When it comes to managing expenses and bills, especially when one has low funds. This becomes really pressurizing and people start looking for sources to lend money from. In such situations, borrowing from friends and family could be embarrassing and hectic. And depending upon banks could cost major interests. So where should we look?

Well by acknowledging these situations and deals, online money lending apps are developed. These provide the facility to lend money through digital platforms without any further issues.

Multiple companies are providing the facility of offering loads immediately with minimal competitive interest rates and required tenure durations. These companies facilitate the loan very easily and quickly as compared to usual bank loans.

With keeping such progress in mind, India has developed numerous digital lending companies whose finances can manage smoothly. India is evolving to a great extent in the digital sector and financial inclusion. The country has cash for transactions. But with the evolving method of development and modernization, India is shifting toward a cashless economy. To understand its development more prominently, let’s look at the top 10 digital lending platforms in India.

Best Digital Lending Platforms in India – Lendingkart Website

The prominent digital lending platform, Lendingkart was founded in 2014. It works by offering different capital loans and company loans vary from small to medium-sized businesses across India. They are widely famous for providing capital completely through an online platform and require minimum documentation for the procedure to begin.

For young entrepreneurs, managing their finances becomes quite hectic and it deviates them from focusing on their business growth. That’s why Lendingkart has taken the initiative to make capital funding easily available for entrepreneurs so they don’t have to worry about the cash-flow gaps. Lendingkart is a company established in Ahmedabad, Mumbai and Bangalore. But, its services are accessible throughout the whole of India.

2. Pine Labs

Lending Platform

Pine Labs

Loan Amount

From ₹25,000 to ₹5 Lakhs

Loan Tenure

90 Days

Best Digital Lending Platforms in India – Pine Labs Website

Pine Labs is one of the leading fintech companies in India established in 1998 that provides digital lending services. The company is quite famous for its incredible facility of transforming the mobile NFC into a card machine and activating the service of accepting all types of payment digitally which also includes the ‘Tap n Pay’ card as well.

Pine Labs have brought tons of services for the retailers including multi-channel, different payment options, brand offerings, risk assessments, analytics, and many more.

It provides working capital loans for small to medium businesses. Their loan application process is quite simple and you can apply for a business loan through their website or their app myPlutus.

Pine Labs’ services and technologies are widely preferred and used by more than 100,00 merchants all across India and also, many Asian companies. According to the estimations, PineLabs’ cloud-based technology has the power of over 350,000 PoS terminals; that too in more than 3,700 cities.

3. MobiKwik

Lending Platform

Mobikwik

Loan Amount

Upto ₹5,00,000

Loan Tenure

6 to 36 Months

Top Loan Aggregators in India – MobiKwik Website

MobiKwik is a very prominent mobile payment company that works by connecting the consumers together with the merchants and many online sellers. The company is established in Gurgaon, Haryana, India.

Mobikwik is a private company that has more than 550 employees. Since the establishment of this company, the company has raised a total of 118 million USD from over 8 funding rounds.

Mobiwik provides instant personal loans. You can download its app and once the loan is approved it will be credited to your wallet.

₹1 Lakh to ₹15 Lakhs (unsecured) or up to ₹2.5 Crores (secured)

Loan Tenure

6 to 48 Months (unsecured), Up to 84 Months (secured)

One of the biggest lending companies, Shiksha Finance, is an education-based finance firm. Shiksha Finance provides the services of funding parents for school fees by reducing the school drop-out rates. It also offers capital to educational institutions for the development of buildings, properties and working capital.

Shiksha Finance has loans that range from INR 10,000 to INR 50,000 with a return duration of 6 to 10 months. The loans which Shiksha Finance provides can be utilized for educational based purposes such as school fees, tuition, luggage and stationary.

5. MoneyTap

Lending Platform

MoneyTap

Loan Amount

Upto ₹5,00,000

Loan Tenure

36 Months

Best Digital Lending Platforms in India – MoneyTap Website

The Bengaluru based lending company, MoneyTap is known for its huge service of offering credit lines for the consumers as their loans, with the partnership with RBL Bank. MoneyTap is now counted among the leading lending businesses. Recently, the company received the license of NBFC for co-lending space together with their lending partners.

MoneyTap has offered many great features among which, the minimal documentation procedure for a personal loan is the most special one. Moreover, its app version also provides the facilities for tracking down your borrowing records.

6. Paytm

Lending Platform

Paytm

Loan Amount

Upto ₹2,00,000

Loan Tenure

6 to 36 Months

Fintech Lending Companies in India – Paytm Website

The biggest digital lending wallet company Paytm is wildly famous in the minds of Indians. The company is established in Noida, Uttar Pradesh. Paytm has grown to a great extent and now, millions of downloads have been made.

The development the company has received is breathtaking. It employs more than 9000 people and has a revenue of a total of $118 million. Paytm is highly specialised in online shopping as well.

Best Digital Lending Platforms in India – PolicyBazaar

The company is counted among the top leading online insurance companies, PolicyBazaar was established in the year 2008 and headquartered in Gurgaon, Haryana, India.

It is online life insurance as well as a general insurance aggregator company. PolicyBazaar is very popular among Indians for its incredible services and holdings. It employs over 2500 people and has an annual revenue of $21 million (as estimated in 2017-18).

The current CEO of PolicyBazaar is Yashish Dahiya who is also one of the founders of this company. It has raised around US$ 346 million through 7 funding rounds.

8. Capital Float

Lending Platform

Capital Float

Loan Amount

₹50,00,000

Loan Tenure

Upto 36 Months

Best Digital Lending Platforms in India – Capital Float Website

Capital Float is one of the leading lending companies in India. It is acquired by CapFloat Financial Services. Capital Float is popular for its amazing service of specialised financial loans and business credits.

Capital Float has a partnership with some prominent companies such as Shopclues, Paytm and Uber. The company lends the potential borrower through its system of proprietary loans. Capital Float is now targeting established store owners and small merchants.

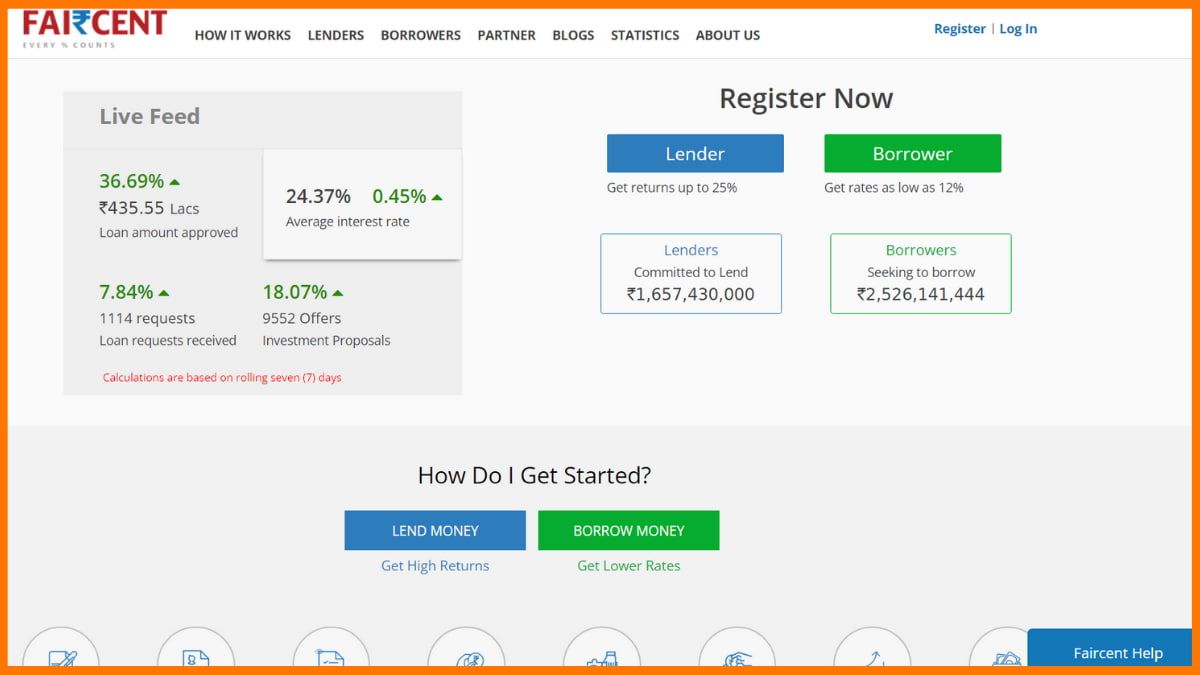

9. Faircent

Details

Information

Loan Amount

₹5,00,000

Loan Tenure

6 to 36 Months

Best Digital Lending Platforms in India – Faircent Website

The largest and first Indian peer-to-peer digital lending platform, Faircent is known to be absolutely amazing. It is officially registered by the RBI. It provides a safe marketplace for people to loan money to a borrower. Faircent facilitates the credit to organizations and individuals who are interested in lending money.

Faircent provides the absolutely convenient procedure of lending the required money to those who need it, at reasonable interest rates.

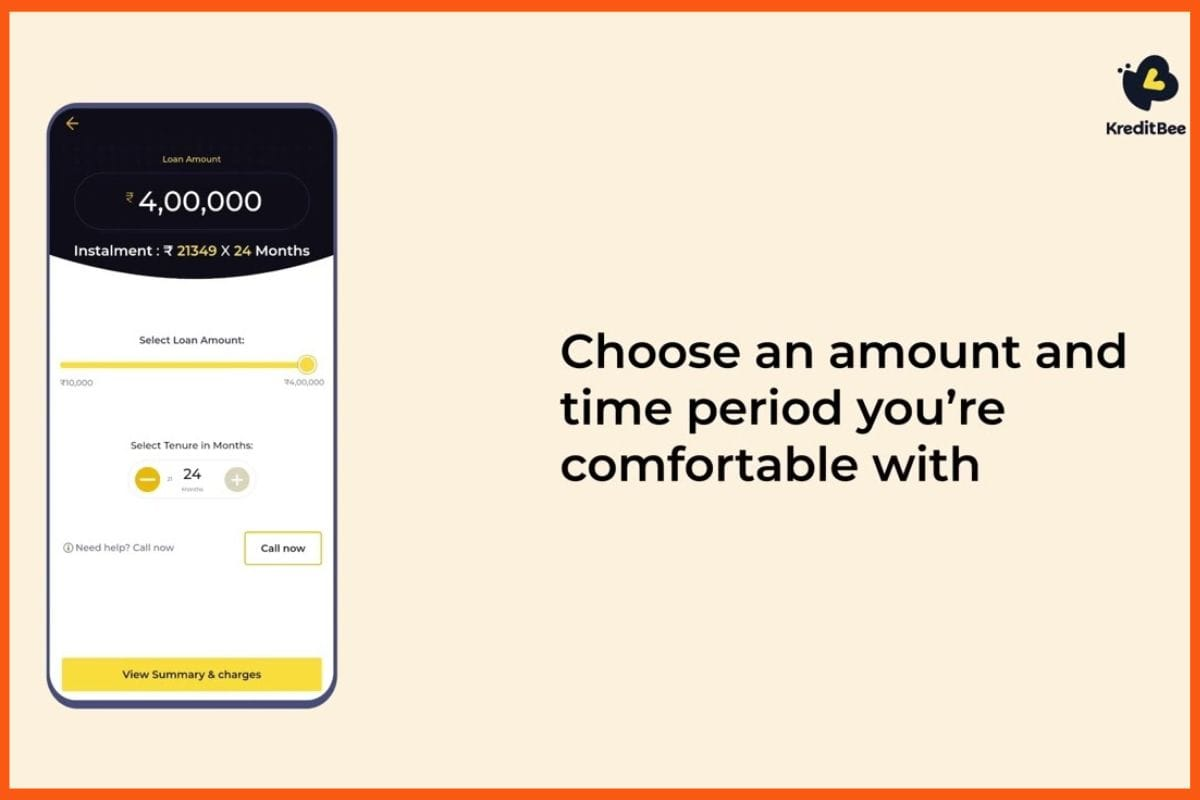

10. KreditBee

Lending Platform

KreditBee

Loan Amount

₹5,00,000

Loan Tenure

6 to 36 Months

Lending Service Providers in India – KreditBee

KreditBee is a Bangalore-based fintech that offers quick personal loans up to INR 2,00,000 for working professionals. Using easy online KYC, the loan process is fast and simple. KreditBee is one of the top lending companies in India.

Backed by trusted investors like ICICI Bank and supported by banks like AU Small Finance, KreditBee serves over 5 million customers.

The process is mostly paperless, sign up on the app, and within 15 minutes, approved loans are transferred instantly to your bank account.

In India, there are many fintech companies that are providing the service of digitally lending money very easily with the minimal documentation procedure. Today, many apps have been developed by these companies to make the transaction of money absolutely susceptible. And for those who require a personal loan or business loan, can easily get one. That’s why we listed these top digital lending companies in India.

FAQs

What are some of the top digital lending companies in India?

Lendingkart, Pinelabs, Mobiwik, Policybazaar, and Paytm are some of the top digital lending companies in India.

How does a lending company work?

Lending companies provide loans to an entity, which is then expected to repay its debt.

How many fintech companies are there in India?

There are around 2,000 fintech companies in India.

Company Profile is an initiative by StartupTalky to publish verified information on different startups and organizations. The content in this post has been approved by Karza Technologies.

Non-performing assets (NPAs) and frauds have been plaguing Indian banks for the last several years. In 2021, the total amount of non-performing assets held by Indian public sector banks was approximately 6.17 trillion Indian rupees. However, as of March 2022, the percentage of gross non-performing assets in the banking sector fell below 6%, which is the lowest it has been since 2016, and bank loan frauds stood at INR 58,303 crore in FY22.

Karza Technologies has stepped in with big data analytics, business intelligence, and machine learning to carry out background checks and assess the creditworthiness of borrowers not just on their track record but also on their future potential and intent to repay. Karza is building an intelligent system that analyzes available financial information from the institutions and trawls the internet for lurking signals that will raise a red flag about the creditworthiness of the borrowers. Recently, in February 2022, this fintech startup was acquired by Perfios Software Solutions.

In this article, know about Karza Technologies, it’s business and revenue model, products and services, founders, startup story, and more.

Karza strives to be a one-stop solution for the financial services ecosystem. Karza is an analytics and automation platform that aggregates and stitches information from 850+ public databases to meet service automation, onboarding, due diligence, and monitoring requirements for the BFSI sector. Their services permit the seamless onboarding of customers and the mitigation of risks, allowing for a better assessment of any customer type, be it individual or entity.

Karza began providing its business intelligence, AML screening, KYC verification, and other services with a view to preventing systematic fraud through consistent innovation in the service of the larger public good. It has so far been successful in its stated objective of reducing fraud, having successfully prevented losses of over 2,500 crores by weeding out bad applications at the outset. It has also greatly simplified the customer onboarding process, with myriad solutions for KYC verification, including VideoKYC.

It is now acknowledged as being one of the preeminent KYC and business intelligence service providers in the country and has 400+ banks, insurance companies, and financial institutions dependent on its services to protect against identity theft, comply with AML and other regulatory obligations, and conduct customer due diligence and enhanced due diligence on their clientele.

Karza Technologies – Industry

The fintech market in India is a rapidly growing industry that encompasses a wide range of financial services and technologies. This includes areas such as mobile payments, online lending, digital banking, insurance, and investment platforms.

Digital lending includes services such as online personal loans, business loans, and other types of digital lending. Other important segments in the Indian fintech market include insurance, investment and wealth management, and blockchain technology.

As of FY2021, the fintech market in India was valued at INR 2.48 trillion. It is projected to reach a value of INR 9.27 trillion by FY2027, growing at an annual rate of around 24.96% during the period between FY2022 and FY2027.

Overall, the fintech market in India is expected to continue growing in the coming years, driven by increasing demand for digital financial services and the government’s efforts to promote digital financial inclusion.

Karza Technologies was founded by Omkar Shirhatti, Gaurav Samdaria, and Alok Kumar.

The co-founders, Gaurav and Omkar, knew each other from their college days, as they had pursued their graduation and chartered accountancy together, after which they took up different jobs. They are level-headed individuals with an enterprising mindset and a penchant for white-collar investigations. Omkar and Gaurav often engaged in conversations about their experiences with the BFSI sector and were struck by the massive gaps that could be filled by data-led, deep-tech approaches.

By March 2015, both Gaurav and Omkar had a fairly structured idea about the way forward, as they had already begun interacting with market stakeholders. Both had to quit their jobs, and the company was incorporated in June through personal investments. However, they were two chartered accountants who were starting a tech company and were in search of a tech expert.

The next challenge was to find a suitable developer. By reaching out to Gaurav’s friend circle, they were able to find some leads to begin the hunt for a tech co-founder, wherein close to 200 to 250 people were personally interviewed by Omkar and Gaurav. They narrowed down their search and found Alok, who has a Master’s in Computer Science from IIT Kharagpur and had been working with Morgan Stanley. He was part of a 7-member global elite team that was working on global tech data, AIML projects, wire transfer frauds, and transaction pattern recognition to detect wire frauds and anomalies, etc.

They discussed the overall vision of Karza and the scale of the operations, including the complexities of profiling millions of businesses, detecting shell entities, and other AI, ML, and data science-related use cases. This excited Alok immensely, and he decided to take up the opportunity, put his Ph.D. and advanced learning dreams on the back burner, and come on board as a co-founder and CTO at Karza.

Omkar Shrihatti

Omkar Shrihatti – Co-founder and CEO at Karza Technologies

Omkar serves as the co-founder and CEO of Karza Technologies and also as the Chief Product Officer at Perfios (Karza Technologies’ parent company). Before co-founding Karza Technologies, Omkar Shrihatti served as a senior consultant at Ernst & Young, a global leader in assurance, tax, transaction, and advisory services. He has over 12 years of experience in the fields of fraud investigations, background checks, and so on.

Gaurav Samdaria

Gaurav Samdaria – Co-founder, Director at Karza Technologies

Gaurav is the co-founder and Director of Karza Technologies and Chief Business Officer at Perfios. Previously, Gaurav served as the co-founder and Director at Schbang Digital Solutions, an integrated marketing solutions agency. Prior to that, he worked as the Chief Financial Officer at M/S FoxyMoron, a marketing and advertising firm.

Alok Kumar

Alok Kumar – Co-founder, CTO at Karza Technologies

Alok is the Co-Founder and CTO at Karza Technologies. After completing his master’s from IIT Kharagpur with a focus on machine learning and big data, Alok specialized as a data scientist for Morgan Stanley for over three years, working on mining/natural language processing (NLP), and fraud detection.

Karza Technologies – Startup Story

The idea behind Karza stemmed from conducting investigations at our previous workplaces. Having worked with global consulting firms such as EY, their focus had been on fraud investigation, during which they identified several gaps in the processes followed by the BFSI sector. They were investigating loan frauds, hawala transactions, security market frauds, conducting market surveys, due diligence, etc., which gave us insights into identifying how money gets siphoned off in fraudulent transactions, how hawala and money laundering work and the way shell companies are floated, etc.

They did a lot of secondary research to identify, piece together, and gather all the scattered information to understand how Karza could solve problems with its data-first approach. While investigating loan frauds, they realized that banks used a lot of manual processes, which led to inefficiencies and were not able to keep pace with the technological advancements in the sphere. Even though the government had already begun to take huge strides in digitization, promoting their vision of a digital India, banks were unable to effectively capitalize on the opportunity with their existing resources, and their processes largely remained manual.

The inspiration came from the above-mentioned scenario, where they realized the power of leveraging technology to build solutions where intelligent information relevant to an entity can be searched and profiled based on various official sources.

Initially, they were able to meet people in the industry due to the social circle of their partners. Some of the interactions were instrumental in creating their first products. From the smallest cooperative banks to large PSUs, private sector banks, etc., they were all pivotal in helping them understand how to build robust products that cater to the BFSI segment. The initial set of clients came in through conversations at BFSI summits and conclaves, where the need for their solutions was immediately recognized, giving us a head start.

Karza Technologies – Name, Tagline, and Logo

Karza Technologies Logo

The name ‘Karza’ came into their focus as it was catchy and roughly translates to ‘lending‘ in several Indian vernaculars. They were looking for names that could be relatable and easily remembered. They reckoned that as a company that provides money-lending technologies, they must keep it simple and go ahead with ‘Karza’, a term specific to India.

Their aim was to revamp how consumers approach BFSIs and the overall journey to get a loan and to revolutionize the lending process by automating every aspect of it. This way, the name will be associated with a service that smooths this process.

Karza Technologies – Mission and Vision

They are now exploring other avenues to expand into, with a continuing focus on the BFSI sector. Karza Technologies is constantly innovating and looking to build products that can increase credit access and availability and, among a host of other things, is looking at the NBFC Account Aggregator framework, the creation of workflows, and improving our analytics and scoring services.

The traditional BFSI ecosystem has various limitations that make organizations slow, inefficient, and unable to service rising demand:

Scattered and Unstructured Data:

Data is scattered across the web and not available in a consumable, intelligent manner.

Evidenced by multiple licensing requirements, high requirements for statutory and compliance filings, several state-level regulatory bodies, and regional language portals.

Lack of credible intelligence also hinders the ability of institutions to service smaller and newer credit customers, inhibiting financial inclusion.

Manual Processes:

Processes such as onboarding, verification, and collection of data, when undertaken manually, have a high turnaround time and lead to huge operational costs.

Moreover, these processes are prone to error and/or manipulation and can lead to fraud and misappropriations remaining undetected.

Karza Technologies endeavors to eliminate these inefficiencies by harnessing the power of big data and AI to provide automated, scalable, and customizable solutions, enabling the digital transformation of businesses. They provide a multitude of services applicable across the lending lifecycle and to different industries.

They started with commercializing Total KYC, onboarding, and the verification suite. Karza Technologies adopts the principle of research-driven innovation to constantly roll out updates, improvements, and new features to its services. Over the course of their research, they also found a need in the market for a product that would allow enhanced due diligence to be carried out effectively and a need to increase access to credit for SMEs. Accordingly, they have built a due diligence platform, KScan, that enables them to conduct due diligence on all business entities registered in India, including identifying litigation filed against these entities.

They supplemented this with our GST and Income Tax solutions, which enable banks to effectively assess the credit risk of lending to SMEs. Most recently, they have gone live with their skip tracing solutions, improving the contact ability of defaulters and improving recovery rates for financial institutions.

Karza Technologies combines human and artificial intelligence through a research-driven development process to create products that address the gaps in the BFSI sector, payment companies, and larger corporates. With data collected from 800+ publicly available sources, they combine alternate data sets to provide maximum insights that no other player in the market can currently provide.

Karza Technologies – Business and Revenue Model

Karza Technologies is a B2B Software-as-a-Service (SaaS) company and works closely with various players across a multitude of industries, including lending, insurance, payments, corporates, law, investment, and several others. Their services are consumed both in the form of APIs that directly integrate with the core banking systems for large players in financial services and in the form of consumer-friendly dashboards that make the consumption of information as easy as possible.

The pricing will vary from product to product and be based on the level of customization required by clients. On account of the highly customizable nature of our solutions, they do not have fixed pricing models. They also offer batch modules for their clients so that they can directly share their insights in the form of reports.

Karza Technologies – Startup Launch

Their initial response from potential clients was positive, as the clients were in dire need of the sort of products that Karza was building. However, the onus was on Karza to prove its mettle and deliver working prototypes, EPIs, etc. that would lead them to use Karza for their business functions. For starters, Karza had to start small by packaging micro-services and catering to the first customers through the initial connections.

Later on, growth was solely through word of mouth. They ended up revamping or digitizing processes for several organizations, with the first year and a half going into researching, identifying resources, and offering offline reports. Furthermore, eliminating fraud was a serious concern for banks, as they weren’t getting the right sort of intelligence for processing the loans seamlessly.

Karza Technologies – Marketing Strategy

In the year 2017-18, there were 32 clients, 66 clients by March 2019, and crossed the 100 client milestone in October 2019, reaching a total of 142 clients by March 2020. This was achieved only by the word of mouth alone, as clients were extremely satisfied with the utility of the products that were being delivered. Now, the platform boasts of having 400+ clients.

Karza spent zero money on marketing and PR until June 2020. They were getting all their leads from existing client referrals; it was completely word-of-mouth. This speaks a lot about the utility and advanced products that Karza has to offer. They fulfill market demand by being a one-stop solution for the entire lending transaction cycle. However, for the next phase of growth, their focus could be on building better marketing and branding strategies now that Karza has managed to make a name for itself in the financial sector.

The NBFC-Account Aggregators ecosystem is improving, which opens up new opportunities for Karza. Entities weren’t able to look into banking analytics earlier; however, through public information sources, a proper official channel can be merged with external intelligence, making the lending process even faster. India has always been a credit-hungry country, and there will be enough space for Karza to expand its presence and build the necessary onboarding and due diligence infrastructure in the long run.

Karza Technologies – Funding

Karza Technologies has raised a total funding worth $1.1 million in over two rounds.

Date

Round

Amount

Lead Investors

Jul 1, 2019

Series A

$750k

–

Jun 21, 2017

Seed Round

$388.5k

–

Karza Technologies – Recognition and Achievements

Recognized as Top25 startup in India to work with, in 2019 by LinkedIn

Winner of HDFC Bank’s Digital Innovation Summit 2020

Super Winners (Won every category) at Technoviti 2020 by Banking Frontiers

Winner of Amazon AI Award 2019 for Fintech

Winner of FinTech Spot Pitches at Fintegrate Zone 2018 held at BSE

Winner of the FinShare 2018 challenge held by ShareKhan

Maharashtra start-up week- Winners- August 2020

Karza Technologies – Challenges Faced

Like every other startup, Karza too has gone through ups and downs during its overall business cycle, as it has had to be cognizant of cash flows. With minimal balances, they initially faced challenges in managing resources to pay off employees and run the organization in parallel. However, the intention was always to be profitable and build a sustainable business rather than go after the valuation game, and they have since been cash-flow positive.

There were challenges also with banks when Karza tried to crack it through. They started with fintech companies, who were the early adopters of our offerings, as they could discuss the services and their applicability openly with the founders and make the right kind of propositions. Later on, they reached out to slightly larger NBFCs, which often had centralized decision-making and a close-knit setup because they would have a single product or offering, which made communication easier. However, with banks, they realized that getting through to them would be tough, as it could take several months or a year to close an agreement with them.

Well-known banks often expect major partnerships while participating in large-scale RFPs, and these challenges can be overcome with time. Karza had gone through a learning curve in the initial months, trying to understand how to bid on RFPs and mature as an organization.

Their other aim is to be cash-rich and maintain healthy liquidity. On the business decision front, the challenge has been getting the right talent. Bangalore is leading the country in terms of producing top-quality tech talent, and attracting the best tech workers to Mumbai was the biggest hurdle. It took two and a half years for them to get the first 20 people on board. In 2018-19, they got 20 more techies, and 40 more in 2019-20. Therefore, getting highly motivated and talented tech experts has always been challenging.

Karza Technologies – Competitors

Some of the competitors of Karza Technologies are:

Karza Technologies is the partner of choice for 400+ clients across banking, lending, payments, insurance, investments, and commerce for digitization, verification, and diligence, including all four credit bureaus, processing over 10 million transactions per month.

Their APIs are integrated with 40+ workflow providers and cover all leading LOS players. Their top clients include Google Pay, Cash Bean—a digital lender—IDFC First Bank, Bajaj Finance, and ICICI Bank, among others. While their only office is based in Mumbai, they work with clients situated across India, from large cities to even rural communities.

Karza Technologies continues to create solutions that transform the consumption of BFSI solutions. Their future plans include expanding and enhancing their existing product suite with additional data, investing in technologies such as advanced natural language processing and computer vision to strengthen their analytics offerings, and building automated solutions for partners.

FAQs

What does Karza Technologies do?

Karza Technologies provides business intelligence services to transform the ways financial institutions lend money. It takes care of the complete lifecycle, from onboarding to diligence and monitoring to collection.

Who founded Karza Technologies?

Karza Technologies was founded by Omkar Shirhatti, Alok Kumar, and Gaurav Samdaria.

Who is the CEO of Karza Technologies?

Omkar Shirhatti is the CEO of Karza Technologies.

How much funding has Karza Technologies raised to date?

Karza Technologies has raised $1.1 million to date.

When was the last funding round for Karza Technologies?

Karza Technologies’ last funding round took place in July 2019 from a Series A round.

Which company has acquired Karza Technologies?

Perfios Software Solutions has acquired Karza Technologies for INR 597 crore.

This article is contributed by Sanjay Sharma, MD, Aye Finance.

Getting a loan is something that bothers everyone with all the formalities and paperwork. But 2021 being the FY that has seen a financial crisis for various sectors, has been some or the other way boosted by various fintech companies that have helped them to manage and survive their businesses. Amongst various fintech companies, there are a few companies that made lending easy and hassle-free.

With $1 billion of loans disbursed to around 1.3 lakh MSMEs across India since its inception, Lendingkart has been growing rapidly in MSME financing and one of the major reasons for this is its credit intelligence platform. Lendingkart’s proprietary underwriting model has been instrumental in providing credit sanctioned loans to 250k loans over the past 6 years but it is important to understand how it is being utilized by the firm itself.

Aye Finance

Aye Finance – Lending Institution

Aye Finance founded by Sanjay Sharma MD is a commercial institution built around the mission to solve these challenges of funding MSMEs and enabling their inclusion into the mainstream of the economy. Aye Finance is equity-funded by three reputed Venture Capital Funds – Accion International, SAIF Partners, and LGT Impact ventures. It also has over a dozen providers who extend their debt funds for its MSME finance business. Aye offers Rs 1-3 lakhs line of credit for working capital to microenterprise owners who typically have sales of INR25-50 lakhs annually.

Aye has successfully enabled the inclusion of 3 lakh micro enterprises having disbursed over Rs 4,000 crore to them.

Ziploan is a tech-enabled RBI registered NBFC that provides loans to small businesses. The platform addresses the need of the SME sector, which has been ignored by financial institutions. The platform generates a unique ZipScore for each loan applicant by developing an automated underwriting algorithm.

Satya MicroCapital

Satya MicroCapital – Lending Company

Satya MicroCapital Limited is an NBFC-MFI that serves low-income entrepreneurs in rural and urban areas. The company provides prompt, convenient, and affordable collateral-free credit to unbanked and underserved people through a strong credit assessment and centralized approval system. Satya MicroCapital’s firm belief in modern technology and its potential to increase efficiency, reduce risks, and enhance the overall customer experience is apparent in its adoption of cutting-edge innovations to power its operations.

NeoGrowth is an SME lending platform, registered with the Reserve Bank of India (RBI). The NBFC’s approach includes innovative technology and a digital payment ecosystem along with flexible repayment options. NeoGrowth aims to bridge the credit gap for MSMEs by offering customized products to address customers’ multiple business needs.

Save Solutions Pvt. Ltd.

Save Solutions – Lending Company

Save Solutions Pvt. Ltd. is one of the country’s largest Business Correspondent Networks. The Bihar-based company is focusing on giving access to Financial Products via kiosk banking and customer service points (CSPs) to rural and semi-urban unbanked citizens. Expanding rapidly, the SSPL group has roots across India in 488 districts, with over 12,000 kiosks in rural areas. The company employs over 25,000 people across these locations at its Customer Service Points (CSPs) and Kiosks. All the employees are provided training in computer and cash management systems to improve client enrolment and service delivery, thereby helping improve Save Solutions’ overall service performance.

InCred is a new-age financial services group founded with the vision of providing credit to Incredible India and thus, furthering financial inclusion in the country. The company endeavors to disrupt the status quo in traditional lending that seems to exclude those most in need of credit, due to outdated, rigid, and often inefficient processes. The company has designed its products with a razor-sharp focus on serving the unique needs of these under-served segments of customers and leverages technology and data science to make lending quick, simple, and hassle-free. It aspires to be the key partner for all financial requirements of an Indian family.

Founded in the year 2016 by Bhupinder Singh, former head of Investment Banking Deutsche Bank Asia-Pacific, the company launched market operations in January 2017. InCred offers a broad portfolio of products that cut across key categories such as Personal Loans, SME Loans & Education Loans.

Company Profile is an initiative by StartupTalky to publish verified information on different startups and organizations. The content in this post has been approved by Credit Fair.

Credit Fair is a consumer lending fintech startup that provides 0% or low-cost, short-term, unsecured installment loans at the point of sale. The startup’s unique credit assessment process has helped it achieve a quick turnaround time (TAT) of less than a day and a high approval rate, enabling more Indians to avail credit. Apart from that, Credit Fair helps borrowers build a credit ladder, i.e. a credit score to help them access credit from other lenders and at a fairer rate. In just 3 years, Credit Fair managed to onboard over 1,000 merchants including upGrad, Toppr, Asian Paints among many. It has disbursed about $9 million to date with a loan book of $4 million currently.

StartupTalky interviewed Mr. Aditya Damani (Founder of Credit Fair) to get insights on the startup story and roadmap of the organization. In this article you’ll discover how Credit Fair was conceptualized, its business model, growth, funding, future plans, and more.

Credit Fair provides 0% or low-cost, short-term, unsecured installment loans at the point of sale. The short-term vision of the company is to be the preferred lender in sectors of education, healthcare, home décor, and electric vehicles. Its long-term vision is to see every Indian have access to the right amount of credit at the right cost and at the right time.

By 2025, the startup aims to positively impact the financial lives of over 1million Indians. This vision reflects in its efforts to enable low-cost loans for ‘Bharat’ i.e. people who are not served by banks and large NBFCs. Over 70% of Credit Fair’s loans are No Cost EMIs, hence offering better terms than even personal loans from banks.

Credit Fair – Industry Details

According to a report by BCG, the total value of digital lending is expected to be $1 trillion by 2023, driven by increased access to the internet and smartphones and increased digital purchases. As for the number of customers, 550 million people i,e, 46% of the population of India is currently underserved and makes up for the total addressable market.

Credit Fair has estimated the market opportunity in its target sectors – health, education, solar rooftop, and electric vehicles to be over $20 billion of which 25% is funded by EMI taking its immediate addressable market to $5bn. These sectors are fragmented but large and experiencing a high growth rate, making them attractive.

The founder got the inspiration of starting a lending business in India while working at new to credit-focused lender, Oakam, and while advising private equity funds on setting up lending businesses. He saw people face issues rejections or delays in getting credit from financial institutions during critical life moments such as medical emergencies leading to reliance on informal channels that charge usurious interest of 10% per month and getting trapped in a debt cycle. This led to the idea of launching Credit Fair.

Credit Fair – Product/Service and USP

About 550 million Indians are underserved by traditional lenders because they are new to credit (NTC) or do not have a prime credit score

Availability of credit at the point of sale is currently enabled through credit cards, penetration of which is less than 4%

Borrowers in remote areas are also underserved by traditional banks due to the high costs associated with their onboarding, management, and recovery.

Hence, there is a huge demand for formal credit that can be availed through simple processes.

On the other hand, merchants, who are majorly SMEs, struggle with providing a point of sale financing options to their customers resulting in loss of potential sales. Second, their operations are mostly based on cash transactions, leading to process inefficiencies and high transaction costs.

Credit Fair provides 0% or low-cost, short-term, unsecured installment loans at the point of sale. Itsticket size ranges from USD150-25,000 and tenure from 3 months to 3 years.

The startup’s unique credit assessment process has helped it achieve a quick turnaround time (TAT) of less than a day and a high approval rate, enabling more Indians to avail credit. Second, by providing 0% or easy EMI, it is increasing access to low-cost credit hence, securing the financing health of the borrowers. Third, Credit Fair also helps borrowers build a credit ladder, i.e. a credit score to help them access credit from other lenders and at a fairer rate.

Credit Fair – Consumer App

As for merchants, Credit Fair’s products and high TAT and approval rate help improve conversions and ensure stable cash flows for the partners, hence, overcoming the issues of low sales and lack of working capital. Second, digitizing cash flows will help merchants manage their cash flows better leading to efficiencies in operations. Finally, it will further the startup’s mission of financial inclusion as SMEs will be able to access credit and working capital loans, based on cash flows generated as a result of partnering with Credit Fair.

Credit Fair – Founders and Team

The founder, Aditya Damani, has a unique mix of fintech and institutional lending experience, having received a Banking Tech award while at new to credit-focused lender Oakam and TransferWise previously. He has also worked at PIMCO and advised private equity funds on setting up lending businesses.

Credit Fair – Founding Team

The team comprises over 50 members covering technology, credit, collections, sales, finance, and marketing functions. The team is young and shares a passion for the mission of the company as demonstrated through the values of ownership, curiosity, and obsession with customer satisfaction.

Credit Fair – Business Model & Revenue Model

Credit Fair follows a B2B2C business model. It is offering a win-win proposition to both merchants and customers by providing 0% or low-cost, short term, unsecured installment loans at the point of sale. The interest costs of these loans are borne by the merchants to attract new customers while the borrowers seek installment facilities to manage their finances. In addition, the borrowers bear a nominal processing fee and in some cases insurance fee as well.

Credit Fair – Startup Launch

It started with acquiring partners in the home décor sector through forming connections over LinkedIn and through cold calling. Because this sector was not actively served by big players such as Bajaj, the founders recognized an opportunity to develop expertise within the sector and provide products and processes suitable for customers within the home décor segment. That helped Credit Fair become the preferred lending partner in the home décor segment. Soon after they targeted the elective healthcare sector that also was vastly underserved by existing players.

The team focused on serving their partner merchants better than the competitors by providing better approval rates, faster turnaround time, and competitive pricing. That has been a key factor in retaining partners and capturing a bigger share of their wallets as well as getting recommendations from existing partners to form new partnerships.

Credit Fair – Challenges Faced

One major challenge that Aditya faced is – Aligning the different teams within the company to focus on the company goals while managing risk. He often observed that the different teams such as credit, operations, collections, etc. would have their team goals which often wouldn’t add to the company’s growth or would be contradictory to the goals of other departments.

One tool, that has been very effective to achieve team-company alignment is setting OKRs. The founders set company OKRs (Objectives & key Results) and based on it, each team lead has developed team OKRs. This has helped them identify key metrics for individual teams that together contribute to the company’s growth. The OKRs are reviewed quarterly and have been effective to give direction to all team members.

Credit Fair – Funding and Investors

Credit Fair has raised a total funding of $15mn, details are as follows –

Date

Stage

Amount

Investors

June 2021

Seed

$15 Mn (Debt + Equity)

Equity – Anand Ladsariya and Alok Agarwal; Debt – Undisclosed

Credit Fair – Advisors/Mentors

Credit Fair’s board of advisors comprises of C-Suite from companies such as HDFC, IFC, PayU, and IBM.

Among large lenders, Bajaj Finance is its primary competitor. Among fintech lenders, Credit Fair’s competitors include companies such as Liquiloans, EarlySalary, ZestMoney, and Eduvanz.

Credit Fair – Tools used to run startup

The startup uses Slack for team communications, OKRs for goal setting and tracking, Jira for sprint planning in addition to using third-party services for managing certain business operations.

Credit Fair – Current Growth & Future Plans

Credit has onboarded over 1,000 merchants including upGrad, Toppr, Indira IVF, Pristyn Care, Toothsi, Asian Paints, and Ampere.

It has disbursed about $9 million to date with a loan book of $4 million currently.

The startup’s month-on-month growth rate is 15%.

Credit Fair was selected to be part of Village Capital’s Finance Forward: India 2020 cohort.

In the next two years, Credit Fair aims to establish partnerships with 5,000 merchants, reaching $15 million monthly disbursements. It is building its products to reach a $15M monthly disbursement rate and $75M Assets under management in 2 years. The funds will be used towards providing loss guarantee, expanding team, and marketing. It also plans to launch a P2P lending platform to further lower its cost of funding, hence keeping costs low for its customers.

Credit Fair – FAQs

What is Credit Fair?

Credit Fair is a fintech startup that provides 0% or low-cost, short-term, unsecured installment loans at the point of sale.

What is Credit Fair’s Business Model?

Credit Fair follows a B2B2C business model. It is offering a win-win proposition to both merchants and customers by providing 0% or low-cost, short-term, unsecured installment loans at the point of sale.

How much funding has Credit Fair raised?

Credit Fair has raised total funding of $15mn (Equity + debt) from Anand Ladsariya and Alok Agarwal.

Is Credit Fair an Indian Company?

Yes. Credit Fair is an Indian company headquartered in Mumbai.