companies are bridging financial gaps and providing needs of salaried professionals.

In this article of Recap’24, we spotlight Rupee112, a digital lending platform that redefines how salaried employees manage emergency funds. StartupTalky had the chance to speak with Mr. Vikkas Goyal, Founder of Rupee112, about the company’s mission to simplify borrowing through AI solutions. Its rapid growth across 45 cities, and its efforts to promote sustainability with Green Loans. Goyal lastly shared plans into Rupee112’s expansion beyond metro cities and its commitment to transparency and customer-centric innovation.

StartupTalky: What inspired the launch of Rupee112, and how does it address the financial challenges of salaried professionals?

Rupee112 was inspired by the need to revolutionize financial accessibility for salaried professionals across India. By leveraging cutting-edge technology, the company offers instant access to emergency cash through a seamless, 100% digital, and paperless experience. This approach addresses common financial challenges like delayed salaries, unplanned expenses, and restricted access to credit for individuals with less-than-perfect credit scores.

StartupTalky: Rupee112 has seen rapid growth with over 10,00,000 app downloads and operations in 45 cities. How have your AI/ML-powered solutions contributed to this success?

The AI/ML-powered solutions enable Rupee112 to provide a data-driven, digital-first lending approach. These technologies facilitate faster loan approvals, accurate risk assessment, and personalized solutions, ensuring customer satisfaction and operational efficiency, which have been key drivers of the company’s rapid growth.

StartupTalky: Your lending process is 100% digital and paperless. How does this enhance user experience and simplify borrowing?

The fully digital and paperless lending process ensures a quick and hassle-free user experience. Borrowers can apply for loans through the mobile app, with quick disbursal. This eliminates the need for physical documentation, long queues, and complex procedures, making borrowing more convenient and accessible.

StartupTalky: What are Rupee112’s Green Loans, and how do they promote sustainability while meeting customer needs?

Rupee112’s Green Loans are an initiative to promote sustainability by offering inclusive financing solutions for eco-friendly purposes. These loans support environmentally conscious projects while maintaining the company’s commitment to meeting diverse customer needs in a responsible and sustainable manner.

StartupTalky: What challenges did Rupee112 face while entering the lending space, and how did you overcome them?

Entering the lending space involved challenges like gaining trust in a highly competitive market, addressing regulatory requirements, and building a robust technological framework. Rupee112 overcame these obstacles by ensuring transparency, operating in a regulatory-compliant ecosystem, and investing in advanced AI/ML technologies to streamline processes and establish credibility

StartupTalky: Transparency is a core value. How do you ensure customers fully understand the loan process and avoid hidden fees?

Rupee112 ensures transparency by clearly communicating all terms and conditions upfront, providing a breakdown of fees, and avoiding hidden charges. This commitment helps build trust with customers and establishes the company as a reliable financial partner.

StartupTalky: What marketing strategies have been most effective in achieving rapid growth, and can you share any successful growth hacks?

Rupee112 has focused on digital marketing, app-based promotions, and leveraging AI-driven customer segmentation for targeted campaigns. Growth hacks such as simplifying the loan application process and highlighting the 10-minute disbursal feature have also contributed to driving app downloads and user engagement.

StartupTalky: Does Rupee112 plan to expand beyond metro areas into smaller cities? How do you see the potential of these markets?

Yes, Rupee112 has plans to expand beyond metro areas. Smaller cities offer significant potential due to the underserved financial needs of their populations. By leveraging its technology-driven approach, Rupee112 aims to provide accessible and inclusive financial services in these markets.

StartupTalky:What lessons has your team learned since launching, and how will these shape Rupee112’s future?

Not relevant.

StartupTalky: As a fintech founder, what’s one piece of advice you would like to share with aspiring fintech founders looking to enter the financial services industry?

The key advice is to prioritize customer trust by being transparent and regulatory-compliant while leveraging technology to solve real-world financial challenges. Innovate with a focus on user convenience and always ensure that your solutions are inclusive and accessible.

StartupTalky presents Recap’24, a series of exclusive interviews where we connect with founders and industry leaders to reflect on their journey in 2024 and discuss their vision for the future.

Digital lending market in India is experiencing quick growth, followed by high demand for accessible financial solutions. By 2029, this sector is going to see potential expansion, driven by in AI-driven credit assessments and a shift toward paperless, hassle-free lending experiences.

In this article of Recap’24, we feature BharatLoan, a fintech company revolutionizing digital lending for salaried professionals. StartupTalky had the privilege to chat with Mr. Amit Bansal, Founder of BharatLoan, who shared insights into the company’s growth— simplifying the loan approval process to leveraging AI/ML for great customer experiences. Bansal chatted on BharatLoan’s growth, milestones, and vision for the inclusive financial ecosystem. It includs new offering like Green Loans and self-employed financing solutions.

StartupTalky: What inspired the creation of BharatLoan, and how does it address the financial needs of salaried professionals in metro cities?

Mr. Amit Bansal: BharatLoan was inspired by the need to provide salaried professionals in metro cities with quick access to emergency funds. The platform simplifies the borrowing process through a hassle-free, 100% digital experience, offering loans even to those with less-than-perfect credit scores. By focusing on speed, convenience, and accessibility, BharatLoan effectively addresses the financial pressures faced by this demographic.

StartupTalky: What has been BharatLoan’s biggest milestone in 2024, and what factors contributed to its rapid growth?

Mr. Amit Bansal: BharatLoan’s biggest milestone in 2024 is becoming the fastest NBFC to surpass 1 million app downloads in June and the company has now achieved over 5 million app downloads. This achievement reflects its strong customer adoption, driven by a seamless, 100% digital loan process, an inclusive approach to lending, and leveraging AI/ML-powered solutions to streamline loan approvals and enhance customer experience.

StartupTalky: How does your 100% digital and paperless loan process differentiate BharatLoan from traditional lenders and other fintech platforms?

Mr. Amit Bansal: BharatLoan’s fully digital and paperless process eliminates cumbersome paperwork, long approval times, and complex procedures commonly associated with traditional lenders. Its streamlined app-based approach ensures faster approvals and disbursals, offering salaried professionals immediate access to funds. This innovation sets it apart from other platforms by prioritizing speed, convenience, and user experience.

StartupTalky: What challenges did BharatLoan face while entering the traditional lending ecosystem, and how were they overcome?

Mr. Amit Bansal: BharatLoan navigated challenges such as building credibility in a competitive and highly regulated market, earning customer trust, and seamlessly integrating advanced technologies into traditional lending frameworks. These obstacles were transformed into opportunities through unwavering adherence to regulatory compliance, the creation of a secure and trustworthy ecosystem, and the strategic use of AI/ML technologies to provide faster, more reliable, and inclusive loan services.

StartupTalky: AI and ML play a significant role in your operations. How do these technologies enhance customer experience and decision-making?

Mr. Amit Bansal: AI and ML enable BharatLoan to automate credit risk assessments, provide personalized loan offerings, and ensure faster approvals. These technologies help predict borrower behavior, streamline operations, and enhance customer satisfaction by delivering tailored solutions quickly and accurately.

StartupTalky: What new services or loan categories are you planning to introduce and how do they align with your vision of a sustainable future?

Mr. Amit Bansal: BharatLoan is committed to expanding its portfolio with services that align with its vision of creating a sustainable and inclusive financial ecosystem. Recently, the platform introduced Green Loans, designed to provide affordable financing for solar energy solutions and electric vehicles (EVs). This initiative not only promotes environmental sustainability but also makes renewable energy and eco-friendly transportation more accessible to individuals and businesses, contributing to a greener future.