India’s long history of promising and successful eCommerce startups also includes some well-known crashes too. ShopClues, an online shopping marketplace venture is a great example here as it rose to great heights before facing a hard fall. The startup tasted success so well that it even acquired the status of India’s fourth unicorn in 2016. But it couldn’t maintain its status for long as a series of events contributed to its downfall. This article will go through the reasons behind ShopClues’s failure.

The advent and wide use of the internet have ensured at least one element – the ability to create branching platforms. In this manner, most aspects of the pre-internet era have transformed to become more accessible and attainable. One such facet is the marketplace.

The traditional physical marketplace has been replaced almost completely by an online space for selling and buying. Contrary to the belief almost 30 years ago, eCommerce spaces are here to stay and thrive at it. There are various reasons why the eCommerce marketplace is booming throughout the world. These include:

It covers almost all borders and distances to bring products to a marketing platform.

It ensures more widespread access to products that were previously closed off to people because of geographical distances, low awareness, lack of access, etc.

It promotes and employs a greater amount of employees than any traditional selling platform.

These are some of the many reasons why eCommerce conglomerates like Amazon, eBay, Joi, Nykaa, etc., have created a successful space for eCommerce to flourish in most parts of the world.

In recent years, the Indian market has opened up multiple avenues to small businesses looking to transform into sustainable eCommerce businesses. The country also promotes established online commercial platforms. Therefore, eCommerce platforms like Amazon India, Snapdeal, Flipkart, Nykaa, Myntra, and more, have gone on to see great success in the Indian subcontinent.

However, these successes are balanced by major businesses that have failed to sustain themselves and secure a long-term future. One such company is ShopClues. Its rise and crash have been among well-noted cases in the eCommerce world.

ShopClues is an online marketplace, similar to Snapdeal and Amazon India. The eCommerce platform was founded 11 years ago in July 2011 by Sanjay Sethi, Sandeep Aggarwal, and Radhika Aggarwal. Owned by Clues Network Pvt. Ltd., the headquarters are situated in Gurugram, Haryana, India. The brand served the interests of the Indian consumerist client as an online shopping space.

The brand operates under the banner of ‘Made in India.’ At a time when Indians were beginning to look for ways to reduce dependency on China for goods and materials, platforms like ShopClues came to the forefront. People saw these online establishments as the perfect solution to a more patriotic and unified image of India. ShopClues certainly profited off of this value, offering goods made in India as well as foreign products at considerable discounts. Moreover, instead of focusing on large urban metro cities, the brand concentrated on selling basic and practical products related to cleaning, kitchen, apparel, electronics, and other items to Tier II and Tier III cities. Within two years of its existence, ShopClues boasted one million active users.

As a result, the brand saw major investors like Tiger Global, Helion Ventures, and Nexus Venture Partners invested in ShopClues. According to Forbes India, the brand possessed a value of $1.1 billion in 2016 and therefore, acquired the status of a unicorn startup in India.

With such success, where did the brand go wrong? How did ShopClues lose such a massive chunk of its revenue in later years? Let us go on to find out the answers.

The success of an eCommerce venture goes beyond selling its products. From rival companies to internal affairs, a lot more goes behind the brand’s capability of running operations smoothly. Sustaining a project as well as ensuring a stream of profits at the end of every fiscal year is not as easy as it sounds. ShopClues also faced many hurdles that led to its downfall. Below, we are going to take a look at some of the most prominent issues ShopClues had to deal with and ended up failing disastrously:

Aggressive Rival Tactics

When ShopClues came about and gained traction in the Indian consumerist sector, eCommerce businesses were a thing of rarity. Its founders took advantage of this in 2011 and began to market its products accordingly. However, by 2014, Amazon and Walmart-owned Flipkart began to focus their attention on establishing online shopping platforms in India.

Whereas Flipkart was seen as only an online bookstore and Amazon as a western organization. Both began to aggressively market themselves to remove rivals. This affected the growth and consolidation of ShopClues, which became the small fish surrounded by sharks. New rivals with better and more refined marketing skills overpowered any model ShopClues could produce. This was one of the reasons behind the failure of ShopClues.

False Branding

The company also suffered losses in terms of its offerings. In 2011, the vision was to bring urban goods to sub-urban and rural spaces that lacked the opportunity to access the same. However, complaints from consumers began to stream in that the products were fake. The Luxottica Group, the owner of Ray-Ban, alleged that ShopClues had been selling Ray-Ban products under fake labellings. The accusation prompted the Delhi High Court to pull up the Indian brand for selling the products despite previous warnings. This adversely affected the image of ShopClues among the public.

Poor Quality Products

Alongside fake products, reports also came in that the brand was dealing people with poor-quality products. Despite the low costs and exciting offers, the products were not up to par. Many users complained of scams and dupes perpetrated by the company. People did not receive their goods or refunds on time. The customer support option was unavailable to most pleas for help. This created bad blood among users towards the brand and affected ShopClue’s image.

Internal Scandals

Multiple scandals rocked the company over and over. The founder and CEO of ShopClues, Sandeep Agarwal, was charged with insider trading allegations in 2013. Consequently, Aggarwal was arrested in the United States where he accepted a plea bargain on the accusations and pleaded guilty. He resigned from the post of CEO of ShopClues the same year.

2017 saw a stormy year for the brand internally. Sandeep Aggarwal blamed Radhika (his estranged wife) for forcing him out of the company. Subsequently, the couple split up and continued to spar publicly over voting privileges and charges of fraud. Aggarwal then made a humiliating Facebook post regarding his wife and also filed a case of criminal defamation against Sethi and Radhika. He accused them of downplaying his contribution as the creator and founder of ShopClues. All such scandals among the founders created a false image of the platform in the public eyes.

ShopClues – Negative Reviews and Scandals

Migration of Consumers

With a clear lack of invigorating and innovative business foundations and adaptability, ShopClues was slated for failure when the big names came into the fight. Platforms like Amazon and Flipkart started gaining popularity and trust among the consumers and ShopClues did not have an adequate plan to retain its consumer base, leading to a collective exit of many consumers towards other platforms.

Extreme Cost-Cutting Measures

Due to continued failures, ShopClues decided to undergo extreme measures to save costs. Hundreds of employees were regularly laid off every year after 2016. In fact, more than 200 employees were laid off in 2017 itself. ShopClues’ expenses decreased by a whopping 60% between 2018 to 2020. The financial year of 2018 saw Rs. 363.4 crores in expenses which went down to Rs. 278 crores in 2019. 2020 saw a further dramatic decrease of Rs. 148.6 crores.

ShopClues shortened its budget for ads and promotions down to 80% in 2018. It further slashed costs to 60% in 2019. The shipment cost dropped completely down to 100%. There were no reports of transport or charges for hiring in the fiscal year of 2020, so it is assumed that these costs were also slashed.

Conclusion

ShopClues had all the makings of being a successful eCommerce platform with viability. However, various factors like competition, a lack of business initiatives, and unclear modules of operation left the company in the dust. Its internal affairs and state of handling procedure also had a hand in ShopClues becoming a redundant business that was once a shining avenue.

FAQs

Is ShopClues an Indian company?

Yes, ShopClues is an Indian company founded by Sandeep Aggarwal, Radhika Aggarwal, and Sanjay Sethi in the year 2011. The company has its headquarters in Gurugram, Haryana, India.

Who acquired ShopClues?

ShopClues was acquired by Singapore-based Qoo10 in a stock deal in the year 2019 for a valuation between 70 to 100 million USD.

Is ShopClues a failure?

ShopClues had many reasons that led the startup towards its failure. These include false branding, rival tactics, internal scandals, and the lack of trust among the customers.

Is ShopClues unicorn?

ShopClues acquired unicorn status in the year 2016 with a valuation of around $1.1 billion, making it the fourth unicorn startup in India. However, the company could not hold this valuation for long and ultimately got sold to Qoo10 at a valuation between $70-$100 million.

McDonald’s Corporation is an American fast-food organization established in 1940 as a café by Richard and Maurice McDonald, in San Bernardino, California, United States. They rechristened their business as a burger stand and later transformed the organization into an establishment; the Golden Arches logo being presented in 1953 at an area in Phoenix, Arizona.

Ray Kroc, a businessperson, joined the organization as an established operator in 1955 and continued to buy the chain from the McDonald’s siblings. McDonald’s had its base camp in Oak Brook, Illinois, and moved its worldwide base camp to Chicago in mid-2018.

McDonald’s is worth $185+ bn today. It is the world’s biggest eatery network by revenue. It was last registered to be serving 69+ million customers each day in more than 120 countries across over 39,000 outlets.

Although McDonald’s is best known for its burgers, cheeseburgers, and french fries, its menu also includes chicken items, breakfast things, sodas, milkshakes, wraps, and sweets. In light of changing buyer tastes and a negative backfire on account of the wretchedness of its food, the organization has added mixed greens, fish, smoothies, and natural products to its offerings.

McDonald’s Corporation’s income originates from leases and charges paid by the franchisees. According to two reports distributed in 2018, McDonald’s is the world’s second-biggest private manager with 1.7 million representatives (behind Walmart with 2.3 million workers).

Here’s bringing you the McDonald’s company profile that will present to you McDonald’s company overview, when was McDonald’s founded, McDonald’s growth over the years, about McDonald’s, McDonald’s owner name, founder of McDonald’s corporation, McDonald’s history and background, McDonald’s case study marketing, and more.

McDonald’s – Company Highlights

Company Name

McDonald’s

Headquarters

Chicago, Illinois , U.S.

Founded

1940

Founders

Richard and Maurice McDonald’s and then by Ray Kroc

Richard and Maurice McDonald in 1940, opened the primary McDonald’s at 1398 North E Street at West fourteenth Street in San Bernardino, California; however, it was not the McDonald’s you know today. Ray Kroc made changes to the siblings’ business and modernized it.

MacDonald’s Founders – Richard McDonald, Maurice McDonald and Ray Kroc (From Left to Right)

The siblings presented the “Speedee Service System” in 1948 by extending the standards of cutting-edge drive-thru eatery that their antecedent White Castle had tried over two decades earlier. McDonald’s emerged with a delivery model where it made its food on a supply belt and delivered it within 2 minutes.

It looked like a fantastic and impossible eatery that had:

• Only burgers, fries, and shakes on the menu • No plates or waiters to serve the customers

However, when Ray Kroc came, he was astonished by the never-ending waiting lines that were there waiting for their orders from McDonald’s.

Kroc was then 50 already and was selling milkshake mixers door to door. Ray Kroc had earlier tried his hand in many things but never had attained success in his whole life. He already worked as a musical director, pianist, and had also worked as a real estate guy, in the paper cup industry, and as a seller of kitchen appliances, but he couldn’t hold on to one thing among them all. Thus, Kroc was a person who lived from paycheck to paycheck.

Kroc came to McDonald’s to deliver an absurd order of 8 milkshake mixers for just one area. He wondered “why would someone want to make 40 milkshakes at a time?” This is why he drove to California, at McDonald’s to see the place himself.

Seeing the huge demand for McDonald’s burgers, fries, and shakes, Kroc sensed a huge opportunity. He soon pushed the founders of the store to embrace a franchise model. The McDonald’s brothers who owned the business, were living a comfortable life then, getting rich by the day, and buying Cadillacs as they filled their pockets. They didn’t have vision nor they were eager to expand. However, Ray convinced them and rushed to work, as soon as he did that.

He assumed the role by taking 2 major steps back to back:

Mortgaging his house when he was already 52

Opening 18 new outlets in the very first year

This has helped the company scale big time, and McDonald’s now boasts of:

Serving 2.3+ billion burgers a year

Serving 39,000+ restaurants across more than 120 countries

Being the 4th largest employer in the world

Being the largest toy distributor in the world

Though it was Ray’s idea and the expansion was promising, the McDonald’s brothers made an unfair deal with him. Kroc was allowed only 2% of the profits. McDonald’s being to scale aggressively but the founders of McDonald’s wasn’t really happy with Ray and his scaling. This is why Ray borrowed and bought them out for $2.7 mn, thereby becoming the 100% owner of McDonald’s.

The organization attributes its success to Ray Kroc. Kroc later bought the McDonald siblings’ value in the organization and was responsible for McDonald’s overall reach. He was seen as a forceful colleague, driving the McDonald siblings out of the business. Kroc and the McDonald’s siblings battled for control of the business, as recorded in Kroc’s life account.

Ray Kroc

The San Bernardino eatery was torn down (1971, as indicated by Juan Pollo) and the site was offered to the Juan Pollo chain in 1976. This zone currently fills in as central command for the Juan Pollo chain, and a McDonald’s and Route 66 museum.

With the development of McDonald’s into numerous universal markets, the organization has turned into an image of globalization and the American lifestyle. Its unmistakable quality has additionally made it a regular point of open discussions about heftiness, corporate morals, and shopper obligation.

McDonald’s – Mascot/Logo

The first mascot of McDonald’s was a cooking cap over a burger who was alluded to as “Speedee”. In 1962, the Golden Arches supplanted Speedee as the all-inclusive mascot. The image of jokester Ronald McDonald was presented in 1965. Ronald McDonald showed up to promote amongst children.

First mascot of McDonald’s

On May 4, 1961, McDonald’s initially petitioned for a U.S. trademark on the name “McDonald’s” with the portrayal “Drive-In Restaurant Services”. By September 13, McDonald’s, under the direction of Ray Kroc, petitioned for a trademark on another logo—a covering, twofold curved “M” image.

McDonald’s Logo

Before the twofold curves, McDonald’s used a solitary curve for the design of its structures. Even though the “Brilliant Arches” logo showed up in different structures, the present form was not utilized until November 18, 1968, when the organization was given a U.S. trademark.

McDonald’s – Business Model And Market Strategy

The business and revenue model of McDonald’s includes almost 37000 outlets which spread to more than 120 nations. Today, McDonald’s is the biggest eatery network on the planet in terms of income.

Initially launched as a Drive-In Hamburger Bar, the idea was advanced in 1940 by The McDonald Brothers, Richard James (Dick), and Maurice James (Mac) McDonald. It was after the presentation of the Speedee Service System with shakes, fries, and burgers costing as low as 15 pennies that the McDonald Brothers started the establishment of McDonald’s Hamburgers.

First McDonald’s

In 1954, Ray Kroc turned into the establishment operator of the McDonald Brothers. The main McDonald’s eatery was opened by Kroc in 1955 in Des Plaines, Illinois, USA. It was in the year 1961 that the rights to the eating joint of the kin were obtained by McDonald’s for a powerful total of $2.7 million.

You may likewise be astonished to realize that when the first McDonald’s eatery opened, the extremely well-known McD french fries were eaten with no ketchup! The revenue model of McDonald’s, the world’s quickest developing food chain, is an interesting one.

McDonald’s – Target And Mission

McDonald’s endeavours hard to be its clients’ “most loved spot and approach to eating”. McDonald’s plan of action is fixated on the ground-breaking strategy “Plan To Win”, which is placed into requests around the world.

With the mission of “Quality, Service, Cleanliness, and Value”, McDonald’s has clung to each of these characteristics. Client experience is improved by the selection of five fundamentals: people, products, place, price, and promotion.

Additionally, McDonald’s plans to give high-review nourishment, at effectively reasonable costs to individuals over the globe. The deals at McDonald’s are furrowed through an efficient deals channel which guarantees remarkable consumer loyalty on all occasions.

Astounding Vision

When Ray Kroc opened the Original McDonald’s in Illinois, he had a dream of expanding the franchise across the globe with more than 1000 outlets in the States itself. Remaining consistent with its guarantee, McDonald’s widened its worldwide handle by opening joints outside the US as early as 1967.

The first international outlets were opened in Canada and Peurto Rico. By January 2018, McDonald’s was situated in 120 nations and had about 37200 cafés with 1.9 million workers. It was serving more than 69 million individuals every day. At one point in time, McDonald’s was opening a new outlet every 14.5 hours!

Significant Growth Strategy

McDonald’s has clutched a promising development technique to serve customers and spread its wings. The presentation of the “Speed Growth Plan” in March 2017 enhanced the development of the business.

McDonald’s development system depends on retaining, regaining, and converting. McDonald’s strives to hold on to its old clients, recapture the lost trust, and convert easygoing clients into ordinary ones.

What’s more, it has additionally embraced three quickening agents: digital, food delivery, and experience of things to control its monstrous development. It keeps on reshaping cooperation with clients and raising the level of consumer loyalty and experience through innovation and human endeavours.

Decent Variety

Monetarily, McDonald’s has affected the world more significant manner than some other organizations. McDonald’s adheres to the conviction “Decent variety is Inclusion” and doesn’t leave a solitary opportunity to make each person from every network feel regarded. Its suggestion of “Decent variety is Inclusion” has affirmed its situation at the top position.

The McDonald’s way of life revolves around the following: customer-obsessed, better together, and committed to lead. These coupled with its conviction has caused the fast-food chain to exceed expectations in the field of business enterprise and showcasing.

McDonaldization

McDonald’s can appropriately be named as one of the best organizations to be involved in the worldwide system. The worldwide broadening of the McDonald’s is regularly alluded to as “McDonaldization.” Its accomplishment in more than 120 nations can be credited to its hierarchical structure.

The hierarchical structure of McDonald’s mulls over expanding localization, and in this way, the entire plan of action of McDonald’s is normally redone thinking about the mass intrigue in different nations.

Fruitful Acquisitions

The McDonald’s Corporation Mergers and Acquisitions (M&A) have, since its inception, entertained itself with cautious acquisitions. Donato’s Pizza which is a Midwestern chain of 143 eateries was obtained by McDonald’s on 6 May 1999. Aside from securing Donato’s, it acquired the Boston Market on 18 May 2000. Boston Market is a drive-through eatery chain that essentially focuses on home-style sustenance.

Supporting Employees

McDonald’s doesn’t, in any capacity, hamper the development of its workers. It bolsters its representatives in every possible way and empowers them to set up business systems.

At McDonald’s, the work environment is brimming with positivity, connections are advanced, professional openings are supported, and business development is sustained.

Coaches, good examples, and backers are accessible at all times to direct the employees on successful initiatives, professional procedures, and prosperous business.

Engagement Of Community And Education

Aside from being one of the best good-quality fast food options, McDonald’s investigates every possibility to endeavour for the network it serves. It effectively takes part in network administration and continues to have a critical effect on assorted networks.

The Global Diversity, Inclusion, and Community Engagement Team alongside its key accomplices have fabricated cherished relations with different network-based associations. McDonald’s Hamburger University readies its workforce to maintain the multi-billion dollar business and worldwide initiative improvement programs.

McDonald’s – Growth

McDonald’s eateries are found in 120 nations and serve 69 million customers each day. McDonald’s operates 39,000 restaurants/cafés around the world, utilizing more than 210,000 individuals as part of the arrangement. They help operate 2,770 organization possessed areas and 35,085 diversified areas, which incorporates 21,685 areas diversified to regular franchisees, 7,225 areas authorized to formative licensees, and 6,175 areas authorized to remote affiliates.

Concentrating on its centre image, McDonald’s started stripping itself of different chains it had gained during the 1990s. The organization possessed a large stake in Chipotle Mexican Grill until October 2006 when McDonald’s was completely stripped from Chipotle through a stock exchange.

Until December 2003, it likewise claimed Donatos Pizza, and it claimed a little portion of Aroma Café from 1999 to 2001. On August 27, 2007, McDonald’s sold Boston Market to Sun Capital Partners.

Outstandingly, McDonald’s has expanded investor profits for 25 back-to-back years, making it one of the S&P 500 Dividend Aristocrats. The organization is positioned 131st on the Fortune 500 of the biggest United States companies by revenue.

In October 2012, its month-to-month deals fell without precedent for nine years. In 2014, its quarterly deals fell without precedent for a long time, when its deals last dropped for the whole of 1997.

In the United States, McDonald’s accounts for 70% of sales in drive-throughs. McDonald’s shut down 184 eateries in the United States in 2015, which was 59 more than what they wanted to open.

Mcdonald’s Drive-Thru

Starting in 2017, the income was roughly $22.82 billion. The brand estimation of McDonald’s is more than $88 billion; outperforming Starbucks with a brand estimation of $43 billion. The total compensation of the organization in 2017 was $5.2 billion; this worth saw an ascent of about 11% from the previous year.

McDonald’s is, without a doubt, the quickest developing drive-thru eatery chain on the planet. In 2018, McDonald’s developed as the most profitable inexpensive food chain with a brand worth nearing $126.04 billion. Also, the all-out resources of McDonald’s were almost $33.8 billion.

The world’s quickest developing cheap fast food chain partitions its market into four unique areas: U.S., International Lead Markets, High Growth Markets, and Foundational Markets and Corporate.

According to the report set forth by the organization in the year 2017, the market in the U.S. created the biggest measure of income at $8 billion. The International Leads Markets which includes Australia, Canada, France, Germany, and the U.K. created an income of $7.3 billion.

The High Growth Markets which incorporate China, Italy, Korea, Poland, Russia, Spain, Switzerland, the Netherlands, and comparative brought in about $5.5 billion in revenue.

The Foundational Markets and Corporate incorporate the rest of the business sectors. Furthermore, it additionally incorporates a wide range of corporate exercises. The income created by this section of the market represented roughly $1.9 billion.

In certain nations, “McDrive” areas close to roadways offer no counter administration or seating. interestingly, areas in high-thickness city neighbourhoods frequently preclude pass-through service. There are likewise a couple of areas, found for the most part in the downtown locale, that offer a “Walk-Thru” administration instead of a Drive-Thru.

McCafe

McCafé is a bistro-style backup to McDonald’s cafés and is an idea conceived by McDonald’s Australia (likewise known, and promoted, as “Macca’s” in Australia), beginning with Melbourne in 1993. As of 2016, most McDonald’s outlets in Australia have McCafés situated inside the current McDonald’s eatery.

McCafe

In Tasmania, there are McCafés in each eatery, with the rest of the states rapidly following suit. After moving up to the new McCafé look and feel, some Australian eateries have seen up to a 60% expansion in deals. There were more than 600 McCafés around the world some time back.

Create Your Taste

From 2015–2016, McDonald’s attempted another gourmet burger administration and eatery idea dependent on other gourmet cafés, for example, Shake Shack and Grill’d. It was taken off without precedent for Australia in early 2015 and extended to China, Hong Kong, Singapore, Saudi Arabia, and New Zealand with progressing preliminaries in the US showcase.

McDonald’s Create Your Taste

In committed “Make Your Taste” (CYT) booths, clients could pick all fixings including a kind of bun and meat alongside discretionary additional items. In late 2015, the Australian CYT administration presented CYT servings of mixed greens.

After an individual had requested, McDonald’s prompted that hold up times were between 10–15 minutes. At the point when the nourishment was prepared, the prepared group (‘has’) carried the sustenance to the client’s table.

Rather than McDonald’s typical cardboard and plastic bundling, CYT nourishment was exhibited on wooden sheets, fries in wire bushels, and servings of mixed greens in china bowls with metal cutlery. A more expensive rate connected. In November 2016, Create Your Taste was supplanted by a “Mark Crafted Recipes” program intended to be increasingly proficient and less expensive.

McDonald’s Happy Day

McHappy Day is a yearly occasion at McDonald’s during which a portion of the day’s deals goes to philanthropy. The collections on this day go to Ronald McDonald House Charities.

In 2007, it was celebrated in 17 nations: Argentina, Australia, Austria, Brazil, Canada, England, Finland, France, Guatemala, Hungary, Ireland, New Zealand, Norway, Sweden, Switzerland, the United States, and Uruguay. As indicated by the Australian McHappy Day site, McHappy Day brought $20.4 million up in 2009. The objective for 2010 was $20.8 million.

McDonald’s Monopoly Donation

In 1995, St. Jude Children’s Research Hospital got a mysterious letter stamped in Dallas, Texas, containing a $1 million winnings McDonald’s Monopoly game piece. McDonald’s authorities went to the medical clinic, joined by a delegate from the bookkeeping firm Arthur Andersen, inspected the card under a diamond setter’s eyepiece, took care of it with plastic gloves, and checked it as a winner.

McDonald’s Monopoly

Although game guidelines disallowed the exchange of prizes, McDonald’s deferred the standard and made the yearly $50,000 annuity instalments for the full 20-year time frame through 2014, even in the wake of discovering that the piece was sent by an individual associated with a theft plan meant to cheat McDonald’s.

McRefugee

McRefugees are destitute individuals in Hong Kong, Japan, and China who utilize McDonald’s 24-hour cafés as transitory lodging. One out of five of Hong Kong’s populace lives underneath the destitution line. The ascent of McRefugees was first archived by picture taker Suraj Katra in 2013.

McDonald’s For Refugees

McDonald’s – Future

The reported objective is to source all visitor bundling from inexhaustible, reused, or ensured sources, reuse visitor bundling in 100% of eateries, and overcome framework challenges by 2025.

McDonald’s turned into the principal eatery organization on the planet to set an endorsed Science-Based Target to lessen ozone-depleting substance emanations. It also joined the “We Are Still In Leader’s Circle”, driving activity to relieve environmental change.

McDonald’s USA completed five years as the sole worldwide café organization to serve MSC-ensured fish in each U.S. area. It united with Closed Loop Partners to build up a worldwide recyclable and additionally compostable cup arrangement through the NextGen Cup Challenge and Consortium. Official pioneers called for atmosphere activity and offered arrangements at the primary Global Climate Action Summit (GCAS).

McDonald’s co-facilitated the “Way to Greenbuild” occasion with Illinois Green Alliance at its new worldwide home office. The structure, a collaboration among Sterling Bay, McDonald’s, and Gensler Chicago, got USGBC LEED Platinum accreditation.

McDonald’s is establishing the tone for other inexpensive food organizations to pursue. Given the present want by numerous buyers to spend cash on organizations that are doing great on the planet, where McDonald’s leads, others will pursue.

McDonald’s was founded by Richard McDonald and Maurice McDonald on 15 April 1955 in California, United States.

Who is the CEO of Mcdonald’s?

Chris Kempczinski is the CEO of Mcdonald’s since Nov 2019.

Who is the owner of McDonald’s in India?

In India, McDonald’s is a joint-venture company managed by two Indians- Amit Jatia (M.D. Hardcastle Restaurants Private Ltd) and Vikram Bakshi ( Connaught Plaza Restaurants Private Ltd).

When was the fast-food chain McDonald’s founded?

Mcdonald’s was founded in 1940 in San Bernardino, California.

How much does a Mcdonald’s franchise owner make?

An average Mcdonald’s franchise generates $150,000 annually.

Marketing is the heart of a brand. If it doesn’t work properly, then the brand is as good as dead. Companies and brands often look for new ways to attract the attention of the people who can be their potential customers. Creative techniques of marketing are used to obtain the exact attention from the public. Whether, its about launching new product and services or opening a new branch of the brand or just general marketing, brands elevates new ways to market.

Now, in this digital world, where we live in, competition is higher than ever. So brands are being cautious and more creative to involve people and make their brand noticed. There are different types of marketing techniques that brands follow, especially while launching their new branch. It is naturally done to make people aware and attract them. In this article, we will talk about IKEA and how it creates a big buzz while launching its store in Bangalore, which is the biggest store in India. So, without any further ado, let’s get started.

IKEA is a multinational conglomerate that deals with home furnishing products. The headquarters of the company is situated in Delft, Netherlands. It was founded in the year 1943 by Ingvar Kamprad. The Swedish company is famous for designer home decor like kitchen appliances and other furniture that can be assembled on your own. IKEA is considered the world’s most famous and successful company. All the interior design items that IKEA sells are eco-friendly plus the prices of the products are low as well. As of now, IKEA has 467 stores in 63 countries and serves its people with its modernized and ready-to-assemble furniture.

How Does IKEA Promote Their Store Launch in Bangalore?

The Swedish furniture brand has India covered by having two physical stores in Mumbai and Hyderabad. IKEA opened their biggest store in India in Bangalore. The store is said to be covered in 500,000 sq. ft. and it is said that it will be attracting over 7 million visitors every year, with its low pricing and marketing strategy. Now, the brand has done many marketing schemes to make people aware of the launch of its store. IKEA took the help of drones and hosted a show in Karnataka to invite people to visit their newly formed store. The company used over 520 drones that light up the sky. Apart from that, in different landmarks of the city, the brand created a room set-up that consists of modern-looking home products to showcase it in front of the people of the city.

The Marketing Trend With Funny Banters

Now, we have seen brand engaging with each other in funny banters and using sarcastic comments to rile them up. Some of the brands actually did the same thing with IKEA, during the launch of their Bangalore store. They made funny remarks, challenge IKEA, and promote their own brands in a shady way. The trend was started and still is ongoing. The banter was started by Wakefit and many different brands jump into this trend.

Wakefit

Wakefit

Wakefit is a company that is famous for providing mattresses, pillows, mattress covers and bed frames. Apart from that, the company also deals with furniture products for home decor and appliances. It has released few sarcastic advertisements to taunt IKEA. In the marketing campaign, Wakefit in an open letter gives out a snarky welcome and said how tasty Dosas could be found in CTR and the weather is amazing. It also points out many of its supposed flaws like how IKEA is located on the outskirts of the city. Apart from that it also stated that the audience might face traffic issues as well. They challenge the Swedish company by mentioning that they should visit Wakefit if they Are looking for the best furniture. Not only that, but they have also used Swedish on the front page of the newspaper for their print ad to taunt IKEA. The company still hasn’t responded to this banter.

DrinkPrime

DrinkPrime

DrinkPrime, which is a water purification company that provides water Purifiers from Bangalore, also took part in this trend by posting a digital poster on LinkedIn and using the work ‘KEA’. In this post, they asked their audience if they have visited IKEA? After their visit, if they are tired? Did they have water after that? These questions were ended by ‘KEA’. Basically, in the post, they tried to promote their water purifier brand while using IKEA.

CoWrks

CoWrks

CoWrks is a company that provides co-working space design in offices and makes it feel like home. The company built spaces for all kinds of startups and businesses. The company welcomed IKEA in Bengaluru in their own style by posting a digital poster on LinkedIn that says “Collaborative Spaces + Brilliant Interiors = A Brilliant IKEA”

How Does the Trend Help IKEA?

Many brands got involved in this trend and tries to welcome IKEA in Bangalore, mainly they participated in this trend, to promote themselves. However, this trend helped IKEA make its presence known in front of people. As the brands took turns to welcome or snide remarks, many people got aware of the biggest IKEA store in the country and showed interest in checking it out. This way, the companies not only promote themselves but also promoted IKEA. One of IKEA’s loyal customers also gave a reply to Wakefit’s snide remark and called the brand ‘Fakefit’ and wrote an open letter just like the former.

Patanjali = Baba Ramdev + Ayurveda + Organic + Healthy + Desi + People’s Trust + Quality Product. The combination of all makes Patanjali a dynamic business model in a country like India. Speaking of this, the way Patanjali manifested itself in the Indian market reflects its brilliant marketing strategy and brand positioning. Though Patanjali has a wide range of products, it gets sold easily because of the brainchild behind this, i.e. Baba Ramdev, primarily known for his popularizing Yoga and Ayurveda in India.

Patanjali – Company Highlights

Company Name

Patanjali Ayurved

Headquarters

Haridwar, Uttarakhand, India

Founders

Baba Ramdev & Acharya Balkrishna

Sector

Consumer goods & Healthcare

Founded

2006

Parent Company

Patanjali Ayurved Limited

Website

patanjaliayurved.org

Patanjali Ayurved Limited was established in 2006 with the thought of rural and urban development. The company is not merely an organization but a thought of creating a healthy society through Yoga and Ayurveda.

Patanjali Ayurved, (commonly known as Patanjali), is an Indian fast-moving consumer goods (FMCG) company based in Haridwar, India. It was founded by Baba Ramdev and Acharya Balkrishna in 2006. Its registered office is located in Delhi, with manufacturing units and headquarters in the industrial area of Haridwar. The company manufactures cosmetics, ayurvedic medicine, and food products.

Patanjali fabricates mineral and natural items. It also has manufacturing units in Nepal under the trademark “Nepal Gramudhyog” and imports a greater part of herbs in India from the Himalayas of Nepal.

In 1995, Baba Ramdev was a little-known yoga teacher in Haridwar when his close associate, Acharya Balkrishna, and he set up Divya Pharmacy – under the aegis of Ramdev’s guru, Swami Shankar Dev’s, ashram – to make Ayurvedic and herbal medicines. The medicines proved so popular that Ramdev and Balkrishna sought to diversify. But that proved difficult since Divya Pharmacy was registered under a trust.

Meanwhile, Baba Ramdev started gaining popularity which helped him to receive funds from the likes of NRIs Sarwan and Sunita Poddar, as well as locals such as Govind Agarwal – which in turn helped to get bank loans. This led to the incorporation of Patanjali Ayurved as a private company in 2006, with the purpose to bring the Ayurved in the form of the various product range, particularly in healthcare, hair care, dental care, toiletries, food and more – at breathtaking speed.

The initial days were quite difficult for them. They hardly had money to pay for the registration of Divya Pharmacy. For the first three years, till 1998, they distributed the medicines free. From buying the raw materials to grinding and mixing, everything is done by themselves as they cannot employ staff because of the lack of money.

It is noteworthy for a brand to be not the same as its rivals, and Patanjali quickly developed its own identity. Patanjali’s mantra of low costs goods and ‘swadeshi’ are broadly viewed as the principal purposes for its prosperity.

How did Baba Ramdev do it? The man has astutely related Patanjali with Ayurveda, which pulled in a huge group of spectators. He has brought Ayurveda into the market by matching it with the need of the consumers, particularly, by developing a wide range of products, thus enhancing the brand recall value.

He has picked up the trust of clients not just by demonstrating the products to them but also by using them himself. However, all of the organization’s procedures to verify the quality and amount of the items are strictly followed.

Patanjali Ayurved bids broadly by anticipating a picture of regular and unadulterated items. Baba Ramdev, its image diplomat, is additionally an open figure and well-being advertiser whose mass intrigue has ascended in recent years.

Patanjali – Founders

Baba Ramdev | Founder | Patanjali

In 1995, Balkrishna and Baba Ramdev founded Divya Yoga Mandir Trust in Haridwar, and in 2006, they founded Patanjali Ayurved a fast-moving consumer goods (FMCG) company involved in the manufacturing and trading of FMCG, herbal, cosmetics and ayurvedic products.

Swami Ramdev (born Ram Kisan Yadav in 1965), also known as Baba Ramdev, is an Indian yoga teacher and businessman, primarily known for his popularising Yoga and Ayurveda in India.

While Ramdev does not hold a stake in Patanjali Ayurved, he is the face of the firm and endorses its products to his followers across his yoga camps and television programs. Balkrishna owns 94% of the company and serves as its managing director. He is a close aide of Baba Ramdev.

Archarya Balkrishna | Founder | Patanjali

Balkrishna claims 98.6% of Patanjali Ayurved, and as of March 2018, it has total assets of ₹43,932 crores ($6.1 billion). Acharya Balkrishna is India’s Third youngest Billionaire with US$2.3 billion wealth as per the Forbes list of India’s 100 Richest People (May 2021).

Patanjali – Name, Logo & Tagline

Patanjali Ayurved Logo

The word “Patanjali” is a compound name from”patta” (meaning falling, flying) and “añj” (honour, celebrate, beautiful) or “añjali” (reverence, joining palms of the hand). The meaning of Patanjali is ‘Famous Yoga Philosopher‘ or ‘The authorof Yoga sutras‘.

The tagline of Patanjali is “Prakriti ka Aashirwad” which signifies that it uses Ayurveda (something that is perceived as a healthcare approach) and organic and natural ingredients to create a wide range of products, thus beautifully depicting an illusion in the mind of the customer that the product they’re using is really a nature’s blessing.

Patanjali – Vision and Mission

VISION

Keeping Nationalism, Ayurved and yoga as their pillars, Patanjali is committed to creating a healthier society and country by bringing the blessings of nature into the lives of people in the form of Ayurveda, a healthcare approach that is religious and spiritual. Having said that, Patanjali is all set to create a history in the Indian FMCG sector.

MISSION

Ayurveda has its foundation laid in ancient times as a healthcare approach but people have been neglecting it. So, there when Patanjali came into the picture to make India an ideal place for the growth and development of Ayurveda and a prototype for the rest of the world by upbringing awareness among people.

Patanjali – How Did It Achieve Success?

How Patanjali Achieved Success

Patanjali is the biggest Swadeshi FMCG brand. There is a great deal of information one can gain from Patanjali’s plan of action.

Baba Ramdev made an unpredictable plan of action for selling ayurvedic items. He never introduced his products as ayurvedic medications in the market, he propelled them as FMCG products.

Patanjali Ayurved is not entirely different from other FMCG organizations but it has a strategy similar to them as the products are offered to clients at an edge to procure a benefit.

Here are the factors which helped Patanjali to achieve success.

Pricing of Products

Moderate estimating of Patanjali items is one reason for its solid infiltration into the Indian market. As Baba Ramdev stated, the motivation behind Patanjali is Upkar and not Vyapar. Patanjali aims to give great quality items at low costs. How is it able to sell items at lower prices when compared to its rivals?

The organization sources items legitimately from ranchers and removes middlemen from the picture. This allows Patanjali to reduce crude material acquirement costs.

Patanjali appreciates a duty excluded status which is smack on the essence of other FMCG organizations.

Patanjali acquired terrains at a much-limited rate.

Patanjali doesn’t contract MBAs for selling their item, it employs a lesser number of experts. The organization has faith in assembling the items which the customers may purchase without the need for additional push to sell the item. There is nobody in that organization who is paid crores in salary.

The edge of merchants and retailers is less in Patanjali items when contrasted with other FMCG items.

Swadeshi Factor

The advancement system of Patanjali is entrancing with the “Make In India” campaign to gain more attention from the customers. Baba Ramdev’s main motive is to replace MNCs. They promote their products by saying that it doesn’t contain unsafe synthetic compounds and only natural pith. “Also by purchasing our items, you are guaranteeing the cash you spend remains in India.” The Swadeshi factor has proved to be a profitable strategy.

Baba Ramdev Buzzing Personality

Patanjali doesn’t rely on entertainers or sportsmen to promote its catalogue. Baba Ramdev is a steadying force. He has amassed an enormous group of devotees over 20 years through diligent work around yoga and Ayurveda. This saves the Indian FMCG giant a lot of investment when it comes to promotion and publicity.

A large number of individuals, from India as well as abroad, follow this other-worldly master. Baba accepted this as an open door and propelled a different scope of items under the brand name ‘Patanjali’.

Branded House Strategy

In this technique, different items are propelled and advanced under one brand. For instance – Apple has different items like Mac, iPad, iPhone, and more. Even though each one of them is unique and performs various capacities, collectively they are seen as Apple items.

Similarly, Patanjali advances all of its items under one brand. This additionally encourages lower costs in showcasing and publicizing as it doesn’t need to advance every item. Patanjali pushes for the image name “Patanjali.”

Distribution & Supply Strategy

Distribution And Supply Chain Of Patanjali

Patanjali Ayurved Ltd. built its one-of-a-kind retail organization. It began selling products through its own channels of super distributors, distributors, Chikitsalayas (franchise dispensaries), and Arogya Kendras.

Chikitsalaya – Pharmacies where specialists analyzed patients for nothing and suggested purchasing drugs from stores nearby. This is a unique system no other organization thought of.

Patanjali Arogya Kendras, a well-being and health focus centre.

Non-drug outlets are called Swadeshi Kendras. Additionally, the organization has numerous restrictive outlets across India. Patanjali items can also be purchased online.

Promotion Strategy

Marketing Mix Model Of Patanjali Ayurved

Patanjali uses a marketing mix model strategy to promote its brand or product in the market. The 4Ps make up a typical marketing mix – Price, Product, Promotion and Place.

Price: Patanjali uses a value-based pricing strategy primarily based on a consumer’s perceived value of a product or service that aligns with its competitors.

Product: It has a wide range of all existing and herbal products for different diseases.

Segmentation: Patanjali divides the market on the basis of age, lifestyle, personality, class, gender, etc. depending upon the people looking for healthy FMCG products.

Targeting: Patanjali offers products for all aged people but it targets mainly middle and upper-middle-class families who prefer ayurvedic products.

Positioning: Patanjali positioned itself as a healthier and safer product in the FMCG category that treats diseases with zero side effects.

Authentic Selling Strategy

Strategies Of Patanjali Ayurved

Patanjali uses an authentic selling strategy/authentic marketing to communicate openly, honestly and genuinely with customers. Baba Ramdev promotes the product in his yog shivir, youtube channels and other media platforms.

Patanjali – SWOT Analysis

The SWOT analysis of Pantajali Ayurved is mentioned below:

SWOT Analysis | Patanjali Ayurved Limited

Strengths

Offers 100% natural products with few side effects.

The brand image of the trust.

Extensive marketing has helped Patanjali to consider socially responsible for the health of the society, thus pulling people into accepting its products as a healthier and safer option.

Baba Ramdev’s buzzing personality helped in the quick sale of the products.

Excellent word-of-mouth marketing has helped the brand grow.

Established a successful distribution network in urban areas.

Weaknesses

Low export levels.

Diversification to other products raised quality issues.

No distribution network in rural areas.

Less expenditure on marketing and promotional activities.

Opportunities

Patanjali can tap the overseas and rural market as people are becoming more health-conscious.

Can enter more segments in personal hygiene, FMCG, etc.

Can diversify in different sectors like clothing, education, restaurants, etc.

Can bring change in the trend of becoming more health-conscious and using more organic products.

Threats

Political Interferences.

Big players can overcome new competition from Patanjali with their existing model.

Patanjali has a wide range of quality products – Natural Food Products, Natural Health Care, Natural Personal Care, Ayurvedic Medicines, Herbal Home Care & Patanjali Publication with 50000000+ consumer reach, 300000+ stores reach, 1000+ products and 5000+ Patanjali stores.

Patanjali Food and Herbal Park at Haridwar is the primary creation office of Patanjali Ayurved. The organization has a creation limit of ₹35,000 crores ($5.1 billion) and is growing to a limit of ₹60,000 crores through its new generation units at a few spots, including Noida, Nagpur, and Indore.

The organization intends to set up further units in India and Nepal. In 2016, the Patanjali Food and Herbal Park were given a full-time security front of 35 outfitted Central Industrial Security Force (CISF) commandos. The recreation centre will be the eighth private establishment in India to be watched by CISF paramilitary forces. Baba Ramdev is himself a “Z” class protectee of focal paramilitary forces.

Patanjali Ayurved produces items in the class of individual consideration and food. The organization makes more than 2,500 items, including 45 sorts of corrective items and 30 kinds of sustenance items.

As indicated by Patanjali, all the items fabricated by Patanjali are produced using Ayurveda and characteristic components. Patanjali has additionally propelled magnificence and infant products.

Patanjali Ayurvedic producing division has more than 300 drugs for treating a wide scope of sicknesses and body conditions, from normal cold to ceaseless paralysis. Patanjali propelled Atta noodles on 15 November 2015. The organization is accounted for fabricating conventional garments like Kurta, Pyjama and jeans.

On 5th November 2016, Patanjali declared that it will set up another assembling plant Patanjali Herbal and Mega Food Park in Balipara (Assam) by contributing ₹1,200 crores ($170 million). It would have an assembling limit of 10 lakh products every year. The new plant will be the biggest office of Patanjali in India and is operational at the moment. Patanjali as of now has around 50 assembling units in India.

Patanjali – Why Did It Saw Downfall?

Patanjali Ayurved, being one of the leading FMCG brands in India, had seen a downfall in its sales in 2017. Patanjali has always been the consumer’s favourite due to its affordability, use of natural & organic ingredients and Swadeshi factor.

Following are the reasons that have slowed down the growth of Patanjali in 2018:-

Lack of Innovation: Without innovation, there is not anything new and without anything new, there is no progress especially when everything around you is innovating. Since the introduction of the goods and services tax (GST) hit its operations in 2017, Patanjali has not managed to recover from the low growth cycle. As a result, its top line declined 10% in FY18. The decline was primarily because of its inability to adapt to the GST regime and develop infrastructure and supply chain.

Lack of Advertising: The decrease in advertising slowed down the growth of Patanjali. Patanjali didn’t focus more on advertising as a result faced a decline in its sales because people were not aware of its natural and organic products.

Ignoring Competition: One of the major reasons why Patanjali faced decline is ignoring its competitors. It’s very important for a company to keep an eye on its competitors. Patanjali has created many rivalries along with success and started rolling out their own variant of natural and organic products.

Poor Management: After gaining huge popularity among consumers, Patanjali diversified itself among various sectors besides FMCG. It became difficult to manage the business verticals and ensure quality checks of the products. As a result, various quality issues emerged that resulted in the decline of its growth.

Despite single-digit top-line growth in FY20, Baba Ramdev was hopeful that Patanjali will regain its lost glory.

Patanjali Ramdev reported a 9% jump in its revenue in FY21 and the net profit grew 14%. The net profit of Patanjali was Rs 485 crore while its revenue was around Rs 1000 Crores. The fast-moving consumer goods (FMCG) major Patanjali Ayurved has reported a 22% growth in its net profit for 2019-20 (FY20). According to the financial data accessed by business intelligence platform Tofler, the group’s flagship entity reported Rs 423 crore net profit for the year, compared to Rs 349 crore it had posted in 2018-19 (FY19).

Patanjali Ayurved, earned over 80% of Patanjali Group’s total revenue, such that its operating revenue grew 6% to Rs 9,023 crore in FY20.

The firm’s top-line growth remained higher than the previous year. In FY19, the Ayurveda major had clocked Rs 8,330 crore turnover – 2.4% higher than Rs 8,136 crore it had posted in 2017-18 (FY18).

Since its sales lost momentum in 2016-17 (FY17), Patanjali is yet to regain the momentum it used to have earlier.

In 2014-15 and 2015-16 (FY16), its revenue had grown 86% and 100%, respectively.

In recent years, its net profit, too, has suffered. Despite double-digit growth, Patanjali’s net profit fell well short of the Rs 1,190 crore it had reported four years ago.

In FY20, its net profit margin stood at 4.67%, compared to 13.3% in FY17 and 16% in FY16.

Some anticipated incomes of ₹5,000 crores ($720 million) for 2015–16. Patanjali proclaimed its yearly turnover for the year 2016-17 to be ₹10,216 crores ($1.5 billion). It was recorded thirteenth in the rundown of India’s most confided in brands (The Brand Trust Report) starting in 2018, and positions first in the FMCG classification.

Patanjali Ayurved Ltd has achieved a tremendous presence around the globe and throughout India in a very small time since its inception in 2006. They have more than 47000 retail counters, 3500 distributors, multiple warehouses in 18 states and proposed factories in 6 states.

Future Of Patanjali Ayurved

Patanjali is the quickest developing organization in the Indian FMCG segment, a $50 Billion industry once commanded by worldwide behemoths – a semblance of Unilever, P&G, Nestle, Colgate – Palmolive, Johnson and Johnson.

From cleanser and bread rolls to ghee and noodles, and now clothing and footwear – no indigenous organization has fabricated such a well-differentiated item portfolio. It has developed more than multiple times in income in the most recent five years and is an unmatched accomplishment in India’s FMCG industry.

The organization focused on incomes of Rs.10,000 crore for FY 2016-17 and Rs. 20,000 – 25,000 crore in FY 2018. It has a broad deals channel of more than 5000 merchants, 15,000 stores, and 100 uber bazaars.

Also, it has tied up with retail chains like Future Group, Reliance Retail, Hyper City, and Star Bazaar. The ongoing declarations of a Rs. 1,600 crore sustenance park in Noida and a Rs. 1,200 crore creation office in Assam highlight the buzz around Patanjali’s arrangements to showcase the organization’s hearty extension plan.

With a growth rate of 130%, the Patanjali Group is planning to make a foray into major global markets. As the group is already present in markets like the US, Canada, the UK, Russia, Dubai and some European countries, it is willing to spread its wings wider and farther.

Conclusion

Patanjali, being a Swadeshi brand has always been in the limelight because of its Ayurvedic products. Each of their steps has been cleverly strategized to bring the best to the brand. Even after facing a few setbacks, the company is standing tall as ever, being the fastest-growing company in the Indian FMCG sector.

Patanjali is expected to go a long way in the future, only if it manages to keep itself ahead of competitors. It has a major advantage over other competitors as Baba Ramdev, a famous Yoga teacher, is the face of the firm.

FAQs

Who is the founder of Patanjali products?

Baba Ramdev & Acharya Balkrishna are the founders of Patanjali products.

When was Patanjali established?

Patanjali was established in 2006.

Are Patanjali products FSSAI approved?

Many Patanjali products lack approval by the Food Safety and Standards Authority of India (FSSAI) the federal food safety regulator of India.

What strategy made Patanjali so successful?

The Swadeshi factor, and claim to be chemical-free products promoted by Baba Ramdev have proved to be a profitable strategy for Patanjali.

Who are the competitors of Patanjali?

The top competitors of Patanjali are:

Dabur India

Procter and Gamble

Marico

ITC

Nestle Ltd.

HUL (Hindustan Unilever Limited)

Baidyanath

Emami

Himalaya Herbal

What is the revenue of Patanjali?

The revenue of Patanjali was recorded $4.2 Billion in 2021.

We often come across the question of whether e-commerce or retail is best for a business. E-commerce is a replica of business that enables individuals and companies to sell their services or products via the internet. On the other hand, retail refers to the brick and mortar businesses, in which individuals sell their goods or services from person to person in shops, malls, and localities.

WIDGET: leadform | CAMPAIGN: undefined

According to Statista 2021, total retail sales, both online and offline, amounted to 24.2 trillion USD, out of which 19.1 trillion USD was generated by the brick and mortar retail channel and around 4.9 trillion USD was generated by the eCommerce sales channel. In the same year, global retail sales accounted for a growth of 9.7% as a whole and eCommerce accounted for around 19.6% of total retail sales.

The digital form of business has seen a great increment specifically in this pandemic. But at the same time, the heavy revenue generated from retail cannot be ignored. In this article, we will discuss different factors that will help you know what is best for your business between eCommerce and retail.

Retail Ecommerce Sales Worldwide from 2017 to 2022

In the following points, we will discuss a comparison between eCommerce and retail from different perspectives:

Which Has Lesser Prior Investment?

Ecommerce Starting an eCommerce business may sound like an expensive process but with proper planning and execution, one can start running it on a budget. The investment required to start your eCommerce business in India is nearly 5-10 lakh rupees. It includes building your business website, hosting, domain, sales and management tools, web development, and advertisements.

Retail Investment in setting up a retail store can be an expensive process. A retail store has to invest in various things before selling its product. These include building, buying, or renting a store, paying license fees, hiring staff for multiple positions, paying location tax, investing in filling up the store with sufficient items to attract a customer, and other necessary resources relating to business and government. All such expenses make setting up a retail store far more expensive than starting an eCommerce store.

So, comparatively, the cost of investment is lower in the case of eCommerce than in retail. The advantage of owning an eCommerce store is that it reduces the cost of setting up a brick-and-mortar store or hiring delivery staff. This is because eCommerce stores send their manufactured products to branches such as Amazon, FedEx, Ship Bob, Flipkart, etc. for order fulfilment. After this, it is the responsibility of these branches to pack, track and send the order to the buyer.

Ecommerce It is easier to maintain eCommerce compared to a retail store. But there are still some complications that need to be checked from time to time so that the store can run smoothly. For example- you need to maintain a warehouse or any proper space to keep the products safe and accessible for dropshipping. Since you are not directly connected with your customers, you will have to keep a check on analytics to track customer experience and discover their new tastes and likings. You will also need to keep a check on the timing of product delivery to avoid negative feedback from customers.

Retail The retail business is considered to be a bit more complicated in terms of maintenance. This is because for various reasons like there is a need to maintain a proper brick-and-mortar store and inventory, and maintenance of an adequate communication balance on both sides in real-time with suppliers and customers. Also, you have to keep a regular check on your staff if they are handling the customers politely. You will have to train them and make them more knowledgeable about the services and products you are offering so that they can deal with the customers pleasantly and accurately.

It is easier to modernize the stock in an eCommerce store. But this task becomes pretty difficult with retail stores as for updating products, you need to set up meetings with suppliers now and then. So, in case of ease of maintenance, eCommerce is a better option for your business.

Share of consumers going to brick and mortar stores by country in 2021

Which Has Better Profitability in Future?

Ecommerce With eCommerce comes a great benefit which is unlimited access to customers. Once you are over the internet, there is no limit to the number of people you can reach. Ecommerce allows you to showcase your products and services to a large number of people, therefore, no limitation to any particular locality. Moreover, you can always expand your business and attract new customers via smart and modern marketing techniques. These include offering free shipping, discounts, gift cards, reward points, etc. All this ultimately ensures better sales and thus, better profits.

Retail Retail stores do not have very wide access to the customers as they have limitations due to their fixed location. However, this does not mean that there are no benefits of a retail store. Even in today’s time, many customers do not feel satisfied until they can touch and feel the products themselves. So, the customers who are still skeptical about online shopping contributes to the sales and profits of retail stores. Moreover, there are fewer chances of online fraud with retail shops, as the customer doesn’t need to provide their personal information including emails, mobile numbers, bank details, etc.

In this case, eCommerce will be the clear winner because the products and services of eCommerce stores are visible to a huge audience which makes for a large potential customer base and thus, better sales and profits.

We compared e-commerce and retail stores based on investment, performance easiness, and profits obtained. Although there are factors like trusted quality and physical interaction that make retail stores better than eCommerce ones. But after making an overall comparison and looking at the future of the digital world, we concluded that eCommerce stores are the best way to expand your business and earn more profit in the future since it offers a wider reach with less investment.

However, you can also take another way which is you can opt for omnichannel retail as it allows you to buy products either online or physically through the real stores to keep your customers satisfied in all the possible ways.

FAQs

What is the difference between eCommerce and retail?

Retail is something that can be conducted in a brick-and-mortar store, online, between persons, or through direct mail. However, eCommerce refers to electronic commerce which means commercial transactions that are conducted only through the internet.

How owning an online store is better than physical stores?

Owners of the online stores can sell and ship their products and services to a large number of people with fewer investments as buying a website is easier and more economical than buying a physical store.

What is the biggest challenge faced by eCommerce?

One of the most significant challenges faced by eCommerce is the security issue. Ecommerce involves a great deal of personal information and even a small technical issue can create huge damage to a business’s operations and image.

What is a retail store?

The most common example of a retail store is the conventional brick-and-mortar stores like Walmart, Best Buy, etc. However, retailing as a whole includes goods or services sold through stores, kiosks, or even on the internet.

Today, the fast-food industry has become a big part of our daily lives. Some brands are so popular that their names are linked to the food they serve—like McDonald’s for burgers, Coke for soft drinks, and Domino’s for pizza.

While many fast-food businesses struggle to gain recognition, Domino’s has built a strong brand with its delicious taste and consistent quality. It has earned the trust of loyal customers and continues to grow. Let’s take a look at the story behind Domino’s success.

This Domino’s case study explores how the brand became a global leader in pizza delivery through innovation, quality, and customer satisfaction.

It was in 1960, when Tom Monaghan and his sibling, James, assumed control over the activity of DomiNick’s, a current area of a little pizza café network that had been claimed by Dominick DiVarti, at 507 Cross Street (presently 301 West Cross Street) in Ypsilanti, Michigan, close to Eastern Michigan University.

The arrangement was verified by a $500 initial installment, and the siblings obtained $900 to pay for the store. Within eight months, James exchanged his half of the business to Tom for the Volkswagen Beetle they utilized for pizza deliveries.

Monaghan needed the stores to have a similar marking, yet the first proprietor disallowed him from utilizing DomiNick’s name. At some point, a worker, Jim Kennedy, came back from a pizza conveyance and proposed the name “Domino’s”. Monaghan quickly cherished the thought and authoritatively renamed the business Domino’s Pizza, Inc. in 1965.

The organization logo initially had three dabs, speaking to the three stores in 1965. Monaghan intended to include another spot with the expansion of each new store, yet this thought immediately blurred, as Domino’s accomplished fast growth. Domino’s Pizza opened its first establishment area in 1967 and by 1978, the organization extended to 200 stores. Domino’s Pizza had 20,591 restaurants worldwide as of 2023.

Domino’s Entry in India

Jubilant Foodworks started its business under the name Domino’s Pizza India Private Limited in 1995 and opened the first outlet of Domino’s Pizza in 1996.

In the first quarter of 2014, Jubilant Foodworks inaugurated the 700th Domino’s Pizza outlet, and in the next 24 months, they went on to open 300 more outlets, making India only the second country after the United States to reach the 1000 mark for Domino’s Pizza.

After being in operation for over 20 years now, Jubilant Foodworks has over 1000 Domino’s Pizza outlets in India and 20 outlets in Sri Lanka while holding contracts for both Bangladesh and Nepal. The company aims to double its outlets by 2021.

In 2011, Jubilant Foodworks signed a franchise agreement with Dunkin’ Donuts, an American coffee, and donuts chain to open its stores in India, the first of which opened in 2011.

In January 2016, Domino’s opened its 1000th outlet. In 2016, the Center for Science and Environment(CSE) revealed that their pizza bread was bound with poisons and cancer-causing agents, for example, potassium bromate and potassium iodate. Domino’s did not react to the CSE questions Potassium bromate is a Category 2B cancer-causing agent, which means it can cause liver cancer. In 2017, live bugs were found in Domino’s pizza flavoring sachets in Delhi, a video of which went viral. This provoked Domino’s to quit giving flavoring sachets for quite a while. When they restarted, they changed the pressing from straightforward to obscure.

The organization’s present direction can be followed back to 2010, when Domino’s patched up its pizza formula and propelled a striking “Goodness Yes We Did” crusade that got itself out for having a dreary item.

Since then, systemwide deals have bounced from $3.1 billion to $5.9 billion in 2017. The organization’s methodology has aroused financial specialist intrigue, as well. It’s putting it mildly to state that Domino’s has been having some fantastic luck recently. While a significant part of the business has been level to marginally positive, the pizza mammoth has posted income development above 20% for as far back as 75%, and has encountered 30 successive quarters of same-store deals development.

On account of this reliable advancement, Domino’s outperformed Pizza Hut in 2017 to turn into the nation’s biggest pizza chain by deals, even though it has around 2,000 residential units.

Domino’s is anticipating $25 billion in yearly deals all around by 2025 – twofold its 2017 offers of $12.25 billion – just as 2,000 new U.S. stores inside that time allotment.

Domino’s Revenue and Growth

Domino’s Global Revenue

Domino’s Pizza generated a revenue of 4.36 billion U.S. dollars worldwide in 2021.

The principal source of income for Domino’s is its inventory network which records for the most noteworthy piece of its whole income. Aside from that the sovereignty and expenses it gets from its franchisees are the second biggest wellspring of pay for the brand. Domino’s likewise worked a set number of stores in the US advertise. The Inventory network of Domino’s takes into account certain Domino’s franchisees and the organization’s working stores in the US and Canada. In 2018, the supply chain section of Domino’s represented around 57% of its income. It produced about 1.94 Billion US dollars in income. The rest of the sources including eminences and charges from the US and worldwide franchisees just as deals in the organization worked stores created about 1.5 Billion US dollars in income. Domino’s inventory network works 19 local mixture assembling and sustenance store network focuses in the US and 5 batters assembling and nourishment production network focuses in Canada.

Following are the factors of the success of the dominating pizza company, Domino’s:

Adaptability to Digital and Online Mediums

While the kitsch of the stove vehicle may not speak to each financial specialist, Domino’s has made a striking showing on the innovation front. It’s forceful in making ways for clients to put in their requests on different stages, including keen TVs, Ford Motor Co. (F) vehicles, and on Twitter through emoticons. A ravenous client doesn’t need to look into the number and call – he can arrange a pie on a smartwatch or over a plain exhausting Internet program. “They have a greater number of approaches to get to the brand than contenders,” says BTIG overseeing chief of cafés Peter Saleh. Be that as it may, smaller organizations have fewer assets to adjust to changing innovations and requests, which gives Domino’s a bit of leeway. Domino’s gains 55 percent of U.S. deals through requests on the web or using versatile stages, says Stephen Andersen, an investigator at New York City speculation firm Maxim Group. Furthermore, it’s getting up to speed with Pizza Hut’s piece of the overall industry. Domino’s expanded its piece of the pie from 9 percent to 12.3 percent in 2014, while Pizza Hut slipped from 14.7 percent to 14.4 percent.

Pricing

Some inexpensive food chains are attempting to one-up one another with regards to evaluating fast suppers. Wendy’s Co. (WEN) dismissed things from a year ago with a four-for-$4 bargain. Others went with the same pattern, including Carl’s Jr. Eatery Brands International-possessed Burger King (QSR) and even Pizza Hut. Domino’s has done little to respond to this pattern. “The heft of the cheap food endeavors are at breakfast or lunch,” says Longbow Research expert Alton Stump. “There’s not as much direct presentation” for Domino’s. Genuine, Domino’s offers some menu things for $5.99 (on the off chance that you purchase at least two), yet Pizza Hut offers a comparative, lower-cost alternative. Ease contributions tend to cut into net revenues, however, Dominos has been invulnerable with that impact – truth be told, incomes have bounced 23 percent since the organization presented its ease menu in 2013.

Untapped Markets

Just 7 percent of Domino’s business originates from nations outside the U.S., including the U.K., India, and South America. In any case, this is the place where financial specialists see the most potential pushing ahead. “It’s a long haul plan, yet there’s still a great deal of topography out there,” Andersen says. The organization saw an 11.7 percent bounce in the number of stores in 2015 and hopes to include somewhere in the range of 7 and 8 percent every year for a long time to come. One zone it’s just starting to infiltrate is China. Pizza Hut has had the main mover advantage in the nation and Yum is planning to turn off its China-centered business. Be that as it may, while Pizza Hut has built up a to a greater extent a bistro-like methodology in China, Domino’s can concentrate on conveyance. Furthermore, there’s space to develop – Dominos has just a bunch of stores in China, however, Andersen guesses it could have more than 1,800 by 2030.

Domino’s Future Plans

Domino’s is the main Pizza brand with solid universal nearness. Its income has likewise risen strongly over the most recent five years. By 2025, the organization expects a systemwide number of cafés to have developed over 25,000 stores. The fundamental focal point of the organization is quality and client accommodation. This has prompted solid brand value in the US and global markets separated from high deals, client dependability, and by large ubiquity. Interest in Pizza around the globe is developing and it introduces an appealing open door for Domino’s.

With over 1000 outlets in India and every outlet offering the same tasty pizzas that everyone loves, Domino’s has shown everyone that standardization of taste and quality is very well achievable no matter how big the enterprise is. With over 1000 stores in just over 20 years and the goal of 1000 more in another 5, Domino’s India has shown what it looks like to be successful.

The new and improved pizza has indeed struck the right chords with the customers and hopefully will re-establish Domino’s India as the ultimate pizza brand in the country.

FAQs

When did Domino’s open in India?

Domino’s entered India in 1996.

Where was the first Domino’s Pizza store in India?

The first Domino’s Pizza store was opened in New Delhi.

What is Domino’s annual revenue?

Domino’s generated a revenue of $4.36 billion in 2021.

What is Domino’s market share in India?

Domino’s is the market leader in the organized pizza market with a 50% market share and 70% share in the Pizza home delivery.

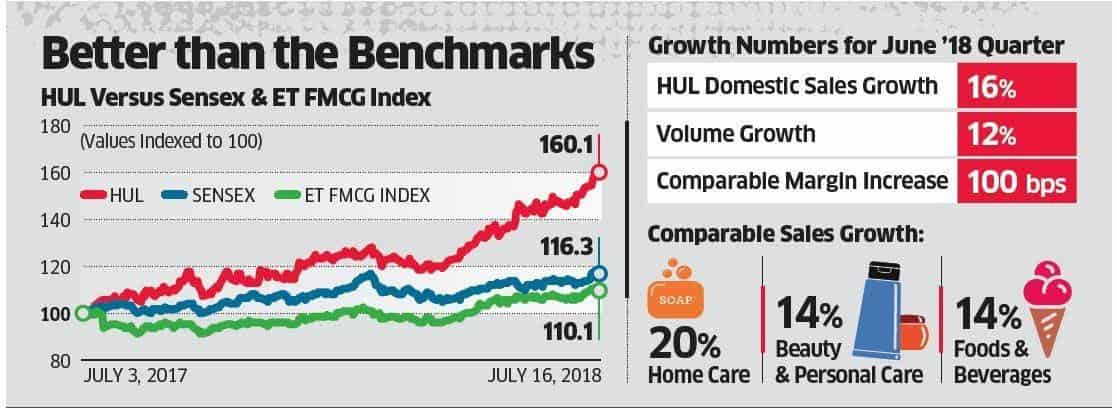

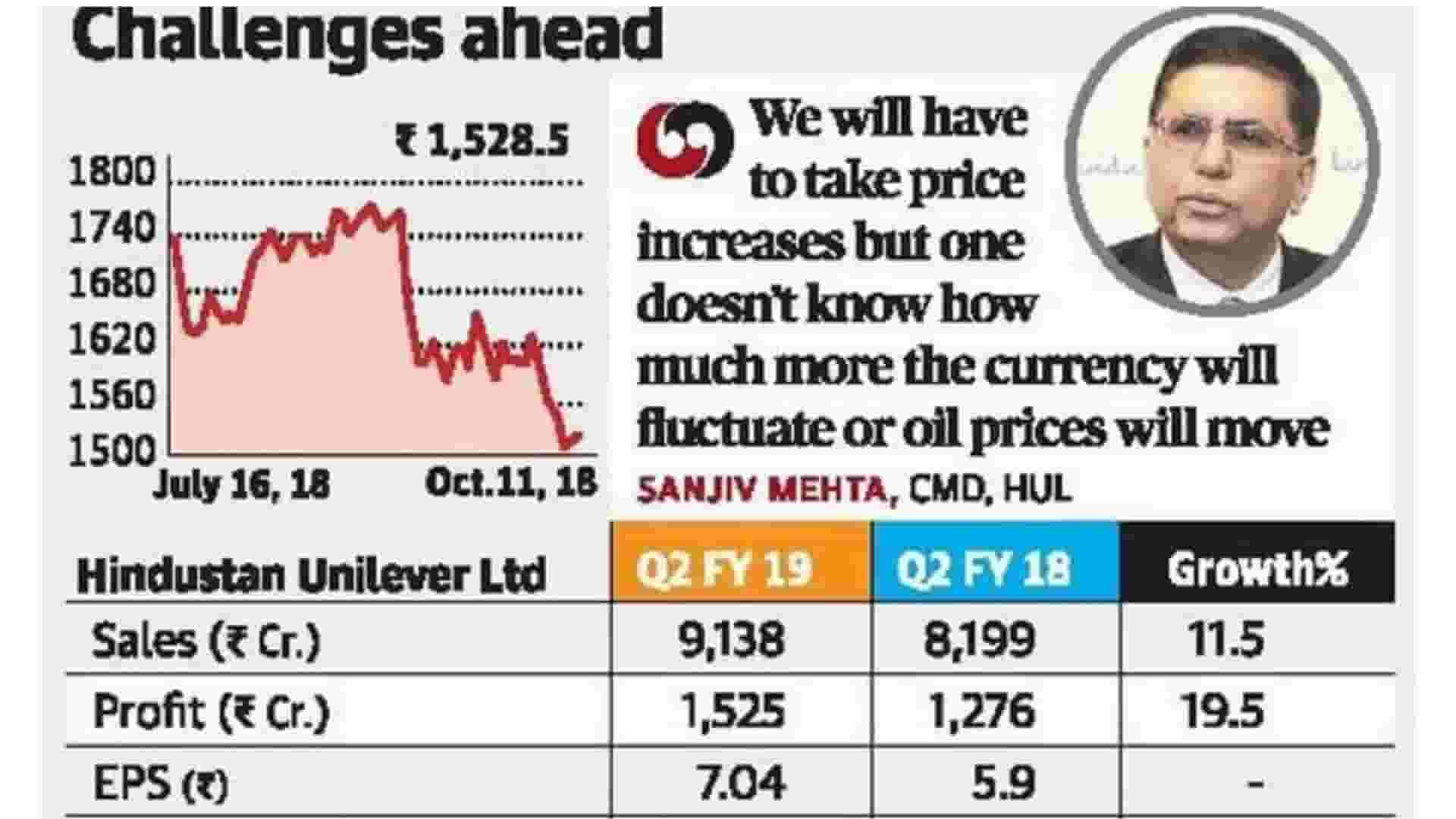

Hindustan Unilever Limited (HUL) is a British-Dutch assembling organization headquartered in Mumbai, India. The items of Hindustan Unilever Ltd incorporate nourishments, drinks, cleaning specialists, individual consideration items, water purifiers, and purchaser merchandise. HUL was set up in 1933 as Lever Brothers and following the merger of its constituent gatherings in 1956, HUL was renamed Hindustan Lever Limited. The organization was then renamed in June 2007 as “Hindustan Unilever Limited”.

At the start of 2019, the Hindustan Unilever Limited portfolio had 35 items marked in 20 classifications and utilized 18,000 representatives with offers of Rs. 34,619 crores in 2017-18. In December 2018, HUL reported its procurement of Glaxo Smithkline’s India business for $3.8 billion out of an all value merger manage ratio of 1:4.39.

However, the joining of 3800 representatives of GSK stayed questionable as HUL expressed there was no provision for maintenance of workers in the deal. In January 2019, HUL said that it hopes to finish the merger with Glaxo Smith Kline Consumer Healthcare (GSKCH India) this year.

Hindustan Unilever Limited (HUL) is India’s biggest quick-moving customer merchandise organization. HUL works in seven business sections.

The cleanser segment incorporates cleansers, cleanser bars, cleanser powders, and scourers. Individual items incorporate items in the classifications of oral consideration, healthy skin (barring cleansers), hair care bath powder, and shading beautifiers. Refreshments incorporate tea and espresso.

Nourishments incorporate staples (atta salt and bread) and culinary items (tomato-based items natural product-based items and soups). Frozen yogurts incorporate frozen yogurts and solidified treats. Others incorporate synthetic substances and water business.