This article has been contributed by Manish Goyal, Chairman and Managing Director at Finkeda

The peaceful villages and fields of rural India are gradually being disrupted, altering a way of life that has existed for hundreds of years. For so long, businesses in these areas were either reliant exclusively on the feel of crumpled rupees or the trust that came from a handshake. The old way of banking, which often involved filling out long, complicated forms or going to branches that were so far away that it seemed impossible, was very difficult. But today, thanks to a powerful wave of digital transformation driven by pricing and government ambition, barriers are being broken down. This story is about how banking is moving from physical locations to the palm of your hand, bringing millions into the official economy and creating a future where financial inclusion is a basic right, not just a luxury.

The Foundation of a Digital Economy

The success of digital banking in rural regions relies on three key elements: Jan Dhan, Aadhaar, and Mobile, often called the JAM Trinity. The Pradhan Mantri Jan Dhan Yojana (PMJDY), started in 2014, aimed to give a bank account to every adult who didn’t have one. These “zero-balance” accounts allowed millions of people to join the formal financial system for the first time. The Aadhaar system provided every citizen with a digital identity, making it easier to open an account without needing a lot of documents. Plus, the fact that mobile phones are available even in faraway villages helped a lot. Together, these three things created a system where people could open a bank account just by using their fingerprints and get banking services from a nearby agent, making banking available to everyone.

UPI and AePS

The most noticeable part of this change is the rise of digital payments. The Unified Payments Interface (UPI) is a system that lets people transfer money instantly between bank accounts using an easy mobile app, and it has become super popular. The effectiveness of UPI lies in its simplicity. To transfer or receive money, users just need a mobile number or a unique UPI ID, which cuts out the hassle of complex account numbers and codes. Now, making digital payments is as straightforward as sending a text message. For instance, a farmer can now get paid for their crops directly into their bank account with just one click, and a small shopkeeper can take digital payments from customers using a QR code. The number of UPI transactions has increased a lot, showing how widely accepted it is in rural areas.

Another thing to note is that the Aadhaar-enabled Payment System (AePS) complements UPI by providing essential financial services to those without smartphones or internet. It allows users to carry out simple banking activities like cash withdrawals or balance inquiries using their Aadhaar number and a fingerprint scanner. Local helpers, called Bank Mitras, use these user-friendly devices to offer a mini banking experience right at the doorstep of villagers. This technology is particularly beneficial for seniors or anyone who finds reading and writing challenging, as it spares them from navigating complex digital platforms.

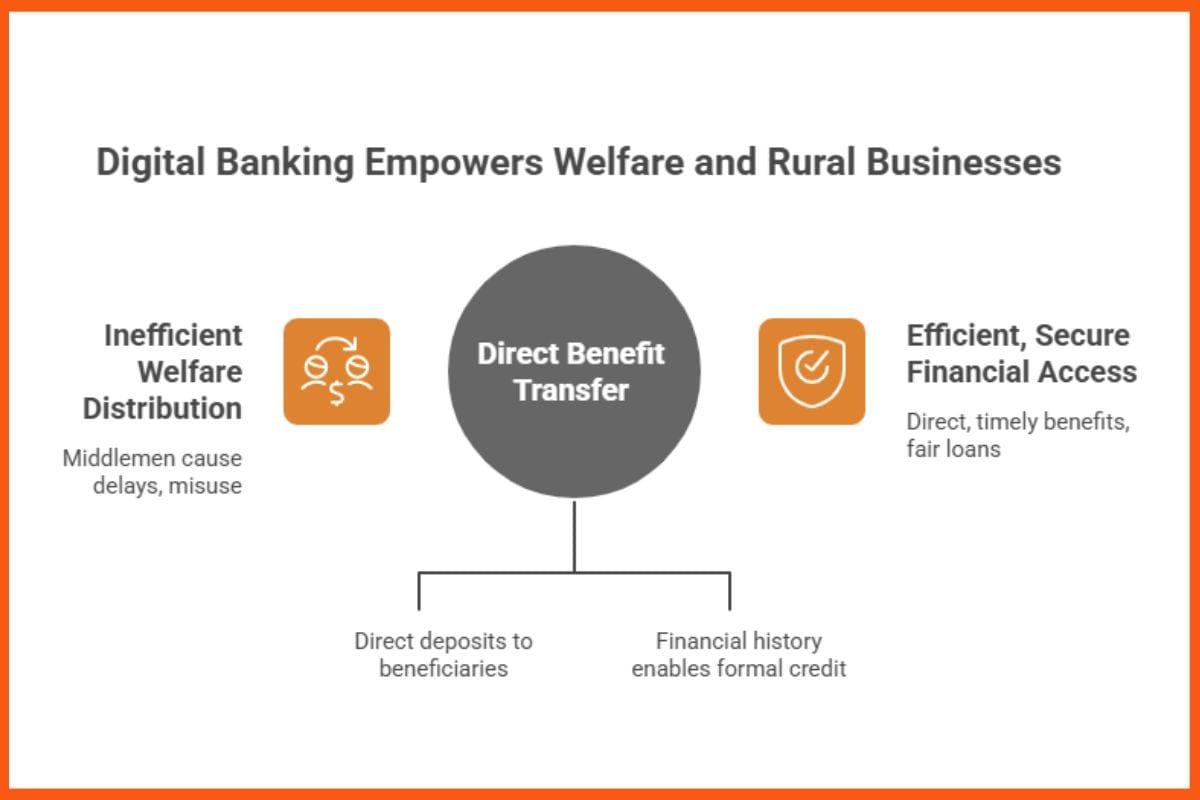

Digital Banking Empowers Welfare and Rural Businesses

The shift to digital banking has completely transformed the way the government manages welfare programs. The Direct Benefit Transfer (DBT) system allows government assistance and benefits to be deposited directly into the bank accounts of those in need. In the past, this money usually passed through a lot of middlemen, which led to delays and sometimes even misuse. Now, by directly sending money to the bank accounts created under PMJDY, the government has made the process easier and more efficient. This means that a farmer’s crop subsidy, a senior citizen’s pension, or a student’s scholarship is received completely and on time. This easy way of transferring money has not only helped the government save money but has also given people a feeling of security and control over their finances.

Also, besides what the government is doing, digital banking is helping rural entrepreneurs and small businesses, too. With a real bank account and a record of digital transactions, people can now create a financial history, which helps them get loans. Having access to formal credit is really important for them to grow their businesses or invest in new ideas. A new trend is emerging with small business owners in rural India who are moving away from local moneylenders and are now able to access fair and affordable loans from banks. This marks a significant advancement in creating a more robust and inclusive rural economy.

The Path Forward

The transition from traditional banking to online banking in rural India is still underway. Initiatives like UPI and AePS have shown how technology can enhance financial inclusion, but there’s still much more to accomplish. Fintech companies are crucial in providing new, user-friendly apps and services that meet the needs of those in rural areas.

It’s not just about moving from cash to digital payments. It’s about building a system that enables every Indian, regardless of where they live, to manage their finances, save for the future, and support themselves, which in turn helps the economy of India. The transition to digital banking is linking urban and rural India, creating a future where financial services are available to everyone, not just a select few.

In an effort to democratise financial services nationwide, WeCredit, an Udaipur-based firm, has joined the ONDC (Open Network for Digital Commerce) Network, which is supported by the Indian government, as a Buyer App.

According to the press note, the strategic integration will make it possible for users—both people and businesses—to easily access lending and borrowing services through the ONDC Network, offering a simplified experience for anyone looking for financial solutions.

According to WeCredit co-founder Mukul Devpura, the company is excited to be a part of the ONDC Network and sees this as a major chance for investment and expansion within its broader business plan.

Making an Effort to Streamline the Loan Application Procedure

The landscape of digital banking has undergone a dramatic change with WeCredit’s admission into the ONDC Network. The firm will concentrate on improving financial accessibility and streamlining the loan application procedure, enabling consumers to more effectively reach their financial objectives.

The advancement supports ONDC’s overarching goal of promoting a more transparent and inclusive digital economy. Firm is delighted to be a part of a movement that seeks to make e-commerce more equitable and accessible for all people and businesses, regardless of their size or location, as India prepares for a digital revolution. According to Devpura, ONDC is about more than just expanding businesses; it’s also about helping to transform Indian trade by encouraging cooperation, diversity, and creativity.

Plans to Increase the Range of Products Offered

WeCredit will first concentrate on credit products as part of its staged strategy, with plans to soon broaden its offerings to include investment options, insurance, and a few retail categories.

WeCredit will function as a Technology Service Provider (TSP) on the ONDC Network in addition to being a Buyer App. Because of this function, WeCredit may assist companies that want to access the network without having to invest in a large internal IT infrastructure.

“ONDC is dedicated to furthering its goals of democratising digital commerce and promoting financial inclusion,” said T Koshy, MD and CEO of ONDC. Both small and large enterprises will be better able to negotiate the digital financial landscape thanks to WeCredit’s capabilities, which will create new avenues for growth and businesses.

What WeCredit Does?

WeCredit is a website that offers loans to both people and companies. It gives consumers a platform that enables them to apply for credit cards and loans instantly, with little paperwork and at affordable interest rates. In order to satisfy their credit needs, they concentrate on putting prospective borrowers in touch with various banks and regulated organisations. Over $2.86 billion has been raised by WeCredit and its rivals in 102 investment rounds with 375 investors, according to Tracxn. The competition set consists of three public companies, two acquired companies, and one private unicorn.

Setting up a business account for your small business is crucial if you’re looking to do anything related to banking. You may also need to apply for an EIN, which will make managing your taxes easier in later years. There are tons of perks when it comes to having this type of bank account.

But the perks are only attached to the right decision taken while going through the selection of the bank account. Let’s have a detailed understanding of the whole procedure starting with the perks attached to the small business account.

Each type of bank account has its own personal merits and demerits. Even small business bank accounts have their own perks over any other type of bank account. Let’s take a look at the advantages of having a small business bank account.

Bank Account is the Base of Business

The bank account will be where you deposit money from clients and make deposits from sales. The bank account is also where you receive payments for services or products sold through your business.

You can use this money to pay employees, rent office space, buy equipment and supplies, advertise your business, and more. All these dependencies on the bank account make it the foundation of the business. Hence, it is not wrong to assume that a bank account plays an essential role in forming the foundation of the business.

Maximizes Tax-Deductible Business Expenses

The bank will allow you to set up an account specifically for business expenses, which can be used to deduct any business-related expenses from your annual taxes. This means you won’t be taxed on any business income earned by using this account as a personal source of funds.

It Will Be Easier to Track Your Business Expenses

It will be easier to track your business expenses. You’ll be able to see which bills are paid by the business and which ones are paid by yourself. It will also make it easier to know how much money is available in the bank account at any given time, which can help determine whether you need money from home or if there is extra money sitting around waiting to be spent on something else.

Access to Capital and Credit

A capital and credit line is imperative for a small business. A good way to access capital is through a business loan, which can be obtained from a local bank or credit union.

Alternatively, one can also apply for a small business loan from a commercial lender. Commercial loans are usually more expensive than personal loans, but they come with more flexibility in repayment and interest rates.

8 Basic Things to Remember While Setting up the Small Business Bank Account

Though it may look exciting, setting up a small business bank account can be tricky. It’s more than just choosing a good financial institution and choosing the right type of account for your needs – there are pitfalls to be aware of. To avoid mistakes, we’ve compiled a list of things you should know when setting up your first small business bank account.

1. Consider the Type of Business You Operate

Knowing what type of business you will be running is important before setting up your business bank account. If you plan on running a very small business with just one employee or a small business with a few employees, it may not make sense to open an account with a big bank with multiple branches throughout your city.

Instead, consider opening an account with a local bank that caters to small businesses. This will ensure you get the best service and rates for your needs.

If you operate multiple locations or have employees working remotely, it makes sense to open an account at a large bank that provides services nationwide. You can still use these larger banks for managing your finances, but it’s also good practice to set up accounts at smaller local banks as well (especially if you do business online).

2. Check for the Bank Locations and Branches

Ensure your bank has multiple locations, including at least one branch near your business. If you’re doing a lot of business with other banks, it’s a good idea to make sure that you’ve got their contact information on file at your new bank as well. You never know when something might come up, and it would be nice to have a backup plan in place just in case.

3. Estimate the Frequency of the Bank Use

If you are only making monthly deposits, then opening an account with a local institution may be sufficient. However, if your business has more frequent transactions (i.e., weekly or daily), then you should consider a high-yield checking account instead of the previous one.

4. Outline The Payroll System

When managing a small business, you need to be aware of payroll and other financial matters. Payroll is one of the most costly elements of running a business. It can include taxes and benefits such as health insurance, 401(k) plans, vacation time, etc. You’ll want to ensure your business can pay its employees in full every month.

5. Get a List of Loan/ Credit Offered by the Bank as a Service

While banks tend to offer small business loans in one form or another, a handful of options are tailored specifically for small businesses. These include merchant cash advances (which allow you to take money from your account when needed), overdraft protection, and payroll advances.

6. Select a Bank With a Good Reputation

Researching banks can help you find out if they have been operating successfully in their chosen field for many years or not and if they have had any complaints filed against them by customers or clients over late payments or other issues such as fraudulence or corruption.

7. Enable Digital Banking

If you want to access your bank account via mobile phone or tablet, some banks offer apps that allow you to do so with a few clicks.

Digital banking has become standard for most financial institutions these days. This means that if there’s an issue with one account or another (which can happen), you’ll be able to access all of your accounts from any device — computer, tablet, or phone — without having to physically go into a branch or call customer service staff on the phone.

8. Look for Any Associated Fees

The following are some of the most common fees.

Deposit Fee: A fee a financial institution charges to make a deposit. A small business bank account may charge a low flat rate or tiered fee structure based on the size of the deposit you make.

Service Fee: The amount you pay to use an account, such as ATM withdrawals or checks to cash. It’s often included in your monthly statement and not explicitly listed. Ensure you understand how much you’ll be paying for each service before signing up for an account.

Terms and Conditions: Any additional information about your account that isn’t included in the monthly statement, such as additional fees or restrictions. Make sure to review these carefully before signing up for an account.

The complete process for setting up a small bank business account is a simple process given if all the steps are completed successfully and without any mistake.

Choosing a Bank

There are many banks to choose from, but you need to ensure that the one you choose is right for your small business. It’s important to look at their services and fees before choosing.

You can find this information on their website or contact them directly. You’ll need to look out for the interest rates and fees they charge, as well as whether they offer any special programs for small businesses.

If you’re starting a new business and aren’t sure where to start looking, it may be helpful to call around and see what other businesses are using as their banking service provider. This will give you a better idea of which banks offer the most competitive rates and services for small businesses.

Choosing an Account

You’ll need to choose a bank that offers the lowest interest rates to get the best rate. The most common way to do this is by using a credit card with a rewards program. To get the best rate, however, you will also need to use a bank offering low fees and minimum balances.

You can check banks’ websites or call their customer service lines to find out if they have any programs like these. You may need to make an appointment with someone in the customer service department to do this.

Setting up Your Account

Once you’ve selected a bank and have chosen an account, there are still a few steps to complete. To open an account, you’ll need to provide:

Proof of Identity: You’ll need two forms of proof of identity — one that shows your name and address, such as a passport or driver’s license. The other form must show your signature and photo, such as a birth certificate or passport.

Complete Formalities: The business will be required to furnish the mandatory details that might be related to the business to complete the account-setting process.

Get Your Welcome Kit: Once the formalities are done, you will receive a welcome kit that will include everything you need to start with banking transactions.

Leading private banks in India by their assets in Trillion Indian Rupees

The primary benefit of having a small business bank account is preventing your finances from getting mixed up with business finances. This will help you keep track of everything that’s going on with your business, but more importantly, it will help you avoid paying income taxes on money that doesn’t need to be taxed.

Avoiding extra income taxes not only helps you save money but also helps the government collect less money. The more organized your records are, the easier it will be to manage your business and personal finances later.

FAQs

What 4 documents do you need to open a business bank account?

4 documents required to open a business bank account are an employer identification number, business formation document, business license, and government-issued identification.

Do I need a separate bank account to start a business?

Yes, having a separate bank account for a business is considered a good practice to follow for organized business management.

Can I use my saving account as a business account?

Yes, saving accounts can be used as business accounts.

What are the disadvantages of a business bank account?

Business bank accounts are linked to multiple fees as compared to personal accounts. They are also provided with the minimum personal gains such as fewer insurance schemes and policies when compared with the ones available with the personal or saving account.

Company Profile is an initiative by StartupTalky to publish verified information on different startups and organizations. The content in this post has been approved by BANKIT.

BANKIT operates on a B2B2C business model to provide banking and financial solutions under one roof. The startup was officially founded in 2010, took seven years to research the market, and launched its first service in 2017. Founded by Amit Nigam and Satyajeet Limaye, BANKIT is all set to become India’s most trusted payment solutions company and create a ‘Millionaire Agents Network’.

BANKIT focuses to give banking and monetary administrations to underserved individuals who face difficulties in financial offices and are not educated enough. The company’s 50,000+ agents are spread across PAN India across level 2, level 3, and level 4 urban areas and towns to help and furnish clients with banking and monetary offices.

Walkthrough the exciting journey of BANKIT in this article, with highlights on BANKIT’s business model, how it started, its future plans and more.

Being a fintech company, BANKIT operates on a B2B2C business model to provide banking and financial solutions under one roof. It partnered with 15,000 neighbourhood retail stores in tier 2 and tier 3 areas of India, which can offer assisted digital financial services like Domestic Money Transfer, Cash out through APES/ micro ATM, also it has its own Prepaid card apart from additional services in Recharges, Utility Bill payments, loan, Insurance, Travel Booking, etc.

The company has over 80,000 outlets in 29 states that target to strengthen its presence in tier 2 and tier 3 areas with financial services. Recently, the company launched prepaid card solutions for corporates. Also, the vision of the company is to make a “Millionaire Agents Network” (MAN). It wants to maximize the number of agents who are able to make Rs. 10 lakhs as revenue in a year by delivering various BANKIT services.

BANKIT – Industry Details

According to Mr. Amit Nigam, the fintech industry is at the evolving stage to become three times more valuable in the coming 3-5 years. Gladly the government is helping companies to modify their services that add extra creation and strengthen the business. The Indian fintech market is expected to reach a valuation of $150-160 billion by 2025.

BANKIT – Startup Story

The journey of BANKIT started with Amit Nigam, who was also one of the founding members of Spice Money. During that journey, he understood the gap in banking requirements in backward areas. Hence, the idea of BANKIT arrived, where he targeted to enable the unbanked and underserved portions of the country by protected, secure, and advantageous banking, finance, and payment arrangements. BANKIT provides the fastest and easiest money transfer to around 400 banks, based on IMPS technology. It provides safe and instant domestic money remittances. The company was founded in 2010, took seven years to analyse the market, identify gaps, and determine the need for banking services in different states, and launched its first service in 2017.

The founders of BANKIT got in touch with a lot of family members and friends to discuss the idea; many of them gave positive feedback and were impressed by the larger mission that it was to serve. A few of them connected and joined hands, and support was extended in terms of manpower to create an incredible team.

BANKIT is the brainchild of Amit Nigam, a fintech leader with extensive experience of more than 22 years who has worked at the top of management in telecom, FMCG, and fintech companies like Airtel and Aditya Birla Group. Amit serves as the Executive Director and COO at BANKIT. He was also one of the founders of Spice Money. He is an experienced leader with skills in leading direct reports as well as cross-functional teams, justifying new product development investments, determining and documenting new product requirements, developing sales forecasts and product pricing, and launching new products into the marketplace. He also supervises the key management of large-scale projects for the company.

Whereas, Mr. Satyajeet Limaye, Chief Strategy Officer, works alongside Amit Nigam to lead equity deals on both the buy and sell sides, incubating, challenging strategy, and restructuring revenue streams through strategy and financial analytics.

BANKIT – Name and Logo

BANKIT Logo

The team at BANKIT wanted to connect and be relatable to the masses and wanted the name to be relatable with its mission of providing banking and financial services to the last mile.

BANKIT – Product and USP

BANKIT offers financial services to clients through its retail channels, outlets, and banking specialists. Monetary Services are effectively accessible at neighborhood shops. Individuals can visit the closest specialists for administrations with no reports. BANKIT is a stage that has various Banking, Financial, and Payment administrations under one roof and it continues to add more to it as indicated by the client’s needs.

BANKIT focuses on providing banking and financial services to underserved individuals who face difficulties in financial offices and are undereducated. The company’s 50,000+ agents are spread across PAN India across level 2, level 3, and level 4 urban areas/towns to help and furnish clients with banking and monetary offices. It offers B2B2C administrations that address dual-purpose occupations for specialists who offer various types of assistance to buyers and help clients with our quick, simple Banking, Financial, and Payment administrations that require no documentation.

The USP of BANKIT is its web-based interface and versatile application, which is easy to use and user-friendly for the end customers. Its portal and app are much more secure, authentic, and easy to use, if a customer is registered (prior done any exchange with BANKIT) his cash can be sent with 2-3 ticks just right away. The startup continues to update its app and portal according to the client’s needs. BANKIT has added numerous new administrations and guarantees free miniature advances for its agents, which was of great importance and ended up being helpful for the representatives just as much as for the clients. BANKIT is a solitary stage for various administrations accessible 24×7.

BANKIT – Business Model and Revenue Model

Being a fintech organization, BANKIT works on a business-to-business-to-client plan of action to bring banking and monetary arrangements under one roof. It offers financial services like Domestic Money Transfer, and cashouts through APES/miniature ATMs, and has its own prepaid card separate from extra administrations like recharges, utility bill instalments, insurance, travel booking, and so on. Its cutting-edge arrangements are intended to make monetary exchanges consistent, simple, and fast to engage the Agents.

The company offers types of assistance to the purchasers through its agent organization, and for help like DMT, it charges customers @1% on the settlement business according to RBI rules. Different models like money withdrawals through AePS/mATM, Mobile/DTH/Fastag, recharges, bill payments, protection, CMS, and so on are either through banks or aggregators. BANKIT gets a commission from them, which it gives to the retail channel.

As BANKIT’s target group is mainly from rural and semi-urban areas, the team approached retailers through direct marketing via sales personnel. The response received from the same proved to be successful and many retailers joined hands with BANKIT.

The COVID-19 pandemic and induced lockdown forced a lot of migrant workers from urban areas to internally migrate back to their hometowns. BANKIT utilised this opportunity to help these people get opportunities locally and thus get more people on board for its larger mission.

BANKIT – Growth and Revenue

Noida-headquartered start-upBANKIT has a presence in 29 states with more than 70,000 correspondents and 50,000 agents. Its significant business comes from Andhra Pradesh, Orissa, Telangana, Bihar, Maharashtra, Uttar Pradesh, Delhi, West Bengal, Tamil Nadu, Gujarat, Rajasthan, etc. The fintech stalwart’s estimated annual revenue is currently $15.1 million per year.

The team has experienced a huge number of difficulties all throughout their excursion, but the one prominent one that can be highlighted is its colossal business work during the Coronavirus lockdown.

At the point when the Coronavirus began influencing the Indian business market, the test was to re-plan the business and showcase systems totally at an ideal opportunity to settle and develop the business. The team was happy that BANKIT was not simply made due in the hardest season of the World yet, in addition, made the greatest business in lockdown as the interest of banking and monetary administrations gathered by buyers and BANKIT was prepared to give something very similar in those difficult occasions.

Since BANKIT began its first activity, it has seen that organizations have been confronting a few challenges during this pandemic opportunity to support on the lookout however for them, their huge line of administrations assisted BANKIT to cope in this difficult time and spotlight move on sought after administrations like Cash-out help has turned out a distinct advantage for its business. The company has enlisted the greatest income development and exchanges in the midst of the lockdown and has seen an upward pattern for a few of its contributions.

BANKIT – Competitors

Some of the prominent competitors of BANKIT are PayNearby, Fino PaymentS Bank and Spice Money.

BANKIT – Future Plans

The organization has kept an objective to add 1 lakh+ such outlets in the metropolitan and rustic piece of the country in this monetary year under its channel extension plan. Additionally, the organization is intending to dispatch another line of items and administrations in the coming months.

BANKIT wants to be the pioneer in the formation of a new India where everyone has access to banking facilities and doesn’t have to struggle for basic banking and financial needs. With the vision to become India’s largest and most trusted payment solutions company, the team is working to open more than 10,000 digital and brand BANKIT stores across the country. The startup aims to translate the vision of the government of digitizing rural India and making new entrepreneurs.

FAQs

What is BANKIT?

BANKIT offers financial services to clients through its retail channels, outlets, and banking specialists. It partnered with 15,000 neighborhood retail stores in tier 2 and tier 3 areas of India, which can offer assisted digital financial services like Domestic Money Transfer, Cash out through APES/ micro ATM, also it has its own Prepaid card apart from additional services in Recharges, Utility Bill payments, loan, Insurance, Travel Booking, etc.

Who are the founders of BANKIT?

BANKIT is the brainchild ofAmit Nigam. Mr. Satyajeet Limaye, Chief Strategy Officer, works alongside Amit Nigam.

What is the USP of BANKIT?

The USP of BANKIT is its web-based interface and versatile applicationwhich is easy to use and user-friendly for the end customers. Its portal and app are much more secure, authentic, and easy to use, if a customer is registered (prior done any exchange with BANKIT) his cash can be sent with 2-3 ticks just right away.

How much is BANKIT’s revenue?

BANKIT’s estimated annual revenue is currently $15.1 million per year.

How BANKIT works?

BANKIT offers financial services to clients through its retail channels, outlets, and banking specialists. Monetary Services are effectively accessible at neighborhood shops. Individuals can visit the closest specialists for administrations with no reports. BANKIT is a stage that has various Banking, Financial, and Payment administrations under one rooftop.

Is BANKIT safe?

BANKIT provides the fastest and easiest money transfer to around 400 banks, based on IMPS technology. It provides safe and instant domestic money remittance. Its portal and app are much more secure, authentic, and easy to use.

Who are the competitors of BANKIT?

Some of the competitors of BANKIT are PayNearby, Fino Payment banks & Spice Money.